BUSS1030 Lecture Notes - Lecture 10: Marginal Cost, Sunk Costs, Opportunity Cost

31 Jul 2018

School

Department

Course

Professor

Document Summary

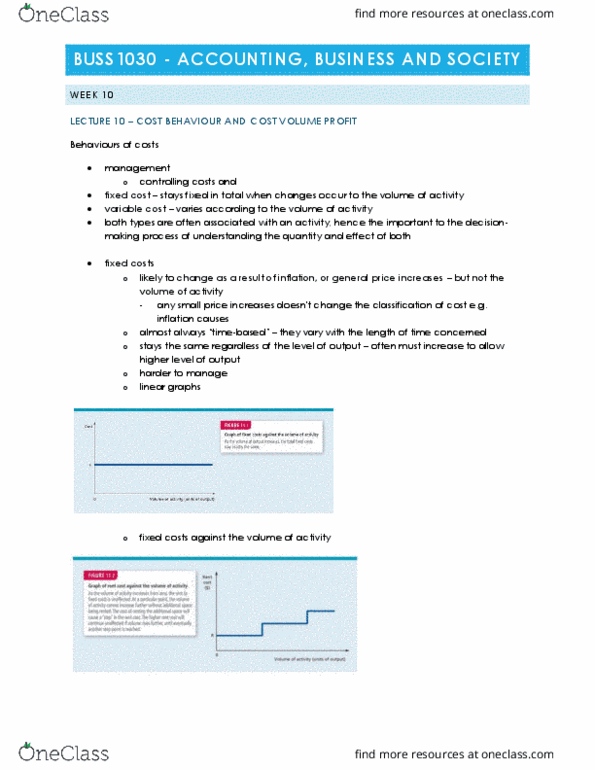

Lecture 10: cost behaviour & cost volume profit - management accounting. Distinguish between fixed costs and variable costs, and explain the importance of a detailed understanding of cost behaviour. The behaviour of costs need to remember formulas ! Both costs often associated/attributed with an activity hence important to the decision-making process of understanding the quantity and effect of both. The cost for heating and lighting would remain largely fixed irrespective of production activity, but for powering of machinery, it would increase with production level: costs have different behaviours depending on what"s driving them/what they"re used for. Apply the distinction between fixed and variable costs to explain and apply break-even analysis. A way of analysing cost behaviour and revenues so as to enable the break-even points (and other target levels of profit) to be calculated. Explain and apply the concept of contribution and contribution margin. Define and distinguish between relevant costs, outlay (historic) costs and opportunity costs.