25300 Chapter Notes - Chapter 1-7: Tax Deduction, Sunk Costs, Capital Budgeting

Fundamentals of Business Finance Notes!

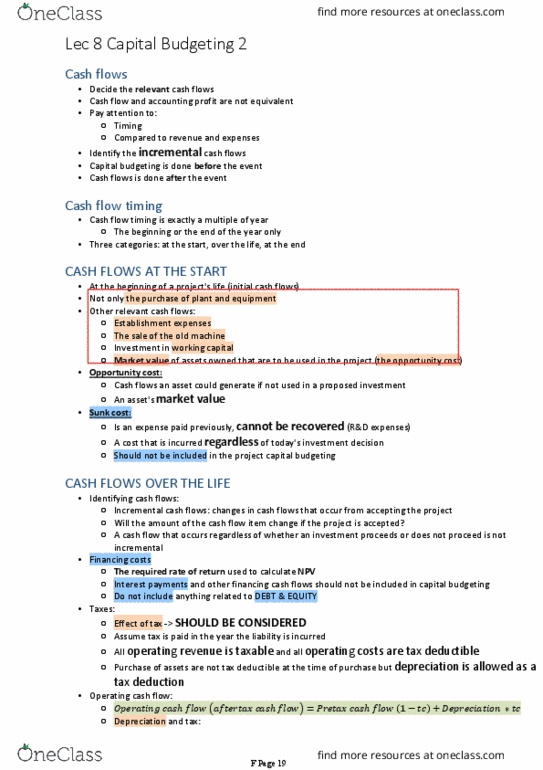

Capital Budgeting II

First step in capital budgeting is deciding on relevant cash flows.!

Incremental cash flows:!

-Cash flows at the start of the year (year 0)!

-Cash flows over the life (year 1 to year n)!

-Cash flows at the end (year n)!

Cash flow timing is exactly a multiple of year, occurring at the beginning or end of the year only!

Cash flows at the beginning:!

•Occur at the beginning on a project’s life!

•Includes purchase of plant and equipment (PPE)!

•Includes establishment expenses, proceeds from sale of old machinery, investment in working

capital, market value of assets owned that are to be used!

Opportunity cost - cash flows an asset could generate if not used in a proposed investment.!

Sunk cost - an expense paid previously by the firm and cannot be recovered, can be incurred

regardless of today’s investment decision!

Identifying cash flows:!

-Incremental cash flows are changes in cash flows that occur from accepting a project!

-A cash flow that occurs regardless of whether an investment proceeds or not is not incremental!

Financing costs - the required rate of return used to calculate NPV compensates owners and

creditors,; interest payments and financing cash flows are not included!

Taxes:!

-Considered in project evaluation, tax is paid in the year the liability is incurred!

-All operating revenue is taxable and all operating costs are tax deductible!

-Purchase of assets are not tax deductible at the time of purchase!

-Depreciation is allowed as a tax deduction!

Operating cash flow is an after-tax cash flow!

Depreciation:!

•Straight line - constant percentage of asset value written off each year (Most used)!

•Diminishing value - fixed percentage of the asset’s taxation book is written off each year!

•Book value of asset (WDV) - initial cost minus accumulated depreciation!

Accumulated depreciation represents sum of depreciation charged to income stamens in prior

years, the ATO sets the asset’s effective life!

Cash flows at the end:!

-One-off group of cash flows occur at the end of a project’s life!

find more resources at oneclass.com

find more resources at oneclass.com

-Assume the firm is restored to the situation before the project was accepted!

-Certain cash flows are recovered: investment in working capital and salvage value of assets!

Tax effect on asset sale:!

-The sale of an asset incurs a tax effect if the salvage value and book value are different!

-If the salvage value is greater than the book value the difference is taxable profit!

-If the salvage value is less than the book value the difference represents a loss!

-Tax on sale = (WDV - salvage value)TC!

Capital budgeting is part of the investment decision, excluding sunk costs and financing costs,

including incremental cash flows.$

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

First step in capital budgeting is deciding on relevant cash ows. Cash ows at the start of the year (year 0) Cash ows over the life (year 1 to year n) Cash ows at the end (year n) Cash ow timing is exactly a multiple of year, occurring at the beginning or end of the year only. Opportunity cost - cash ows an asset could generate if not used in a proposed investment. Sunk cost - an expense paid previously by the rm and cannot be recovered, can be incurred regardless of today"s investment decision. Incremental cash ows are changes in cash ows that occur from accepting a project. A cash ow that occurs regardless of whether an investment proceeds or not is not incremental. Financing costs - the required rate of return used to calculate npv compensates owners and creditors,; interest payments and nancing cash ows are not included.