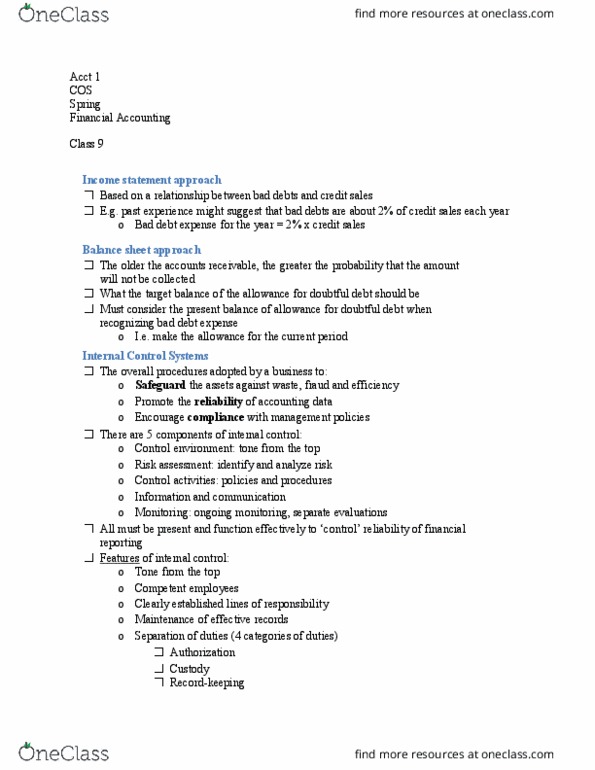

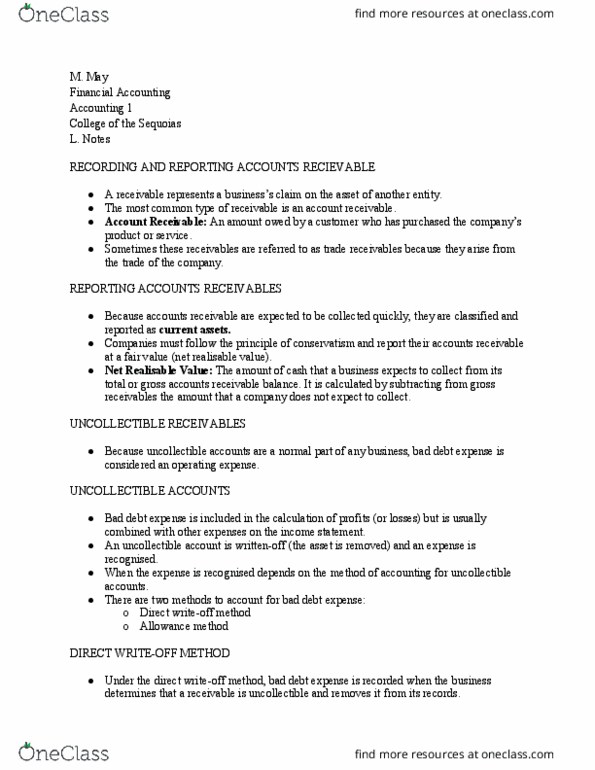

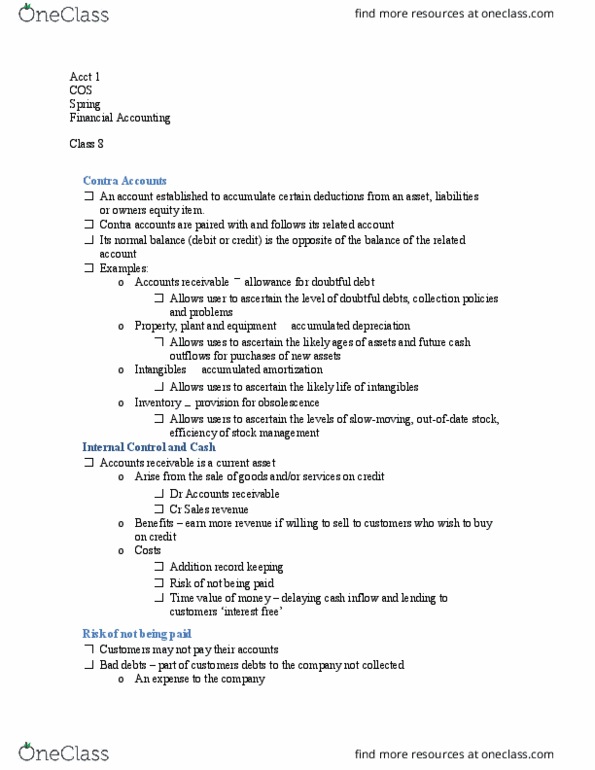

ACCT 001 Lecture Notes - Lecture 13: Subledger, Debits And Credits, Accounts Receivable

