ACCT1511 Lecture Notes - Lecture 11: Management Accounting, Indirect Costs, Cost Driver

6.1 – Management Accounting (Costing)

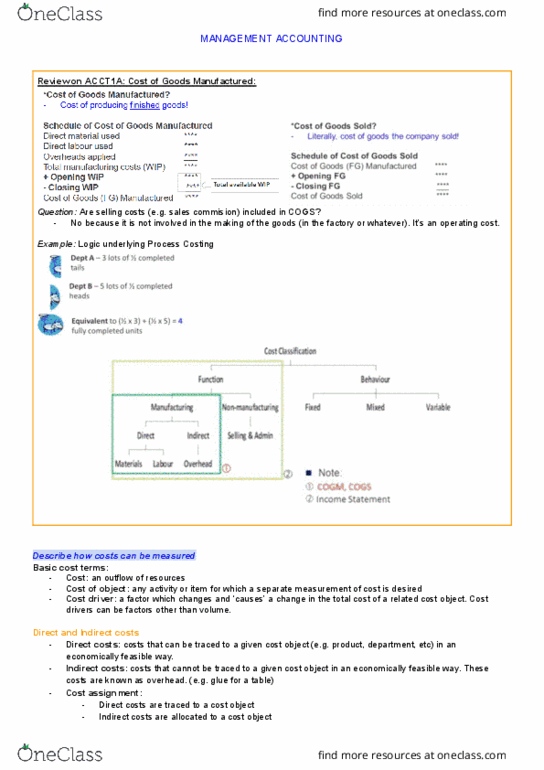

Cost – outflow of resources

Cost of object – any activity or item for which a separate measurement of cost is desired

Cost driver – fator hih hanges and auses hange in total ost

Direct costs – directly traceable to given cost object (e.g. product, department) in

economically feasible way

Indirect costs – cannot be traced to given cost object; known as overhead

Cost assignment:

• Direct costs traced to cost object

• Indirect costs allocated to cost object

Cost measurement:

• Determining dollar amounts of direct materials, direct labor and overhead used

• Can be actual or estimate amounts

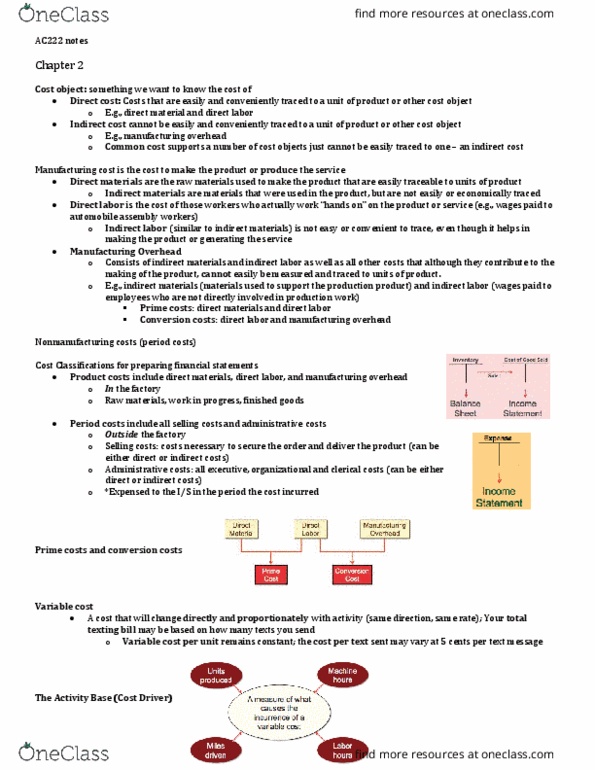

Product costs – osts attached’ to units produced

• Manufacturing costs – capitalized onto product

Period costs – costs that must be charged against income in period incurred

Unit costs – total cost of units ÷ units produced

Prime costs – direct materials & direct labor (able to be traced)

Conversion costs – direct labor & overhead (shape product – transform into final

product)

Normal costing:

• Actual costs for direct materials & direct labor

• Pre-determined costs (adjusted at YE) for overhead

• Timely – able to obtain selling price earlier (not always as reliable)

find more resources at oneclass.com

find more resources at oneclass.com