FNCE10001 Chapter Notes - Chapter 7: Net Present Value, Opportunity Cost

25 May 2018

School

Department

Course

Professor

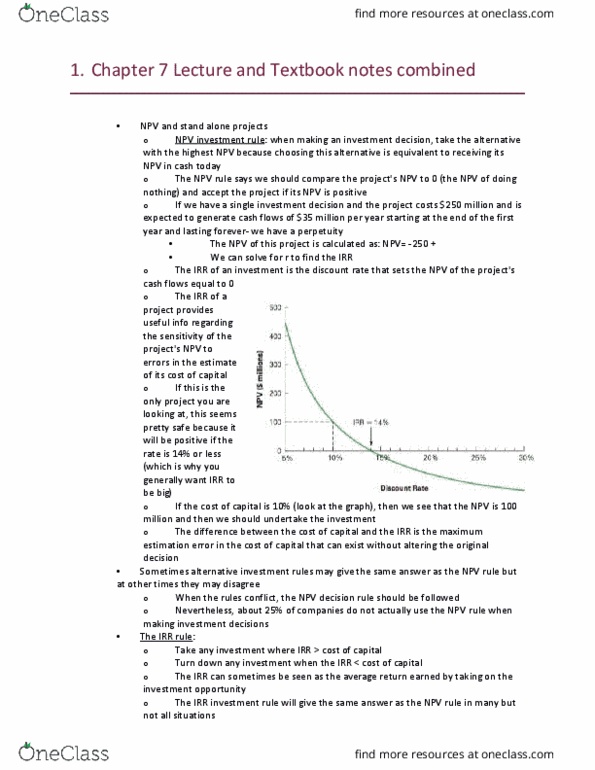

NPV profile and IRR:

NPV profile = graph of project's NPV over a range of discount rates

Difference between cost of capital and IRR is max estimation error in cost of capital that can exist

without altering the original decision

Alternatives rules vs NPV rule:

A wide variety of tools are applied in reality

Sometimes other investment rules give the same answer; other times they may disagree

When rules conflict, alternative rules lead to bad decisions

NPV and Stand

-

Alone Projects

Tuesday, 18 April 2017 6:39 PM

Principles of Finance Page 1

IRR Investment Rule: Take any investment opportunity where the IRR exceeds the opportunity cost

of capital (r)

Gives the correct answer in many, but not all, situations

IRR provides useful information in conjunction with the NPV rule

-

Indicates how sensitive the investment decision is to uncertainty in the cost of capital estimate

-

IRR rule only works for a stand

-

alone project if all negative cash flows precede its positive cash flows

Two IRRs are useful as bounds

-

No. of IRRs = no. of times project's cash flows change sign

-

IRR rule cannot be applied if there is more than one IRR

IRR rule provides no guidance when there is no IRR

Internal Rate of Return Rule

Tuesday, 18 April 2017 6:51 PM

Principles of Finance Page 2

Document Summary

Npv profile = graph of project"s npv over a range of discount rates. Difference between cost of capital and irr is max estimation error in cost of capital that can exist without altering the original decision. A wide variety of tools are applied in reality. Sometimes other investment rules give the same answer; other times they may disagree. When rules conflict, alternative rules lead to bad decisions. Irr investment rule: take any investment opportunity where the irr exceeds the opportunity cost of capital (r) Gives the correct answer in many, but not all, situations. Irr rule only works for a stand-alone project if all negative cash flows precede its positive cash flows. Irr provides useful information in conjunction with the npv rule. Indicates how sensitive the investment decision is to uncertainty in the cost of capital estimate. Irr rule cannot be applied if there is more than one irr.