Document Summary

Get access

Related Documents

Related Questions

| Narrative andInstructions | |||||||

| Rockford Corporation is awholesale plumbing supply distributor. The corporation wasorganized | |||||||

| in 1981, under the laws of theState of Illinois, with an authorized capitalization of 10,000shares | |||||||

| of no-par common stock with astated value of $18 per share. The common stock is sold overthe | |||||||

| the counter in the local area.You have been hired as of Thursday, December 25, 2014, to replacethe | |||||||

| controller, who has resigned.As controller, you are responsible for the corporation'saccounting | |||||||

| recrods, preparation of thefinancial statements, safeguarding the corporate assets, andproviding | |||||||

| management with financialinformation to set prices and to monitor and controloperations. | |||||||

| Rockford Corporation closesits books annually on December 31 but prepares financialstatements | |||||||

| quarterly. Adjusting entriesare posted to the general ledger only at year-end; at the end ofthe | |||||||

| first, second, and thirdquarter the adjustments are entered only on a work sheet, not inthe general | |||||||

| ledger. Therefore, theadjusting entries to be recorded on December 31 are annualadjustments that | |||||||

| you must journalize and thepost to the general ledger accounts before preparing thefinancial | |||||||

| statements. | |||||||

| Rockford Corporation maintainsa perpetual inventory system and takes a physical count eachyear | |||||||

| to adjust the inventorycarrying amount. Purchases are recorded at the gross amount(discounts | |||||||

| taken are recognized at thedate of payment) of the supplier's invoice, and the terms varywith | |||||||

| each supplier. Sales onaccount are subject to terms of 1/10, n/30. Discounts are taken andgranted | |||||||

| only when the terms are met.The cost of all inventory sold in December was 65% of the salesprice. | |||||||

| The corporation uses thefollowing journals and ledgers: | |||||||

| Journals | |||||||

| 1. A sales journal (S) - torecord sales of merchandise on account. | |||||||

| 2. A purchase journal (P)- torecord purchases of merchandise on account. | |||||||

| 3. A cash receipts journal(CR) - to record all cash receipts. | |||||||

| 4. A cash disbursementsjournal (CD) - to record all cash payments. | |||||||

| 5. A general journal (J) - torecord all transacitons that cannot be recorded in the otherjournals. | |||||||

| Ledgers | |||||||

| 1. A general ledger | |||||||

| 2. An accounts receivablesubsidiary ledger. | |||||||

| 3. An accounts payablesubsidiary ledger. | |||||||

| In recording salestransactions, each sale should be posted on the day of the saledirectly to the | |||||||

| customer's account in thesubsidiary ledger, using the invoice number as the postingreference | |||||||

| number in the subsidiaryaccount. Also, cash receipts from customers should be posted tothe | |||||||

| subsidiary ledger on the daythey are received. The purchase order number should be used as | |||||||

| the posting reference numberin the subsidiary ledger for purchases on account fromsuppliers. | |||||||

| Purchases from suppliers andpayments to them should be posted daily. All other individualposting | |||||||

| may be made weekly or at themonth-end. Account numbers should be used as posting reference | |||||||

| numbers in the journals.Officers and office personnel are salaried employees and are paidmonthly | |||||||

| on the last day of each month.The delivery truck drivers and warehouse employees are hourlywage | |||||||

| employees and are paidbiweekly. Each biweekly pay period ends Friday. On the followingMonday | |||||||

| you assistants provide youwith a payroll summary from which you prepare general journalentries | |||||||

| to record the biweekly payrolland the employer's taxes on the payroll. The biweeklyemployees' | |||||||

| paychecks are distributed onthe following day (Tuesday). | |||||||

| The January 1, 2014, balancesappear in the general ledger accounts as well as the Noverber 30,2014, | |||||||

| balances, for those accountswhose balances have changed. All transacitons affecting thenon- | |||||||

| current accounts from January1, 2014, through Noverber 30, 2014, with explanations, appearin | |||||||

| these accounts to facilitatethe preparation of the statement of cash flows. | |||||||

| Subsidiary ledger accountbalances as of Noverber 30, 2014, are as follows: | |||||||

