FNCE10001 Chapter Notes - Chapter 8: Average Selling Price, Capital Budgeting, Accelerated Depreciation

25 May 2018

School

Department

Course

Professor

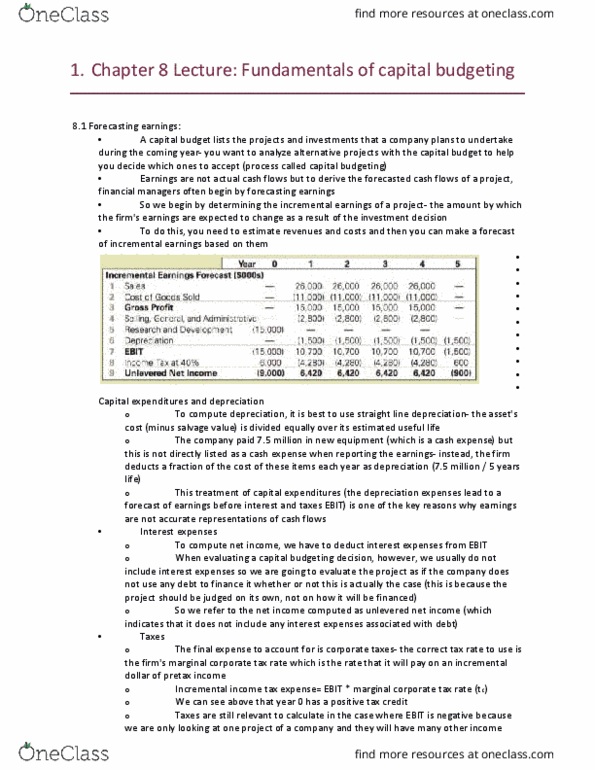

Capital budget = list of projects and investments a company plans to undertake in the coming year

Ultimate goal is to determine effect of decisions on firm's cash flows and evaluate NPV of cash

flows to assess consequences for the firm's value

-

Begins by determining the incremental earnings for a project (amount by which firm's earnings

are expected to change as a result of the investment decision)

-

Revenue and cost estimates

1.

Capital expenditures and depreciation

-

deduct straight

-

line depreciation

-

Interest expenses

-

do not include interest expenses

-

Income tax = EBIT x marginal corporate tax rate

Taxes

-

account for marginal corporate tax rate (tax rate it will pay on an incremental

dollar of pre

-

tax income

-

Unlevered net income = (revenue

-

costs

-

depreciation) x (1

-

tax rate)

Unlevered net income

-

net income that does not include any interest expenses

associated with debt

-

Incremental earnings forecast

2.

Opportunity costs

-

not using the resource in an alternative way

-

Cannibalisation = sales of a new product displace sales of an existing product

Project externalities

-

indirect effects that may change profits of other business activities

of the firm

-

Indirect effects on incremental earnings

3.

Fixed overhead expenses

-

expenses that affect many different areas of the corporation,

only include additional overhead expenses that arise because of the decision to take on

the project

-

Past research and development expenditures

-

Unavoidable competitive effects

-

Sunk costs and incremental earnings

4.

New products typically have lower sales initially, accelerate, plateau and then decline

-

Average selling price of a product and its cost of production will generally change over

time

-

Competition tends to reduce profit margins over time

-

Real

-

world complexities

5.

Capital budgeting = process of analysing alternative projects and deciding which ones to accept

Forecasting Earnings

Saturday, 29 April 2017 1:12 PM

Principles of Finance Page 1

Free cash flow = incremental effect of a project on the firm's available cash, separate from any

financing decisions

Depreciation is not included in cash flow forecast

○

Include actual cash cost of the asset when purchased

○

Capital expenditures and depreciation

-

NWC = current assets

-

current liabilities

○

= cash + inventory + receivables

-

payables

Most projects require the firm to invest in NWC

○

Need to maintain a minimum cash balance to meet unexpected expenditures, and

inventories of raw materials and finished product to accommodate production

uncertainties and demand fluctuations

○

Trade credit = net amount of firm's capital that is consumed as a result of credit

transactions = receivables

-

payables

○

Increases in NWC represent an investment that reduces cash available to the firm and

free cash flow

○

Net working capital

-

Calculating free cash flow from earnings:

Calculating free cash flow directly:

= (revenue

-

costs) x (1

-

tax rate)

-

capital expenditure

-

change in NWC + tax rate x

depreciation

Free cash flow = (revenues

-

costs

-

depreciation) x (1

-

tax rate) + depreciation

-

capital expenditure

-

change in NWC

Depreciation tax shield = tax savings that results from the ability to deduct depreciation = tax rate x

depreciation

Calculating the NPV:

Discount its free cash flow at appropriate cost of capital

NPV of project = sum of present values of each free cash flow

Determining Free Cash Flow and NPV

Saturday, 29 April 2017 5:38 PM

Principles of Finance Page 2

Document Summary

Capital budget = list of projects and investments a company plans to undertake in the coming year. Capital budgeting = process of analysing alternative projects and deciding which ones to accept. Ultimate goal is to determine effect of decisions on firm"s cash flows and evaluate npv of cash flows to assess consequences for the firm"s value. Begins by determining the incremental earnings for a project (amount by which firm"s earnings are expected to change as a result of the investment decision) Capital expenditures and depreciation - deduct straight-line depreciation. Interest expenses - do not include interest expenses. Taxes - account for marginal corporate tax rate (tax rate it will pay on an incremental dollar of pre-tax income. Income tax = ebit x marginal corporate tax rate. Unlevered net income - net income that does not include any interest expenses associated with debt. Unlevered net income = (revenue - costs - depreciation) x (1 - tax rate)