ACCT 2000 Chapter : Acct Homework

Document Summary

Get access

Related Documents

Related Questions

Required information

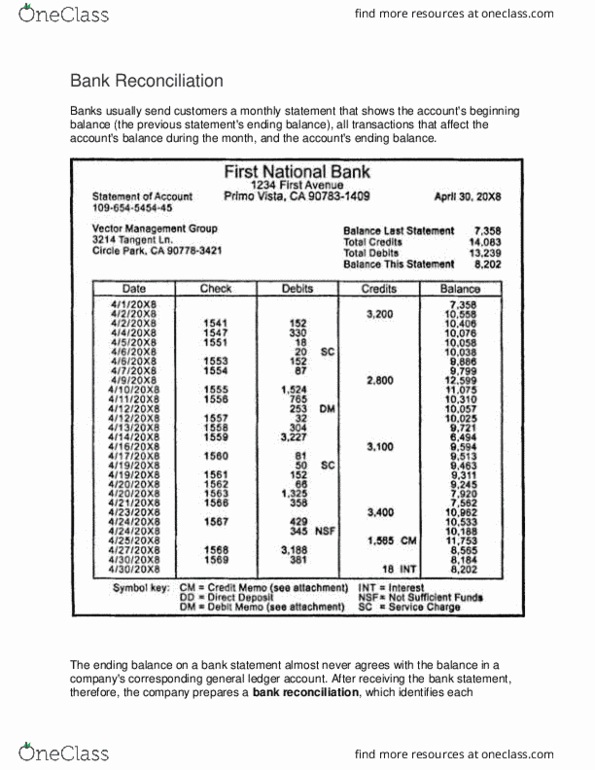

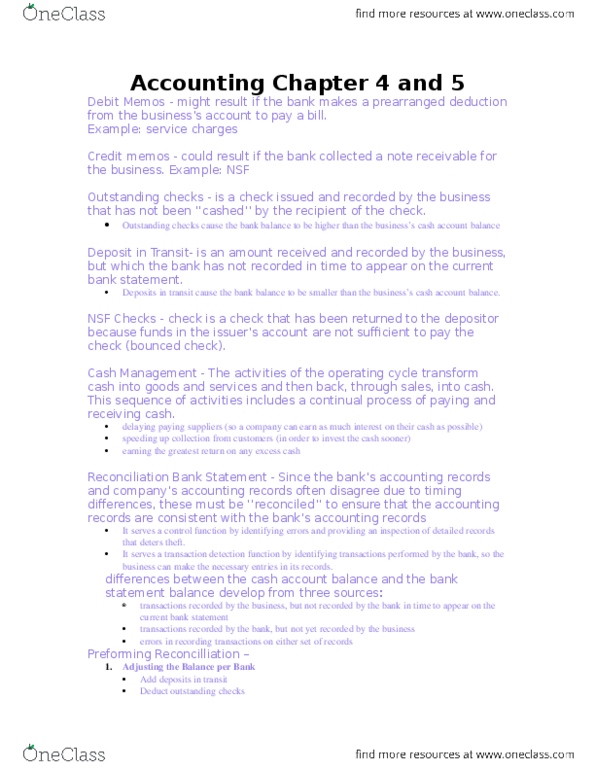

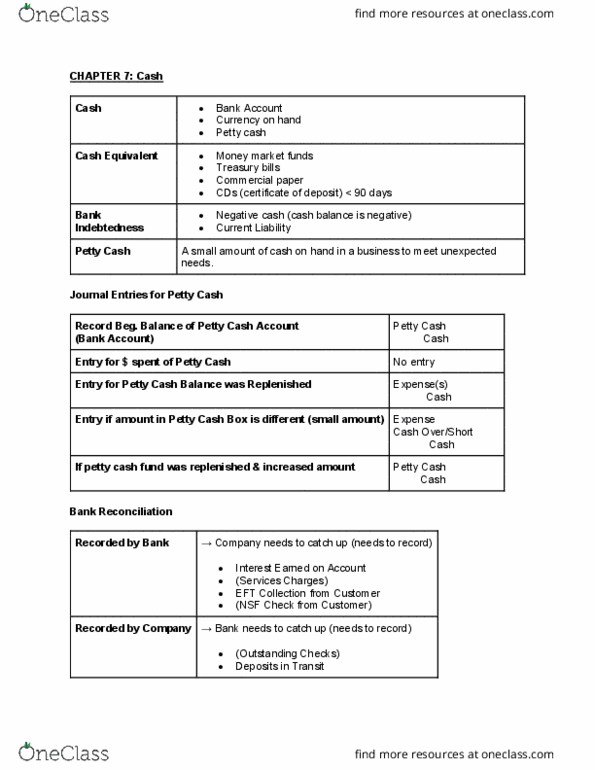

Problem 8-5A Preparing a bank reconciliation and recordingadjustments LO P3

[The following information applies to the questionsdisplayed below.]