| Accounts Receivable | Acct No | Amount | |||||

| Boecker Builders | 117 | 62,920 | |||||

| The Potts Company | 122 | 46,300 | |||||

| Swanson BrothersContruction | 133 | 22,590 | |||||

| A & B Hardware | 143 | - | |||||

| Trudy's Plumbing | 155 | 15,500 | |||||

| Coconino Contractors Inc | 160 | 28,700 | |||||

| Rankin Plumbing Corp | 166 | 74,350 | |||||

| Beverly's BuildingProducts | 175 | 13,600 | |||||

| Bilder Construction Co | 180 | 48,900 | |||||

| Iwanaga Plumbing andHeating | 190 | 5,800 | |||||

| Total | 318,660 | ||||||

| Accounts Payable | Acct No | Amount | |||||

| Phoenix Plastics | 14 | 19,280 | |||||

| Business Basics Inc | 16 | - | |||||

| Edward's PlumbingSuppliers | 18 | 20,050 | |||||

| DeKalb Transport | 20 | - | |||||

| Oxenford Copperworks | 35 | 28,700 | |||||

| Smith Pipe Co | 39 | 37,700 | |||||

| Ron & Rod's PlumbingProducts | 44 | 14,850 | |||||

| Khatan Steel Corp | 57 | 12,000 | |||||

| Total | 132,580 | ||||||

| The transactions throughDecember 23 have already been recorded by the former controller.You | |||||||

| are to begin your work byentering the transaction of December 25 for the payment of cashto | |||||||

| repurchase stock. | |||||||

| Dec-14 | |||||||

| S | M | T | W | T | F | S | |

| 1 | 2 | 3 | 4 | 5 | 6 | ||

| 7 | 8 | 9 | 10 | 11 | 12 | 13 | |

| 14 | 15 | 16 | 17 | 18 | 19 | 20 | |

| 21 | 22 | 23 | 24 | 25 | 26 | 27 | |

| 28 | 29 | 30 | 31 | ||||

| December Transactions | |||||||

| December | |||||||

| 1 | Received a check in the amount of $22,364 fromSwanson Brothers Contruction in full | ||||||

| payment of invoice No. 1120 dated Novermber 26 inthe amount of $22,590. | |||||||

| 1 | Sold sewer and drainage pipe to Beverly's BuildingProducts on account, invoice No. 1201 | ||||||

| for $28850. | |||||||

| 2 | Purchased copper tubing and fittings from Edward'sPlumbing Supplies Inc. on account, | ||||||

| purchase order No. 315 for $32660, terms n/60. | |||||||

| 2 | Issued check No. 1580 for $28,700 to OxenfordCopperworks in settlement of the | ||||||

| balance owned on purchase order No. 280. | |||||||

| 3 | A court notice indicates that Iwanaga Plumbing andHeating is bankrupt and payment | ||||||

| of its account improbable; the president orders theaccount to be written off as a | |||||||

| bad debt (invoice No. 780). | |||||||

| 3 | Sold bathroom fixtures to Bilder Construction Co onaccount, invoice No. 1202 for | ||||||

| $47,700.00 | |||||||

| 4 | Received a check in the amount of $45,374 from thePotts Co in full payment of invoice | ||||||

| No. 1128 dated November 27 for $46,300. | |||||||

| 4 | Sold plumbing supplies and plastic pipe to CoconinoContractors Inc. on account, invoice | ||||||

| No. 1203 for $12,300. | |||||||

| 4 | Issued check No. 1581 for $720 to Standard Oil Co,in payment of gas, oil, and truck repair | ||||||

| from Tierney's Standard Service. | |||||||

| 5 | Issued check No. 1582 for $11,880 to Khatan SteelCorp. in full settlement of purchase order | ||||||

| No. 312 for $12,000. | |||||||

| 5 | Issued check No. 1583 for $12,054 to PhoenixPlastics in full payment of Phoenix's invoice | ||||||

| dated November 28 in the amount of $12,300, forpurchase order No. 313, terms 2/10, n/30. | |||||||

| 5 | Received a check in the amount of $72,863 fromRankin Plumbing Corp. in full payment | ||||||

| of invoice No. 1129 dated November 28 for$74,350. | |||||||

| 8 | Sold cast pipe to Trudy's Plumbing on account,invoice No. 1204 for $26,300. | ||||||

| 8 | Received a check in the amount of $28,700 fromCoconion Contractors, Inc. in full payment | ||||||

| of invoice No. 1091 dated October 20. | |||||||

| 8 | Purchased bathroom fixtures from Phoenix Plastics,on account, purchcase order No. 316 | ||||||

| for $56,800 terms 1/10, n/30. | |||||||

| 8 | Received a check in the amount of $29,600 fromBoecker Builders in partial payment of | ||||||

| balance outstanding covering invoice Nos. 1050 and1071. | |||||||

| 9 | The payroll summary for the biweekly pay periodended Friday, December 5 contained the | ||||||

| follwing information: | |||||||

| Delivery and warehouse wages | 4,860 | ||||||

| FICA taxes withheld | 410 | ||||||

| Federal income taxes withheld | 900 | ||||||

| State income taxes withheld | 190 | ||||||

| Net pay | 3,360 | ||||||

| Employer's payroll taxes: | |||||||

| FICA tax | 410 | ||||||

| Federal unemployment tax | - | ||||||

| State unemployment tax | - | ||||||

| Issued check No. 1584 for the amount of the net payand deposited it in the payroll bank | |||||||

