ACCT1101 Lecture 9: L9

lOMoARcPSD|2476239

Lecture9:TheCashFlowStatement

‐

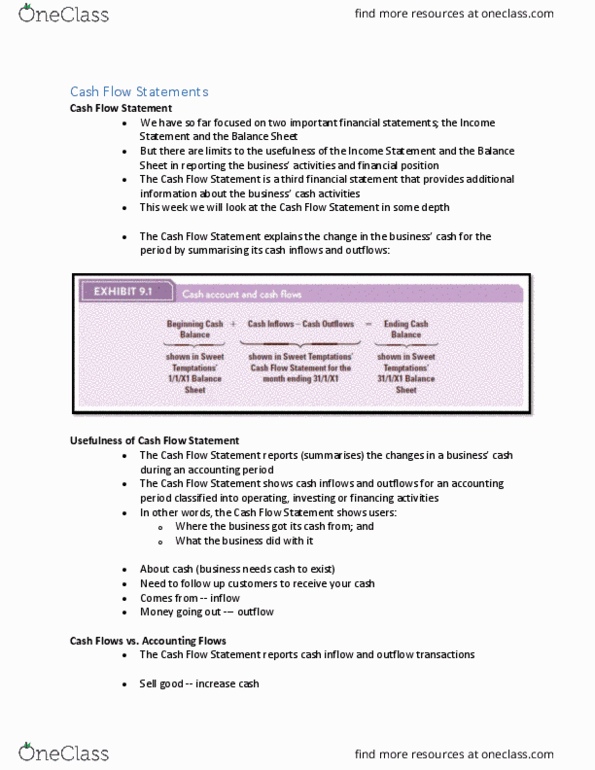

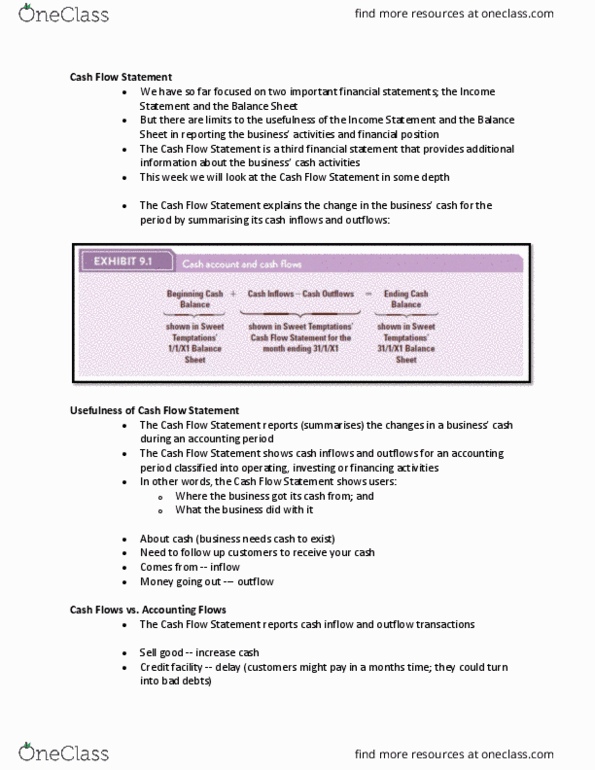

CashFlowStatementreports(summarises)thechangesinabusiness’cashduringanaccounting

period

‐

Creditsalesnotreflectedincashflow.Althoughcreditsalesarereflectedinincomestatementasa

revenue,wouldnotrecordonthecashflow,untilthecashwasreceived

‐

Allinflowsandoutflows,dividedintooperating,investingandfinancingactivities

OperatingActivities:theprimaryactivitiesofbuying,sellinganddeliveringgoodsforsaleaswell

asprovidingservices

Totalcashcollections=netsales+previousyearaccountsreceivable(creditsalesfromlastyear)–

currentyearaccountsreceivable(creditsalesfromthisyear)

Note*Iftheaccountsreceivableaccountdecreasesduringaperiod,thenthebusinesshascollected

morecashfromcustomersthantheamountofcurrentcreditsalesmade.

TotalCashpaymentfrompurchasesbudget(paymentstosuppliers)=previousyearaccounts

payable(creditpurchasesfromlastyear)–currentyearaccountspayable(creditpurchasesfromthis

year)+currentyearpurchases.

Currentyearpurchases=currentyearCOGS+desiredendinginventorycurrentyear–ending

inventoryfrompreviousyear.

Totalcashpaymenttoemployees’=Wagescost+previousyearsalariespayable–currentyear

salariespayable

InvestingActivities:lendingmoneyandcollectingontheloans,investinginothercompaniesand

buyingandsellingpropertyandequipment.(Lendingmoney).Changesnon‐currentassetinbalance

sheet.