FINS1613 Lecture Notes - Lecture 9: Risk Premium, Standard Deviation, Investment

Wednesday, 24 May 2017

Business Finance

Cost of Capital

-Risk & Return Concepts:

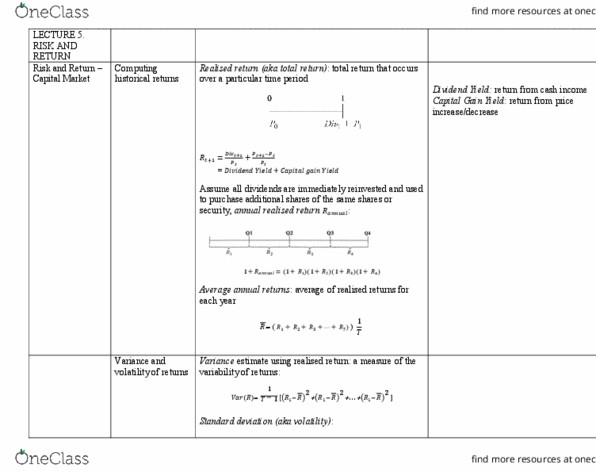

•Realised Returns

-To determine cumulative return on security over multiple time periods, compound

returns for each individual period

-For stocks, assume that all dividends are used to purchase new shares in stock

•All dividends reinvested in stock

•Describing Realised Returns

-Security’s arithmetic average return for a given time-period length is simply

average of realised returns over several such time-periods

-Variance is the average squared deviation of realised returns from the average:

-Standard deviation is the square root of the variance:

-Historical Risk & Return:

•Risk premium - reward for bearing risk:

!1

- 1

find more resources at oneclass.com

find more resources at oneclass.com

Wednesday, 24 May 2017

-Stocks, which are relatively risky, have higher returns than bonds which are

relatively safe

-Portfolios, which are relatively low risk, can perform as well as individual

securities, which have relatively high risk

•Objective - model that is compatible with two observations

1. Stocks outperform bonds, which outperform cash

2. Portfolios can provide similar performance to individual securities, despite

having lower risk

-Types of Risk:

•Systematic risk - linked across outcomes (common risk)

•Unsystematic risk - risks that bear no relationship to each other

-Independent, diversifiable or idiosyncratic risk

-Portfolios:

•Collection of securities, defined by:

1. Securities that are in the portfolio

2. Amount invested in each security

-Possible to have negative amounts invested in security (e.g. borrowing cash &

shorting stocks)

!2

find more resources at oneclass.com

find more resources at oneclass.com

Wednesday, 24 May 2017

•Portfolio Return - weighted average of returns of individual securities, where

portfolio weight (wj) is the value of investment in asset j as % of total portfolio value

•Portfolio containing two assets has a variance given by:

-Diversification:

•Principle of Diversification: As (i) different types of securities are added to a portfolio

and (ii) the average size of each position shrinks, the amount of unsystematic risk in

the portfolio declines to zero & only systematic risk remains

-Unsystematic risk essentially eliminated by diversification

-Relatively large portfolio only has systematic risk

-Systematic Return Principle:

•Risk premium of a security is determined by its systematic risk & does not depend

on its diversifiable (unsystematic) risk

-Only systematic risk earns a risk premium

-Investors not compensated for holding unsystematic risk

-Investors rewarded for bearing systematic risk, otherwise no one would own risky

assets

-As systematic risk increases, expected returns increase

-Capital Asset Pricing Model (CAPM):

•Key implications:

!3

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Risk & return concepts: realised returns. To determine cumulative return on security over multiple time periods, compound returns for each individual period. For stocks, assume that all dividends are used to purchase new shares in stock: all dividends reinvested in stock, describing realised returns. Security"s arithmetic average return for a given time-period length is simply average of realised returns over several such time-periods. Variance is the average squared deviation of realised returns from the average: Standard deviation is the square root of the variance: Historical risk & return: risk premium - reward for bearing risk: Stocks, which are relatively risky, have higher returns than bonds which are relatively safe. Portfolios, which are relatively low risk, can perform as well as individual securities, which have relatively high risk. Wednesday, 24 may 2017: objective - model that is compatible with two observations, stocks outperform bonds, which outperform cash, portfolios can provide similar performance to individual securities, despite having lower risk.