| account. Individual payroll checks were thenpreppared for distributions to the biweekly | |||||||

| emplyees on Tuesday, December 9, 2014. | |||||||

| 9 | Issued check No. 1585 for $650 to Scooter Gordonfor lettering and sign painting on some | ||||||

| delivery trucks. | |||||||

| 9 | Issued check No. 1586 for $6,980 to PhoenixPlastics, in payment of Phoenix's invoice dated | ||||||

| November 12 in the amount of $6,980, our purchaseorder No. 299. | |||||||

| 10 | Issued check No. 1587 for $37,323 to Smith Pipe Coin full payment of their invoice dated | ||||||

| November 28, terms 1/15, n/30, our purchase orderNo. 314. | |||||||

| 10 | Received a check in the amount of $15,500 fromTrudy's Plumbing in full settlement of | ||||||

| invoice No. 1106 dated November 7. | |||||||

| 10 | Sold pipe, fixtures, and accessories to Trudy'sPlumbing on account, invoice No. 1205 for | ||||||

| $26,850.00 | |||||||

| 11 | Sold pumbing supplies and copper tubing to ThePotts Company on account, invoice No. | ||||||

| 1206 for $31,450. | |||||||

| 11 | Received a check in the amount of $33,320 fromBoecker Builders in full payment of invoice | ||||||

| No. 1071. | |||||||

| 11 | Cash sales to date totaled $10,232. | ||||||

| 12 | Received a check in the amount of $25,774 fromTrudy's Plumbing in payment of inoivce | ||||||

| No. 1204. | |||||||

| 12 | Sold plumbing fixtures and supplies to BoeckerBuilders, on account, invoice No. 1207 | ||||||

| for $24,730. | |||||||

| 15 | The Potts Co returned defective copper tubing thatis purchased on December 11. A credit | ||||||

| memo in the amount of $5680 is issued relative toinvoice No. 1206. The copper tubing | |||||||

| had a cost of $3692. | |||||||

| 15 | The defective copper tubing is returned to Edward'sPlumbing supplies, Inc. along with | ||||||

| a debit memo in the amount of $3692 in reduction ofpurchase order No. 315. | |||||||

| 15 | Issud check No. 1588 for $599 in payment ofNovember telephone bill to Northern | ||||||

| Illinois Communications. | |||||||

| 16 | Issued check No. 1589 in the amount of $12,360 inpayment of federal withholding taxes, | ||||||

| $10,573, and FICA taxes, $1787, payable on Novembersalaries and wages; The check is | |||||||

| remitted to the Winnebago County Bank as thedepository. | |||||||

| 16 | Issued check No. 1590 for $56,232 to PhoenixPlastics, Inc, in payment of purchase order | ||||||

| No. 316. | |||||||

| 17 | The president informs you that Bilder ConstructionCo agrees to convert the $48900 | ||||||

| overdue account receivable (invoice No. 1120) to a8% note due six months from today. | |||||||

| 17 | Purchased plumbing materials from Smith PipeCompany on account, purcase order No. | ||||||

| 317 for $,51,120 terms 1/15, n/60. | |||||||

| 17 | Sold drain tile, plastic pipe, and copper tubing toA & B Hardware on account, invoice No. | ||||||

| 1208 for $7,340. | |||||||

| 18 | Sold fixtures and materials to CoconinoContractors, Inc. on account, invoice No. 1209 for | ||||||

| $44,530. | |||||||

| 18 | An invoice in the amount of $1,021 was receivedfrom S. White Trucking Company for | ||||||

| freight on purchase order No. 317 and paid byissuing check No. 1591. | |||||||

| 18 | Received a check in the amount of $26,582 fromTrudy's Plumbing in payment of invoice | ||||||

| No. 1205. | |||||||

| 19 | Purchased office supplies from the Pen & Pad,issuing check No. 1592 in the amount of | ||||||

| $1,460. (Note: Debit asset account). | |||||||

| 19 | Purchased a new Faith computer for $5600 fromBusiness Basics, Inc, purchase order | ||||||

| No, 318, paying $600 down through check No. 1593with the balance due in thirty days | |||||||

| (n/30). The computer has an estmated life of 4years with a salvage value of $2200. | |||||||

| 22 | Purchased bathroom and kitchen fixtures fromPhoenix Plastics, on account, purchase | ||||||

| order No. 319 for $48,330, terms 1/10, n/30. | |||||||

| 22 | Received a bill from DeKalb Transport for $2580 forfreight costs incurred during the last 30 | ||||||

| days, terms n/30. | |||||||

| 23 | The payroll summary for the biweekly pay periodended Friday, December 19 contained the | ||||||

