01:198:170 Lecture Notes - Lecture 11: Financial Statement, Step One, Income Statement

4 Apr 2017

School

Department

Course

Professor

9

01:198:170 Full Course Notes

Verified Note

9 documents

Document Summary

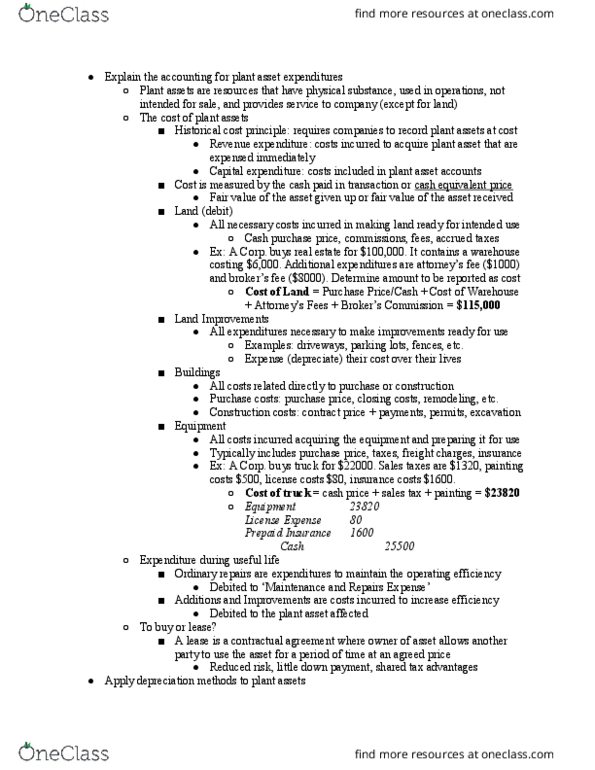

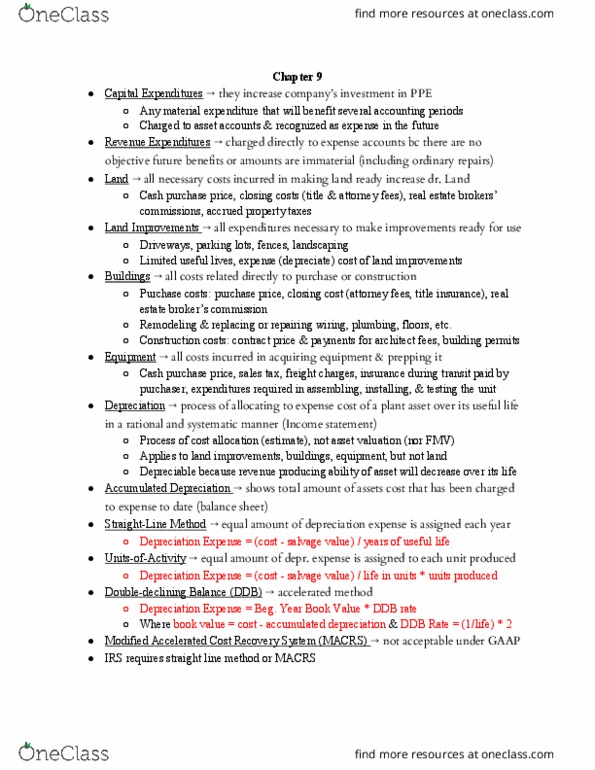

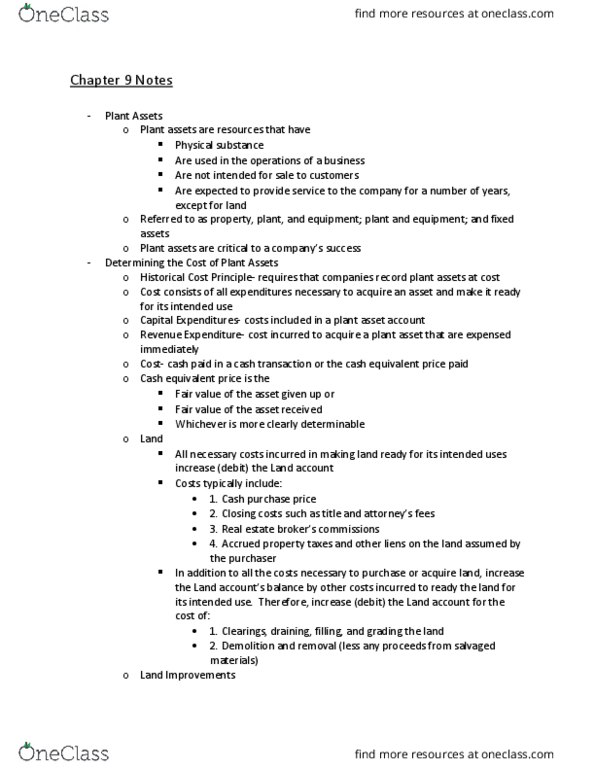

Chapter 9: plant assets, natural resources, and intangible assets. Plant assets- physical substance, not intended for sale, to be used by company for years. Record plant assets at cost; any cost that goes into the land. All costs that go into the land go into the land account. Examples: cash price of land, attorney fees, broker"s commission, etc. Land improvements: additions to the land that make the land usable. Things that depreciate in price as time passes by. Buildings- all the costs that deal with building/constructing or buying. Equipment- buying the equipment, freight costs, tax, insurance, etc. Cost- the initial price you purchased it for. Salvage value- value of asset at end of its life. Total units of activity- useful life in miles, hours worked, etc. Depreciable cost / useful life = annual depreciation expense. Depreciable cost / total uoa = depreciable cost per unit (depreciable cost per unit) *(total uoa per year (given)) = annual depreciation exp.