BUSS1030 Lecture Notes - Lecture 9: Gross Margin, Financial Ratio, Financial Statement

17 May 2018

School

Department

Course

Professor

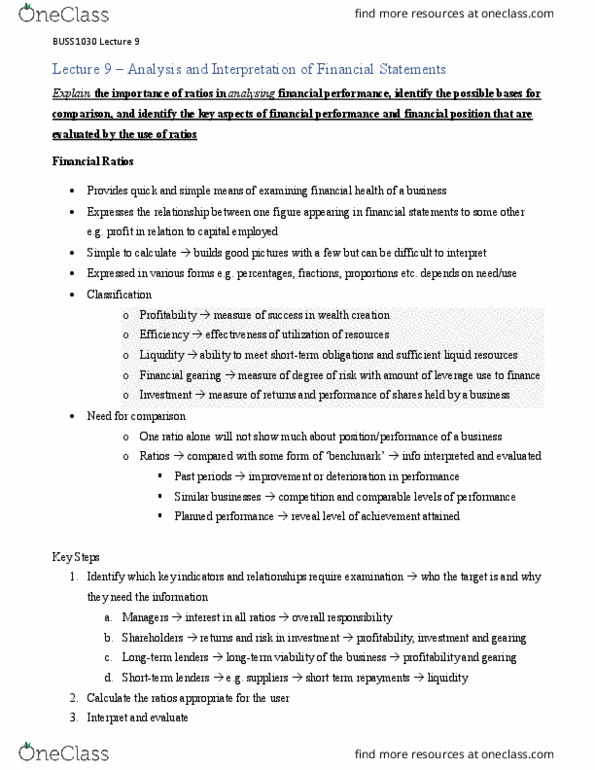

Lecture 10: Analysis and interpretation of financial statements

Financial ratio classification

• Profitability : Measure of success in wealth creation

• Efficiency: Effectiveness of utilisation of resources

• Liquidity: The ability to meet short-term obligations

• Financial gearing: Measure of degree of risk to do with the amount of leverage used to

finance the business

• Investment: Measure of the returns and performance of shares held by a business

The need for comparison

Ratios need to be compared with some form of bench mark for the information to be

evaluated

e.g. past periods; similar business; planned performance

Financial ratios

When a ratio involves a comparison between two statements of financial position, we

use year-end figures

• If the ratio involves both the statement of financial position and the statement of

financial performance, we would use the average of the 2 figures from the statement

of financial position rather than the year-end figure

Profitability ratios

• Return on ordinary shareholders’ funds/return on equity (ROSF)

• Compares the amount of profit for the period available to the ordinary

shareholders with the ordinary shareholders’ average stake in the business

during that same period

•

!"#$ %

&

'()*+,

&

-*,.(

&

,-/-,+)0

&

-01

&

-02

&

3(.*.(.04.

&

1+5+1.01

-5.(-6.

&

)(1+0-(2

&

78-(.

&

4-3+,-9

&

39:7

&

(.7.(5.7

&

;

&

<==

• Return on capital employed (ROCE)

• Relationship between the operating profit generated during a period and the

average long-term capital invested in the business during that period

•

!">? %

&

@ABCDEFGH

&

ACIJFE

K8DCB

&

LDAFEDMNOBPBCQBPNRIGLSCCBGE

&

MFDTFMFEFBP

&

U

&

<==

• Operating profit margin

• Operating profit for the period to the sales during that period

•

"VWXYZ[\]

&

VX^_[Z

&

`YX][\ %

&

@ABCDEFGH

&

ACIJFE

KDMBP

&

U

&

<==

• Gross profit margin

• Relates the gross profit of the business to the sales revenue generated during the

same period

• Gross profit is the difference between sales and cost of sales

•

]X^aa

&

VX^_[Z

&

`YX][\ %

&

HCIPP

&

ACIJFE

PDMBP

&

U

&

<==

Efficiency ratios

• Average inventories turnover period

• Measures the average period for which inventory is being held

•

bcdecfghbei

&

fjhcgdeh

&

kehbgl %

&

DQBCDHB

&

FGQBGEICm

&

8BMn

LIPE

&

IJ

&

PDMBP

&

o

&

pqr

&

• Average settlement period for accounts receivable

Document Summary

Lecture 10: analysis and interpretation of financial statements. Financial ratio classification: profitability : measure of success in wealth creation, efficiency: effectiveness of utilisation of resources. Liquidity: the ability to meet short-term obligations: financial gearing: measure of degree of risk to do with the amount of leverage used to finance the business. Investment: measure of the returns and performance of shares held by a business. Ratios need to be compared with some form of bench mark for the information to be evaluated e. g. past periods; similar business; planned performance. When a ratio involves a comparison between two statements of financial position, we use year-end figures. If the ratio involves both the statement of financial position and the statement of financial performance, we would use the average of the 2 figures from the statement of financial position rather than the year-end figure.