ACCT3321 Lecture Notes - Lecture 5: Defined Contribution Plan, Financial Statement, Profit Sharing

CHAPTER 9

Employee Benefits

Short-term employee benefits

- Employee benefits (other than termination benefits) that are expected to be settled

wholly before twelve months after the end of the annual reporting period in which

the employees render the related service

- Include payment for employment services as well as paid leave entitlements (sick

leave…)

- Non-monetary benefits fringe benefits health insurance, housing and motor

vehicles

-Payroll

oThe subsystem for regular recording and payment of employee benefits

oInvolves:

Recording the amount of wages or salaries for the pay period

Updating personnel records for the appointment of new employees

Updating personnel records for termination of employment contracts

… p3

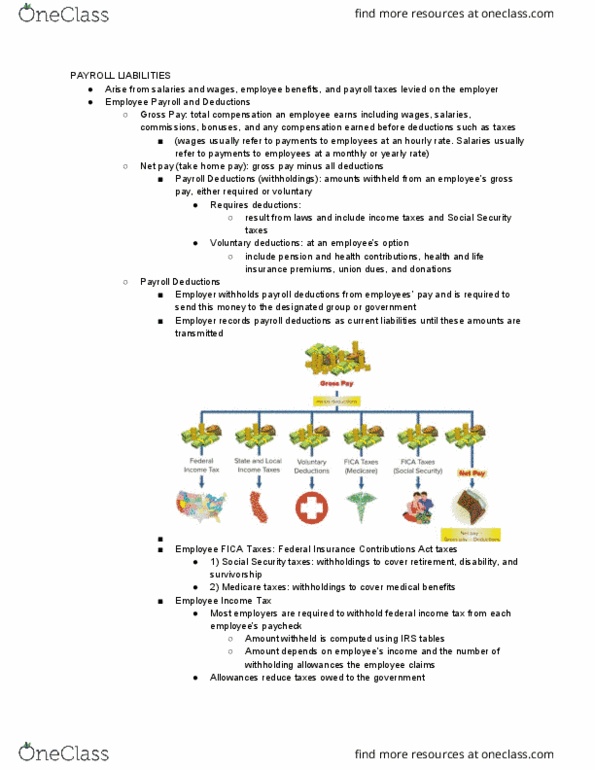

oemployers are typically required to deduct and withhold income tax from

employees’ wages and salaries employee received a payment that is net of

tax and the employer pays the amount of income tax deducted to the

authorities

oaccounting for the payroll – example 9.1

-Accrual of wages and salaries

oThe end of the payroll often differs from the end of the reporting period…

oExample 9.2

oDR Wages and salaries expense for the cost of employee benefits for the

remaining days

CR Accrued wages and salaries

-Short-term paid absences

oSome entities offer paid leave such as annual leave or short periods of

illness… maternity leave….

oEntitlements that are expected to be settled within 12 months after the end

of the reporting period

oNon-accumulating paid absences leave entitlements that the employee

may not carry forward to a future period

oAccumulating paid absences leave entitlements that the employee may

carry forward to a future period if unused in the current period Paragraph

15 of AASB 119

Vesting the employee is entitled, upon termination of employment,

to cash settle for any unused leave

Non-vesting the employee is not entitled to cash settlement of their

unused leave

oIf the leave is cumulative but non-vesting, it is possible that there will not be

a future settlement the sick leave must still be accrued throughout the

find more resources at oneclass.com

find more resources at oneclass.com

period of employment, because the employee remains entitled to the leave

while they remain employed, and as such there is no obligation

oExample 9.3 an annual adjustment was made to the provision for annual

leave

oExample 9.4 accounting for accumulating sick leave

-Profit sharing and bonus plans

oBonuses may be determined as a lump-sum amount or market based

measures

oParagraph 19 of AASB 119 entity to recognise profit sharing if:

The entity has a present legal or constructive obligation to make such

payments as a result of past events

A reliable estimate of the obligation can be made

a present obligation exists when, and only when, the entity has no

realistic alternative but to make the payments

oFigure 9.3 – components of remuneration

oMeasured at nominal (undiscounted) amount that the entity expects to pay

Post-employment benefits

- Are benefits, other than termination benefits, that are payable after completion of

employment, typically after the employee retires

- Superannuation plans, employee retirement plans and pension plans

- The employer makes payments (contributions) to a fund in respect of current

employees, which are available for the employee to access at a later date

- The fund, which is a separate entity invests the contributions and provides post-

employment benefits to the employees, who are members of the fund

-Defined contribution plans

oAn entity (employer) pays fixed contributions to a separate entity

(superannuation fund) on behalf of the employee

oNormally based on a percentage of the wages

oThe employer has no legal or constructive obligation to pay further

contributions if the fund does not hold sufficient assets to pay all the

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Employee benefits (other than termination benefits) that are expected to be settled wholly before twelve months after the end of the annual reporting period in which the employees render the related service. Include payment for employment services as well as paid leave entitlements (sick leave ) Non-monetary benefits fringe benefits health insurance, housing and motor vehicles. Payroll: the subsystem for regular recording and payment of employee benefits, involves: Recording the amount of wages or salaries for the pay period. Updating personnel records for the appointment of new employees. Updating personnel records for termination of employment contracts. Accrual of wages and salaries: the end of the payroll often differs from the end of the reporting period , example 9. 2, dr wages and salaries expense for the cost of employee benefits for the remaining days. Vesting the employee is entitled, upon termination of employment, to cash settle for any unused leave.