Chavez Company most recently reconciled its bank statement andbook balances of cash on August 31 and it reported two checksoutstanding, No. 5888 for $1,026 and No. 5893 for $518. Thefollowing information is available for its September 30, 2017,reconciliation.

From the September 30 Bank Statement

| PREVIOUS BALANCE | TOTAL CHECKS AND DEBITS | TOTAL DEPOSITS AND CREDITS | CURRENT BALANCE |

| 19,500 | 9,768 | 11,581 | 21,313 |

| CHECKS AND DEBITS | DEPOSITS AND CREDITS | ||||||

| Date | No. | Amount | Date | Amount | |||

| 09/03 | 5888 | 1,026 | 09/05 | 1,114 | |||

| 09/04 | 5902 | 714 | 09/12 | 2,257 | |||

| 09/07 | 5901 | 1,813 | 09/21 | 4,376 | |||

| 09/17 | 628 | NSF | 09/25 | 2,308 | |||

| 09/20 | 5905 | 926 | 09/30 | 14 | IN | ||

| 09/22 | 5903 | 406 | 09/30 | 1,512 | CM | ||

| 09/22 | 5904 | 2,118 | |||||

| 09/28 | 5907 | 257 | |||||

| 09/29 | 5909 | 1,880 | |||||

From Chavez Companyâs Accounting Records

| Cash Receipts Deposited | ||||

| Date | Cash Debit | |||

| Sept. | 5 | 1,114 | ||

| 12 | 2,257 | |||

| 21 | 4,376 | |||

| 25 | 2,308 | |||

| 30 | 1,729 | |||

| 11,784 | ||||

| Cash Disbursements | ||||

| Check No. | Cash Credit | |||

| 5901 | 1,813 | |||

| 5902 | 714 | |||

| 5903 | 406 | |||

| 5904 | 2,079 | |||

| 5905 | 926 | |||

| 5906 | 1,042 | |||

| 5907 | 257 | |||

| 5908 | 390 | |||

| 5909 | 1,880 | |||

| 9,507 | ||||

| Cash | Acct. No. 101 | ||||

| Date | Explanation | PR | Debit | Credit | Balance |

| Aug. 31 | Balance | 17,956 | |||

| Sept. 30 | Total receipts | R12 | 11,784 | 29,740 | |

| 30 | Total disbursements | D23 | 9,507 | 20,233 | |

Additional Information

Check No. 5904 is correctly drawn for $2,118 to pay for computerequipment; however, the recordkeeper misread the amount and enteredit in the accounting records with a debit to Computer Equipment anda credit to Cash of $2,079. The NSF check shown in the statementwas originally received from a customer, S. Nilson, in payment ofher account. Its return has not yet been recorded by the company.The credit memorandum is from the collection of a $1,530 note forChavez Company by the bank. The bank deducted a $18 collection fee.The collection and fee are not yet recorded.

Journal Entry Worksheet

Record the entry related to the September 30 deposit, ifrequired.

Record the entry related to interest earned, if required.

Record the entry related to the note receivable and thecollection fee, if required.

Record the entry related to the outstanding checks, ifrequired.

Record the entry related to the NSF check, if required.

Record the entry related to the error on check 5904, ifrequired.

| |||||||||||||||||||||||||

|

*Enter debits before credits

Journal Entry Worksheet

Record the entry related to the September 30 deposit, ifrequired.

Record the entry related to interest earned, if required.

Record the entry related to the note receivable and thecollection fee, if required.

Record the entry related to the outstanding checks, ifrequired.

Record the entry related to the NSF check, if required.

Record the entry related to the error on check 5904, ifrequired.

| |||||||||||||||||||||||||

|

*Enter debits before credits

Journal Entry Worksheet

Record the entry related to the September 30 deposit, ifrequired.

Record the entry related to interest earned, if required.

Record the entry related to the note receivable and thecollection fee, if required.

