ECON 200 Lecture Notes - Lecture 4: Normal Good

18 Sep 2016

School

Department

Course

Professor

27

ECON 200 Full Course Notes

Verified Note

27 documents

Document Summary

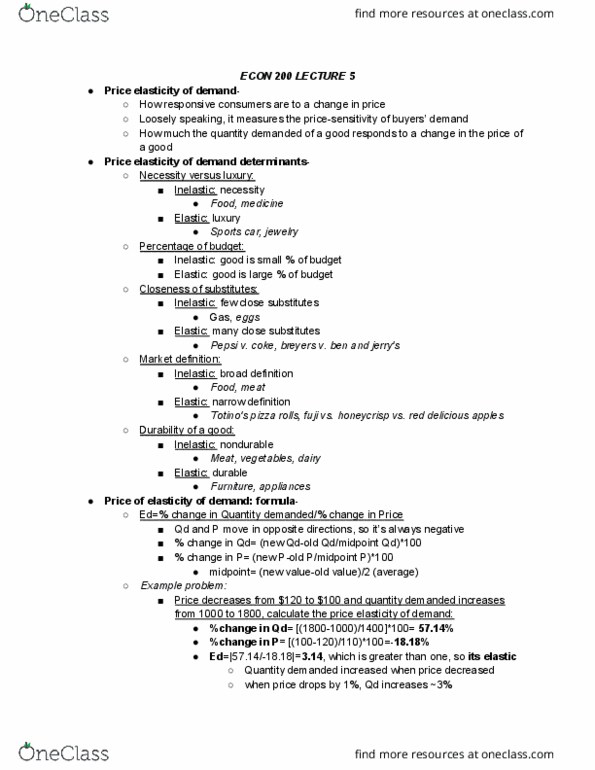

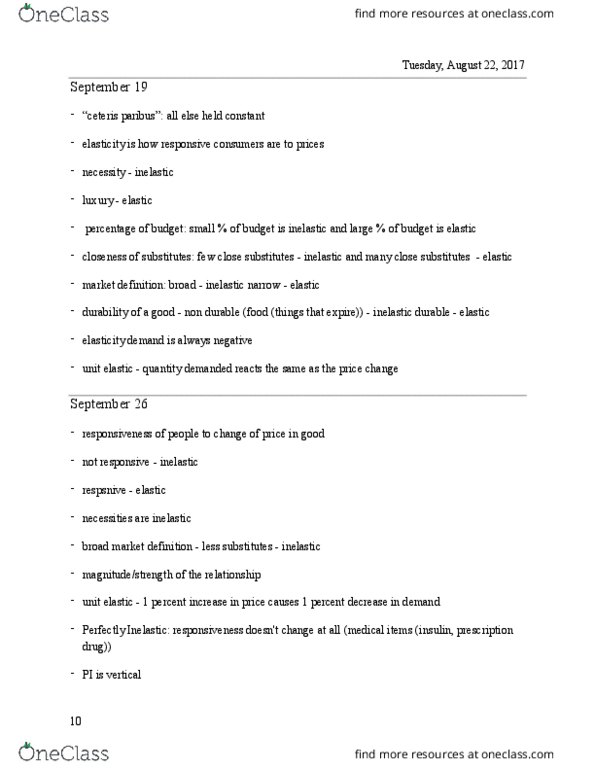

Elasticity: a measurement of the responsiveness of quantity demanded or quantity supplied to a change in one of its determinants. Price elasticity of demand: measures how much the quantity demanded responds to a change in price. Is elastic if the quantity demanded responds substantially to changes in the price. Is inelastic if the quantity demanded responds only slightly to changes in the price. Measures how willing consumers are to buy less of the good as its price rises. Availability of close substitutes: tend to have more elastic demand. Necessities versus luxuries: necessities tend to be inelastic, while luxuries tend to be elastic. Definition of the market: narrowly defined markets (i. e. ice cream) tend to be more elastic than broadly defined markets (i. e. food) Time horizon: goods tend to have more elastic demand over longer time horizons. Example: gasoline prices rising show a slight fall initially, but a more substantial change over time.