| follwing information: | |||||||

| Delivery and warehouse wages | 5,770 | ||||||

| FICA taxes withheld | 415 | ||||||

| Federal income taxes withheld | 1,067 | ||||||

| State income taxes withheld | 225 | ||||||

| Net pay | 4,063 | ||||||

| Employer's payroll taxes: | |||||||

| FICA tax | 415 | ||||||

| Federal unemployment tax | - | ||||||

| State unemployment tax | - | ||||||

| Issued check No. 1594 for the amount of the net payand deposited it in the payroll bank | |||||||

| account. Individual payroll checks were thenprepared for distributions to the biweekly | |||||||

| emplyees on Tuesday, December 23. | |||||||

| NOTE: Transactions up to this point have beenrecorded. At this point you became | |||||||

| controller and are responsible for recordign allfurther transactions. | |||||||

| 25 | The board of directors voted to purchase 2,500shares of its own stock from stockholder | ||||||

| Dionne Schivone at $76 per share and issued checkNo. 1595 in payment. Stock repurchases | |||||||

| are recorded at cost. Rockford is purchasing theseshares because Ms. Schivone had been | |||||||

| a valuable employee. | |||||||

| 26 | The baord of directors declared a $1.25 per sharecash dividend payable on January 14 to | ||||||

| shareholders of record by the end of the day ofDecember 26. | |||||||

| 26 | The president informs you that Beverly's BuildingProducts agrees to convert the $13,600 | ||||||

| overdue accounts receivable (invoice No. 1119)balance to a 10% note due six months from | |||||||

| today. | |||||||

| 29 | A half-acre parcel of land adjacent to the buildingis acquired in exchange for 750 shares | ||||||

| of unissued common stock. The land has a fair valueof $58,400 and will be used | |||||||

| immediately as an outside storage lot and parkinglot. | |||||||

| 29 | An invoice in the amount of $1,860 is received fromWayne McManus, lawyer, for legal | ||||||

| services involved in the acquisition of theadjacent parcel of land; check No. 1596 is issued. | |||||||

| 29 | Sold pipe and plumbing materials to BoeckerBuilders on account, invoice No. 1210 for | ||||||

| $44,280 | |||||||

| 30 | Issued check No. 1597 in the amount of $3,500 tothe Northern Star for adverstisement run in | ||||||

| the home building supplement of December 13. | |||||||

| 30 | Issued check No. 1598 in the amount of $830 toStandard Oil Co. in payment of gas, oil, | ||||||

| and truck repairs from Standard Oil Co. (useFreight-out). | |||||||

| 30 | Purchased copper and cast iron pipe from OxenfordCopperworks on account, purchase | ||||||

| order No. 320 for $55,240, terms 1/10, n/30. | |||||||

| 30 | Check No. 1599 for $9,400 is issued to the bondsinking fund trustee, Chicago Trust Co., | ||||||

| for deposit in the sinking fund. (Use OtherAssets). | |||||||

| 30 | Sold plumbing supplies to Swanson BrothersConstruction on account, invoice No. 1211 | ||||||

| for $24,150. | |||||||

| 31 | Received a check for $24,730 from Boecker Buildersin payment of invoice No. 1207. | ||||||

| 31 | Issued check No. 1600 for $50,609 to Smith PipeCompany in payment of purchase order | ||||||

| No. 317. | |||||||

| 31 | The custodian of the petty cash fund submits thefollowing receipts for reimbursement | ||||||

| and reports a cash-on-hand count of $8. | |||||||

| Postage stampls used (supplies) | $38 | ||||||

| United Parcel (freight-out) | 23 | ||||||

| C.O.D postage (freight costs) | 51 | ||||||

| Christmas office decorations (Misc exp) | 30 | ||||||

| Check No. 1601 is issued and cashed to reimbursethe fund. | |||||||

| 31 | Sold an electric truck-lift to Leila Stierman Co.for $2600 cash. The original cost was | ||||||

| $7900 with salvage value of $900, a life of 10years, and accumulated depreciation | |||||||

| recorded through 12/31/13 is $4,550. Thestraight-line method is used. (Note: the | |||||||

| company follows the practice of recording a halfyear's depreciation in the year of | |||||||

| acquisition and a half year in the year ofdisposal.) First, bring the depreciation expense | |||||||

| up to date in the general journal. Then journalizethe entire entry for the sale in the cash | |||||||

| receipts journal. | |||||||

| 31 | Sold bathroom fixtures and plumbing supplies toTrudy's Plumbing on account, invoice | ||||||

| No. 1212 for $56370. | |||||||

| 31 | Because for some time the petty cash fund has beensmaller than required for monthly | ||||||

| expenditures, the fund is increased by $95 bycashing check No. 1602 and placing the | |||||||

| money in the petty cash fund. | |||||||

| 31 | The payroll summary for the monthly paid employeesin submitted so that December | ||||||

| checks can be distributed before the year-end; thedetails are as follows: | |||||||

| Office and administrative salaries | $43,900 | ||||||

| Federal income taxes withheld | 7,696 | ||||||

| State income taxes withheld | 1,517 | ||||||

| FICA taxes withheld | 3,120 | ||||||

| Net pay | $31,567 | ||||||

| Issued check No, 1603 for the amount of the net payand deposited it in the payroll bank | |||||||

| account. Individual payroll checks were preparedfor distribution to all monthly employees | |||||||

| by the end of the day. | |||||||

| Employer's payroll taxes: | |||||||

| FICA tax (all office and administrative) | $3,120 | ||||||

| Federal unemployment tax | 0 | ||||||

| State unemployment tax | 0 | ||||||

| 31 | Cash sale since December 12 total $42150. | ||||||

| Instructions | |||||||

| 1 | Make the entries in the appropriate journal forDecember 25 through December 31. | ||||||

| (adjusting entries are recorded in generaljournal) | |||||||

| 2 | Post any amounts to be posted as individual amountsfrom journals to the general ledger | ||||||

| and update the receivable and payable subsidiaryledger accounts. | |||||||

| (only a few entries are posted for Dec, e.g.,account receivable. Please post all other entries) | |||||||

| 3 | Foot and cross-foot the columnar journals andcomplete the month-end postings of all | ||||||

| books of orginal entry. | |||||||

On 1 July 2017, Panda Ltd acquired all the issued shares ofSmarty Ltd. Panda Ltd paid $250,000 more than the equity itacquired in the fair value of Smarty Ltdâs net assets. At the dateof acquisition, the shareholderâs equity of S

On 1 July 2017, Panda Ltd acquired all the issued shares ofSmarty Ltd. Panda Ltd paid $250,000 more than the equity itacquired in the fair value of Smarty Ltdâs net assets. At the dateof acquisition, the shareholderâs equity of Smarty Ltd was asfollows.

$

Share capital

100,000

Retained earnings

175,000

Total

275,000

All the assets and liabilities of Smarty Ltd were recorded atamounts equal to their fair values at the acquisition date, exceptfor some assets detailed below.

Remaining useful life

Cost

Carrying amount

Fair value

$

$

$

Plant

5 years

180,000

90,000

120,000

Computer equipment

5 years

90,000

40,000

60,000

Required:

Prepare the acquisition analysis at 1 July 2017.

Prepare the consolidation worksheet entries for Panda Ltdâs groupat 1 July 2017.

Prepare the consolidation worksheet entries for Panda Ltdâs groupat 30 June 2018.

Question 1

Max. marks allocated

Acquisition analysis

3

Consolidation entries at 1 July 2017

6

Consolidation entries at 30 June 2018

10

Presentation

1

Total

20

Question 2 [35 marks]

Topic 2: Consolidation: Intra-group transactions

On 1 July 2015, Ping Pong Ltd acquired all the issued shares ofSing Song Ltd. At the date of acquisition, the shareholdersâ equityof Sing Song Ltd consisted of share capital $120,000; generalreserve $25,000 and retained earnings $55,000. The identifiable netassets of Sing Song Ltd were recorded at amounts equal to theirfair values, except for the following assets:

Carrying amount

Fair value

$

$

Land

100,000

130,000

Inventories

78,500

86,100

Machinery (cost $86,000)

52,000

56,000

Vehicles (cost $58,000)

47,000

53,000

The assets of Sing Song Ltd at acquisition date includedgoodwill recorded at $15,000 arising from a business combinationtransaction in 2011. As at the date of acquisition, the vehiclesand machinery were expected to have a further useful life of 6 and8 years respectively, with benefits to be received evenly overthose periods. Inventories on hand on 1 July 2015 was all sold by31 January 2016. The land owned at 1 July 2015 was sold inSeptember 2016 for $150,000. The machinery on hand at 1 July 2015was sold on 1 January 2018 for $38,000.

Adjustments for the differences between carrying amount and fairvalues of assets and liabilities on hand at acquisition date arerecognised on consolidation. When assets are sold or derecognised,any related valuation reserves are transferred to retainedearnings.

At 1 July 2015, Sing Song Ltd owned but had not recorded aninternally generated brand name, an identifiable asset included aspart of the business combination transaction. This brand name wasconsidered by Ping Pong Ltd to have a fair value of $29,000 and anindefinite useful life. An impairment test conducted with respectto the brand name on 30 June 2018 concluded that its recoverableamount at that date was $2,000 less than its carrying amount.

In June 2017, Sing Song Ltd paid a share dividend worth $20,000from the general reserve on hand at 1 July 2015.