Record the entry related to the outstanding checks, ifrequired.

Record the entry related to the NSF check, if required.

Record the entry related to the error on check 5904, ifrequired.

| |||||||||||||||||||||||||

|

*Enter debits before credits

Journal Entry Worksheet

Record the entry related to the September 30 deposit, ifrequired.

Record the entry related to interest earned, if required.

Record the entry related to the note receivable and thecollection fee, if required.

Record the entry related to the outstanding checks, ifrequired.

Record the entry related to the NSF check, if required.

Record the entry related to the error on check 5904, ifrequired.

| |||||||||||||||||||||||||

|

*Enter debits before credits

Journal Entry Worksheet

Record the entry related to the September 30 deposit, ifrequired.

Record the entry related to interest earned, if required.

Record the entry related to the note receivable and thecollection fee, if required.

Record the entry related to the outstanding checks, ifrequired.

Record the entry related to the NSF check, if required.

Record the entry related to the error on check 5904, ifrequired.

| |||||||||||||||||||||||||

|

*Enter debits before credits

Journal Entry Worksheet

Record the entry related to the September 30 deposit, ifrequired.

Record the entry related to interest earned, if required.

Record the entry related to the note receivable and thecollection fee, if required.

Record the entry related to the outstanding checks, ifrequired.

Record the entry related to the NSF check, if required.

Record the entry related to the error on check 5904, ifrequired.

| |||||||||||||||||||||||||

|

*Enter debits before credits

Chavez Company most recently reconciled its bank statement and book balances of cash on August 31 and it reported two checks outstanding, No. 5888 for $1,065 and No. 5893 for $519. The following information is available for its September 30, 2017, reconciliation.

From the September 30 Bank Statement

| PREVIOUS BALANCE | TOTAL CHECKS AND DEBITS | TOTAL DEPOSITS AND CREDITS | CURRENT BALANCE |

| 20,000 | 9,775 | 11,705 | 21,930 |

| CHECKS AND DEBITS | DEPOSITS AND CREDITS | ||||||

| Date | No. | Amount | Date | Amount | |||

| 09/03 | 5888 | 1,065 | 09/05 | 1,168 | |||

| 09/04 | 5902 | 703 | 09/12 | 2,263 | |||

| 09/07 | 5901 | 1,843 | 09/21 | 4,367 | |||

| 09/17 | 644 | NSF | 09/25 | 2,382 | |||

| 09/20 | 5905 | 917 | 09/30 | 21 | IN | ||

| 09/22 | 5903 | 377 | 09/30 | 1,504 | CM | ||

| 09/22 | 5904 | 2,133 | |||||

| 09/28 | 5907 | 222 | |||||

| 09/29 | 5909 | 1,871 | |||||

From Chavez Companyâs Accounting Records

| Cash Receipts Deposited | ||||

| Date | Cash Debit | |||

| Sept. | 5 | 1,168 | ||

| 12 | 2,263 | |||

| 21 | 4,367 | |||

| 25 | 2,382 | |||

| 30 | 1,713 | |||

| 11,893 | ||||

| Cash Disbursements | ||||

| Check No. | Cash Credit | |||

| 5901 | 1,843 | |||

| 5902 | 703 | |||

| 5903 | 377 | |||

| 5904 | 2,091 | |||

| 5905 | 917 | |||

| 5906 | 966 | |||

| 5907 | 222 | |||

| 5908 | 405 | |||

| 5909 | 1,871 | |||

| 9,395 | ||||

| Cash | Acct. No. 101 | ||||

| Date | Explanation | PR | Debit | Credit | Balance |

| Aug. 31 | Balance | 18,416 | |||

| Sept. 30 | Total receipts | R12 | 11,893 | 30,309 | |

| 30 | Total disbursements | D23 | 9,395 | 20,914 | |

Additional Information

Check No. 5904 is correctly drawn for $2,133 to pay for computer equipment; however, the recordkeeper misread the amount and entered it in the accounting records with a debit to Computer Equipment and a credit to Cash of $2,091. The NSF check shown in the statement was originally received from a customer, S. Nilson, in payment of her account. Its return has not yet been recorded by the company. The credit memorandum is from the collection of a $1,520 note for Chavez Company by the bank. The bank deducted a $16 collection fee. The collection and fee are not yet recorded.

2. Prepare the journal entries to adjust the book balance of cash to the reconciled balance. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)