FINS1613 Lecture Notes - Lecture 3: Corporate Bond, Discount Window, Weighted Arithmetic Mean

Valuatio of a Fir’s Securities: Bod

Valuatio

Capital Structure

• How a company finances itself is called its capital structure.

• Companies sell types of securities to investors in return for money.

• Owners of these securities have the rights to cash flows (profits) from

the firm.

• We focus on how to value the securities: BONDS and EQUITY.

• Assets = Liability + Equity

• Enterprise Value + Cash = Debt + Equity

Bonds

• Terms of the bond indicate that amounts and dates of all payments are

to be made.

• Obligation to make payments

• Form of debt financing

Equity

• Preference Shares

- Receive dividend payments generally dictated at issuance

- Receive before ordinary shares receive (but not guaranteed)

• Ordinary Shares

- Holders receive dividends (not guaranteed)

- Represents ownership and carries voting rights

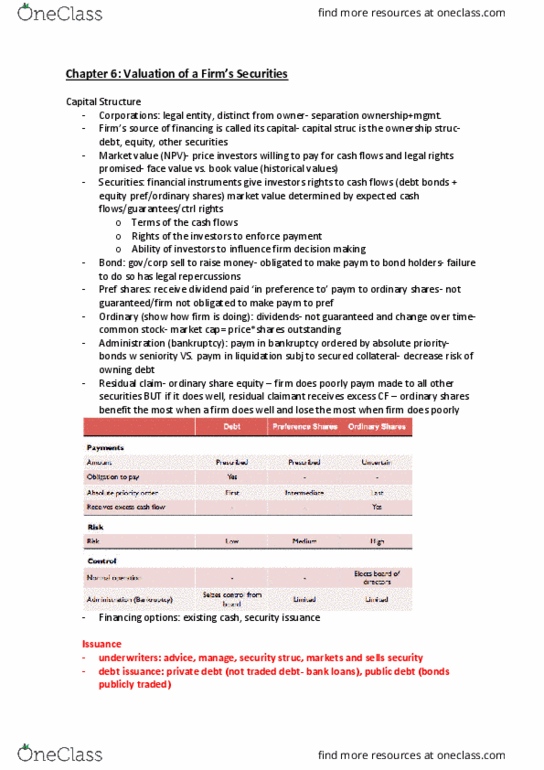

Debt Vs Equity

• Bonds ➔ Preference Shares ➔ Ordinary Shares

• When paying out profits, bond owners get a set return with the

residual amounts going to equity

- When a company does well, Equity gets the most return.

- But when company does not do well, Equity payments stop.

• When company goes bankrupt and is liquidated, payments are made in

the order of preference.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Bonds: terms of the bond indicate that amounts and dates of all payments are to be made, obligation to make payments, form of debt financing. Receive dividend payments generally dictated at issuance. Receive before ordinary shares receive (but not guaranteed: ordinary shares. Debt vs equity: bonds preference shares ordinary shares, when paying out profits, bond owners get a set return with the residual amounts going to equity. When a company does well, equity gets the most return. But when company does not do well, equity payments stop: when company goes bankrupt and is liquidated, payments are made in the order of preference. Term structure of interest rates: relationship between length of investment and its interest rate, determined by expectations of future interest rates. Bond valuation: draw the timeline, discount all the promised cash flows to time 0 to figure out the pv of the bond.