The trial balances of both companies at 30 June 2018 showed thefollowing balances:

Ping Pong Ltd

Sing Song Ltd

Dr ($)

Cr ($)

Dr ($)

Cr ($)

Sales revenue

450,000

320,000

Dividend revenue

17,000

-

Other income

11,400

17,000

Proceeds on sale of equipment

18,000

-

Proceeds on sale of machinery

-

38,000

Cost of sales

210,000

192,550

Income tax expense

30,000

32,000

Depreciation and other expenses

39,000

36,000

Carrying amount of equipment sold

21,000

-

Carrying amount of machinery sold

-

30,500

Dividend paid

10,000

5,000

Dividend declared

20,000

12,000

Transfer to general reserve

10,000

5,000

Share capital

200,000

140,000

General reserve

35,000

10,000

Retained earnings (1 July 2017)

51,300

67,500

Accounts payable

69,500

36,000

Loan payable (due 30 June 2022)

25,000

15,000

Dividend payable

20,000

12,000

Provisions

12,500

9,300

Current tax liability

43,000

34,000

Deferred tax liability

11,800

5,000

Accumulated depreciation-vehicles

16,400

60,000

Accumulated depreciation-equipment

-

34,500

8%Debentures (matures 30 June 2021)

25,000

-

Cash

2,500

1,250

Receivables

27,000

13,000

Inventories

39,700

24,500

Other current assets

15,200

8,200

Deferred tax assets

7,500

3,500

Vehicles

88,000

158,000

Equipment

-

42,000

Land

140,000

180,000

Financial assets

68,000

14,800

Goodwill

28,000

15,000

Shares in Sing Song Ltd

250,000

-

Debentures in Ping Pong Ltd

-

25,000

1,005,900

1,005,900

798,300

798,300

Additional information:

On 1 January 2018, Ping Pong Ltd sold an item of equipment toSing Song Ltd for $18,000. The equipment had a carrying amount atthe date of sale of $21,000. Both companies depreciate equipment at20% on a straight line basis.

On 1 May 2017, Sing Song Ltd sold a machine to Ping Pong Ltd for$7,800. The machine had a carrying amount of $7,000 at the date ofsale. Ping Pong Ltd recorded the machine as inventories. Theinventories item was sold to an external party in November 2017 for$8,200.

All interests on the 8% debentures has been paid and brought toaccount in the records of both companies.

During the 2017-2018 financial year, Ping Pong Ltd sold inventoriesto Sing Song Ltd for $75,000. The cost of these inventories to SingSong Ltd was $70,000. Of these inventories, 25% is still on hand at30 June 2018.

The transfer to the general reserve recorded by Sing Song Ltd inthe current year was from retained earnings recorded at 1 July2015.

The tax rate is 30%.

Required:

Prepare an acquisition analysis.

Prepare the consolidation worksheet entries necessary to preparethe consolidated financial statements for the year ending 30 June2018 for the group comprising Ping Pong Ltd and Sing Song Ltd.

Note: you are not required to prepare the consolidationworksheet and the consolidated financial statements.

marty Ltd was as follows.

$ | |

Share capital | 100,000 |

Retained earnings | 175,000 |

Total | 275,000 |

All the assets and liabilities of Smarty Ltd were recorded atamounts equal to their fair values at the acquisition date, exceptfor some assets detailed below.

Remaining useful life | Cost | Carrying amount | Fair value | |

$ | $ | $ | ||

Plant | 5 years | 180,000 | 90,000 | 120,000 |

Computer equipment | 5 years | 90,000 | 40,000 | 60,000 |

Required:

Prepare the acquisition analysis at 1 July 2017.

Prepare the consolidation worksheet entries for Panda Ltdâsgroup at 1 July 2017.

Prepare the consolidation worksheet entries for Panda Ltdâsgroup at 30 June 2018.

Question 1 | Max. marks allocated |

Acquisition analysis | 3 |

Consolidation entries at 1 July 2017 | 6 |

Consolidation entries at 30 June 2018 | 10 |

Presentation | 1 |

Total | 20 |

Question 2 [35 marks]

Topic 2: Consolidation: Intra-grouptransactions

On 1 July 2015, Ping Pong Ltd acquired all the issued shares ofSing Song Ltd. At the date of acquisition, the shareholdersâ equityof Sing Song Ltd consisted of share capital $120,000; generalreserve $25,000 and retained earnings $55,000. The identifiable netassets of Sing Song Ltd were recorded at amounts equal to theirfair values, except for the following assets:

Carrying amount | Fair value | |

$ | $ | |

Land | 100,000 | 130,000 |

Inventories | 78,500 | 86,100 |

Machinery (cost $86,000) | 52,000 | 56,000 |

Vehicles (cost $58,000) | 47,000 | 53,000 |

The assets of Sing Song Ltd at acquisition date includedgoodwill recorded at $15,000 arising from a business combinationtransaction in 2011. As at the date of acquisition, the vehiclesand machinery were expected to have a further useful life of 6 and8 years respectively, with benefits to be received evenly overthose periods. Inventories on hand on 1 July 2015 was all sold by31 January 2016. The land owned at 1 July 2015 was sold inSeptember 2016 for $150,000. The machinery on hand at 1 July 2015was sold on 1 January 2018 for $38,000.

Adjustments for the differences between carrying amount and fairvalues of assets and liabilities on hand at acquisition date arerecognised on consolidation. When assets are sold or derecognised,any related valuation reserves are transferred to retainedearnings.

At 1 July 2015, Sing Song Ltd owned but had not recorded aninternally generated brand name, an identifiable asset included aspart of the business combination transaction. This brand name wasconsidered by Ping Pong Ltd to have a fair value of $29,000 and anindefinite useful life. An impairment test conducted with respectto the brand name on 30 June 2018 concluded that its recoverableamount at that date was $2,000 less than its carrying amount.

In June 2017, Sing Song Ltd paid a share dividend worth $20,000from the general reserve on hand at 1 July 2015.

The trial balances of both companies at 30 June 2018 showed thefollowing balances:

Ping Pong Ltd | Sing Song Ltd | |||

Dr ($) | Cr ($) | Dr ($) | Cr ($) | |

Sales revenue | 450,000 | 320,000 | ||

Dividend revenue | 17,000 | - | ||

Other income | 11,400 | 17,000 | ||

Proceeds on sale of equipment | 18,000 | - | ||

Proceeds on sale of machinery | - | 38,000 | ||

Cost of sales | 210,000 | 192,550 | ||

Income tax expense | 30,000 | 32,000 | ||

Depreciation and other expenses | 39,000 | 36,000 | ||

Carrying amount of equipment sold | 21,000 | - | ||

Carrying amount of machinery sold | - | 30,500 | ||

Dividend paid | 10,000 | 5,000 | ||

Dividend declared | 20,000 | 12,000 | ||

Transfer to general reserve | 10,000 | 5,000 | ||

Share capital | 200,000 | 140,000 | ||

General reserve | 35,000 | 10,000 | ||

Retained earnings (1 July 2017) | 51,300 | 67,500 | ||

Accounts payable | 69,500 | 36,000 | ||

Loan payable (due 30 June 2022) | 25,000 | 15,000 | ||

Dividend payable | 20,000 | 12,000 | ||

Provisions | 12,500 | 9,300 | ||

Current tax liability | 43,000 | 34,000 | ||

Deferred tax liability | 11,800 | 5,000 | ||

Accumulated depreciation-vehicles | 16,400 | 60,000 | ||

Accumulated depreciation-equipment | - | 34,500 | ||

8%Debentures (matures 30 June 2021) | 25,000 | - | ||

Cash | 2,500 | 1,250 | ||

Receivables | 27,000 | 13,000 | ||

Inventories | 39,700 | 24,500 | ||

Other current assets | 15,200 | 8,200 | ||

Deferred tax assets | 7,500 | 3,500 | ||

Vehicles | 88,000 | 158,000 | ||

Equipment | - | 42,000 | ||

Land | 140,000 | 180,000 | ||

Financial assets | 68,000 | 14,800 | ||

Goodwill | 28,000 | 15,000 | ||

Shares in Sing Song Ltd | 250,000 | - | ||

Debentures in Ping Pong Ltd | - | 25,000 | ||

1,005,900 | 1,005,900 | 798,300 | 798,300 | |

Additional information:

On 1 January 2018, Ping Pong Ltd sold an item of equipment toSing Song Ltd for $18,000. The equipment had a carrying amount atthe date of sale of $21,000. Both companies depreciate equipment at20% on a straight line basis.

On 1 May 2017, Sing Song Ltd sold a machine to Ping Pong Ltd for$7,800. The machine had a carrying amount of $7,000 at the date ofsale. Ping Pong Ltd recorded the machine as inventories. Theinventories item was sold to an external party in November 2017 for$8,200.

All interests on the 8% debentures has been paid and brought toaccount in the records of both companies.

During the 2017-2018 financial year, Ping Pong Ltd soldinventories to Sing Song Ltd for $75,000. The cost of theseinventories to Sing Song Ltd was $70,000. Of these inventories, 25%is still on hand at 30 June 2018.

The transfer to the general reserve recorded by Sing Song Ltd inthe current year was from retained earnings recorded at 1 July2015.

The tax rate is 30%.

Required:

Prepare an acquisition analysis.

Prepare the consolidation worksheet entries necessary to preparethe consolidated financial statements for the year ending 30 June2018 for the group comprising Ping Pong Ltd and Sing Song Ltd.

Note: you are not required to prepare the consolidationworksheet and the consolidated financial statements.