ACCT20200 Chapter 3: Section 3.5

Document Summary

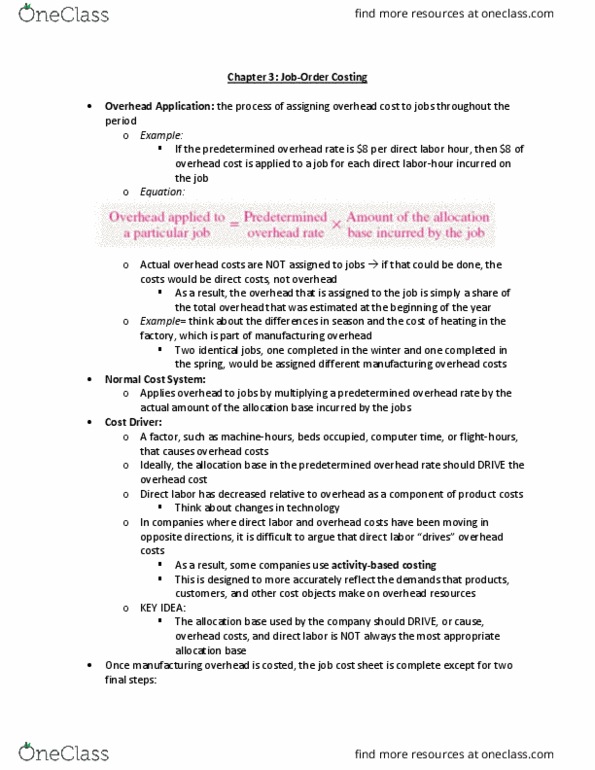

Overhead cost applied in work in process will generally differ from the amount of overhead cost actually incurred: actual does not equal applied moh. However, this is not always true because: Much of the overhead often consists of fixed costs that do not change as the number of machine-hours incurred goes up or down. Spending on overhead items may or may not be under control: costs may be more or less than expected depending on the individuals responsible for controlling overhead. If applied moh < actual moh, then overhead is underapplied. If applied moh > actual moh, the overhead is overapplied. ** when the allocation base is dollars, the predetermined overhead rate is expressed as a percentage of the allocation base ** Another way of looking at overapplied and underapplied moh: transactions: Debit entries to moh account = actual overhead costs. Credit entries to moh account = applied overhead costs: as a result: