ACCT1501 Lecture Notes - Lecture 8: Inventory Control, Perpetual Inventory, Income Statement

18 May 2018

School

Department

Course

Professor

Thursday, 4 May 2017

Accounting & Financial Management 1A

Introduction to Inventory & Non-Current Assets

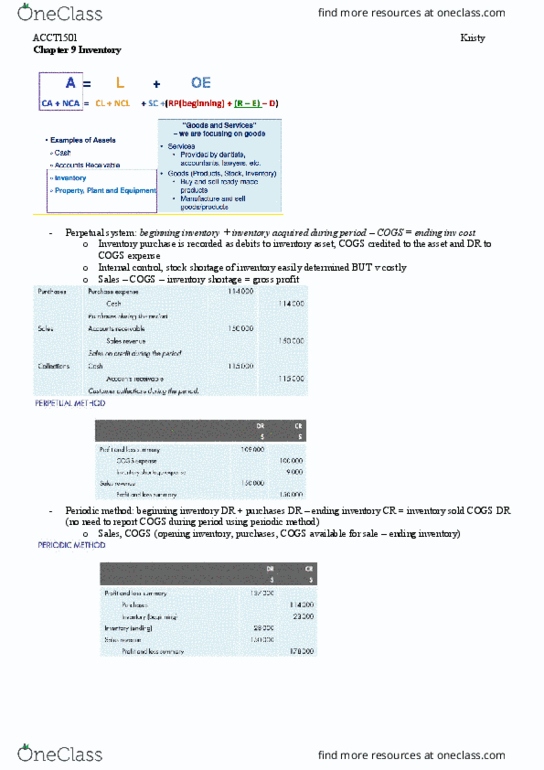

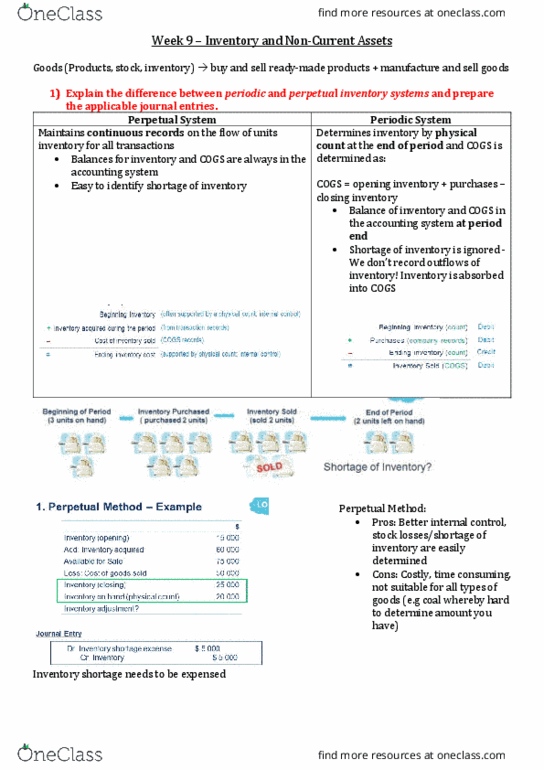

-Inventory Control Systems:

•Perpetual System: Maintains continuous records on flow of units of inventory for all

transactions

-Balances for inventory & COGS always in accounting system

-Easy to identify shortage of inventory

-Provides better control

-Stock losses/ shortage of inventory easily determined

-However, is costly & not suitable for all types of goods (e.g. coal)

•Periodic System: Determines inventory by physical count at end of period

-COGS = Opening inventory + Purchases - Closing Inventory

-Balance for inventory & COGS in accounting system at period end

-Shortage of inventory is ignored

-Sales of inventory require only ONE entry

•Measurement rule - lower of cost & net realisable value

-Cost comprises:

•Cost of purchase

•ADD: Purchase price + import duties & other taxes + inward transport &

handling costs + any other directly attributable costs of acquisition

•LESS: Trade discounts, rebates & other similar items

•Not included - administration costs, selling costs & storage costs

-Cash Flow Assumption:

!1

find more resources at oneclass.com

find more resources at oneclass.com

Thursday, 4 May 2017

•First In, First Out:

-Assumes first units purchased = first units sold

-Assumes ending inventory contains units purchased most recently

-Results in:

•Higher profit level in times of rising prices (relative to LIFO & weighted average)

•Closing inventory balance closer to current cost (relative to LIFO & weighted

average)

•Suitable for perishable items, electronics etc

•Last In, First Out:

-Assumes last units purchased = first units sold

-Assumes ending inventory contains units purchased earliest

-Results in:

•In time of rising prices, lower value of ending inventory (higher COGS —> lower

profit —> nice tax implication)

•Often does not match physical flow

•Closing inventory balance may not be relevant

•NOT permitted under Australian accounting standards but permitted in the

United States

•Weighted Average:

-When using perpetual inventory control system, referred to as moving average

-Note:

•Simple to apply & less subject to profit manipulation

•Appropriate for similar products & ‘non-expiry’ items

•When prices are changing, each method will provide different ending inventory &

COGS value

•Sum of these two items will always be the same, no matter what the method

-Cost can either be an asset or an expense

-Total cost = asset + expense

-So at the end of the period: Total cost = inventory on hand + COGS

!2

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Inventory control systems: perpetual system: maintains continuous records on ow of units of inventory for all transactions. Balances for inventory & cogs always in accounting system. Stock losses/ shortage of inventory easily determined. However, is costly & not suitable for all types of goods (e. g. coal: periodic system: determines inventory by physical count at end of period. Cogs = opening inventory + purchases - closing inventory. Balance for inventory & cogs in accounting system at period end. Sales of inventory require only one entry: measurement rule - lower of cost & net realisable value. Thursday, 4 may 2017: first in, first out: Assumes rst units purchased = rst units sold. Assumes ending inventory contains units purchased most recently. Assumes last units purchased = rst units sold. Assumes ending inventory contains units purchased earliest. When using perpetual inventory control system, referred to as moving average.