22107 Lecture Notes - Lecture 4: Retained Earnings, Financial Statement, Trial Balance

Lecture 4 (12th April)

Accrual Accounting and Adjusting Entries

LO1 Accrual & Cash Accounting

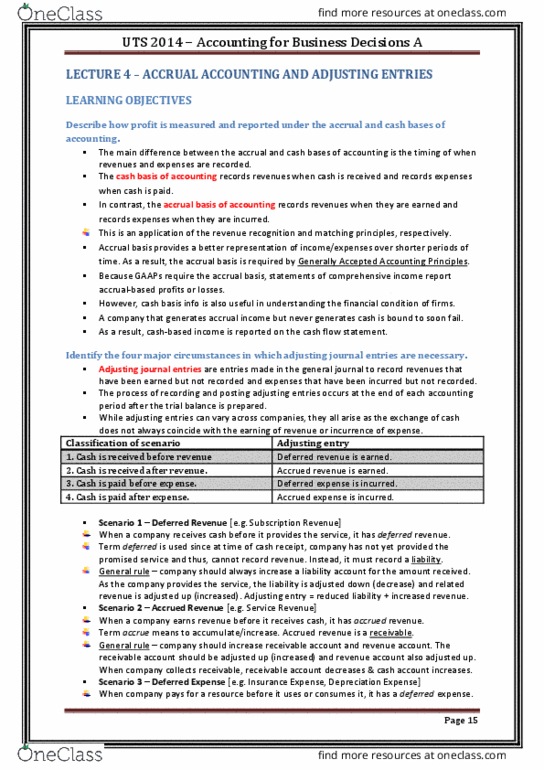

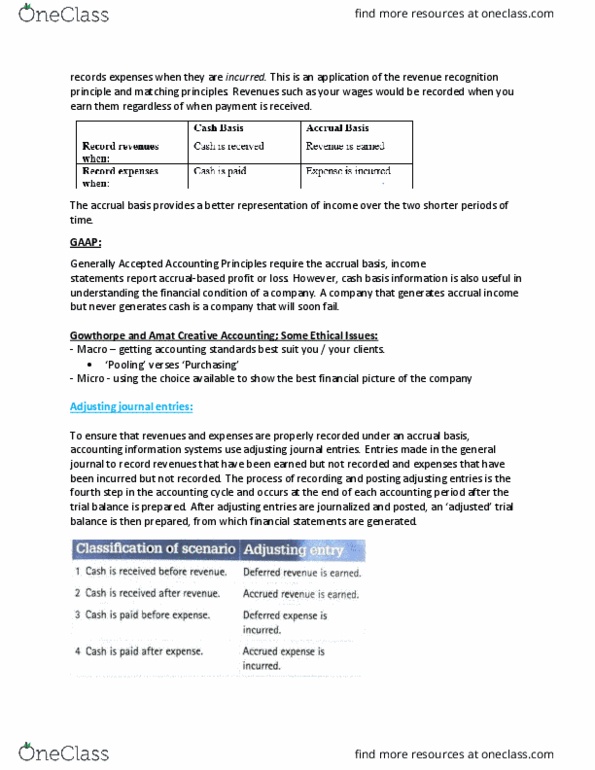

Describe how profit is measured and reported under the accrual and cash bases of accounting.

Dr are uses of funds

Cr are sources of funds

Expanded Transaction Analysis Model

Transaction Analysis

Basic accounting equation:

A = L + (S)E + R - E

(Rearranged) = add expenses to both sides

A + E = L + R + SE

Rules of Debit & Credit

Accrual & Cash Bases of Accounting

Main difference between is the timing of when revenues are recorded.

• The cash basis of accounting records revenues when cash is received and records expenses

when cash is paid.

• The accrual basis of accounting records revenues when they are earned and records expenses

when they are incurred.

Document Summary

Describe how profit is measured and reported under the accrual and cash bases of accounting. A = l + (s)e + r - e (rearranged) = add expenses to both sides. A + e = l + r + se. Requires the accrual basis, income statements report accrual-based profit or loss. However, cash basis information is also useful in understanding the financial condition of a company. A company that generates accrual income but never generates cash is a company that will soon fail. Identify the four major circumstances in which adjusting journal entries are necessary. To ensure revenues and expenses are properly recorded under an accrual basis, accounting information systems are adjusting journal entries. Adjusting journal entries are entries made in the general journal to record revenues that have been earned but not recorded and expenses that have been incurred but not recorded.