Pricing

Log in

Sign up

Home

Homework Help

Study Guides

Class Notes

Textbook Notes

Textbook Solutions

Booster Classes

Blog

Home

Textbook Notes

300,000

US

110,000

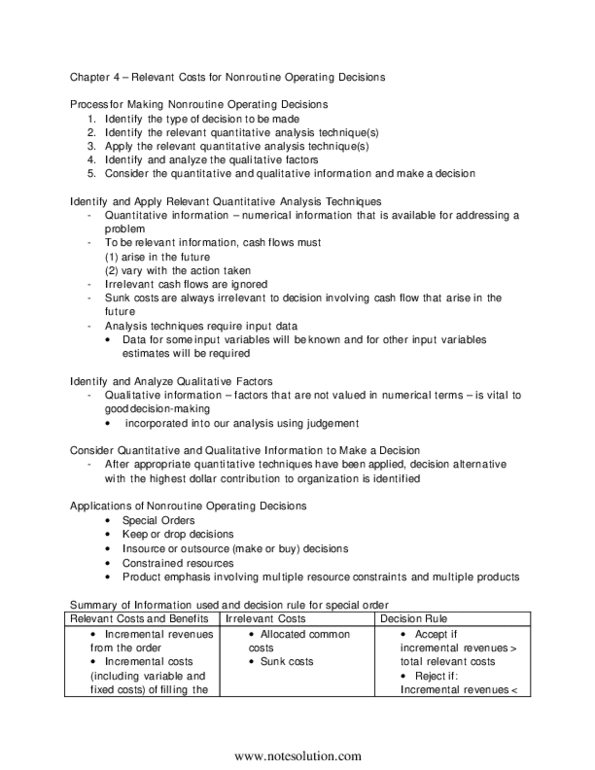

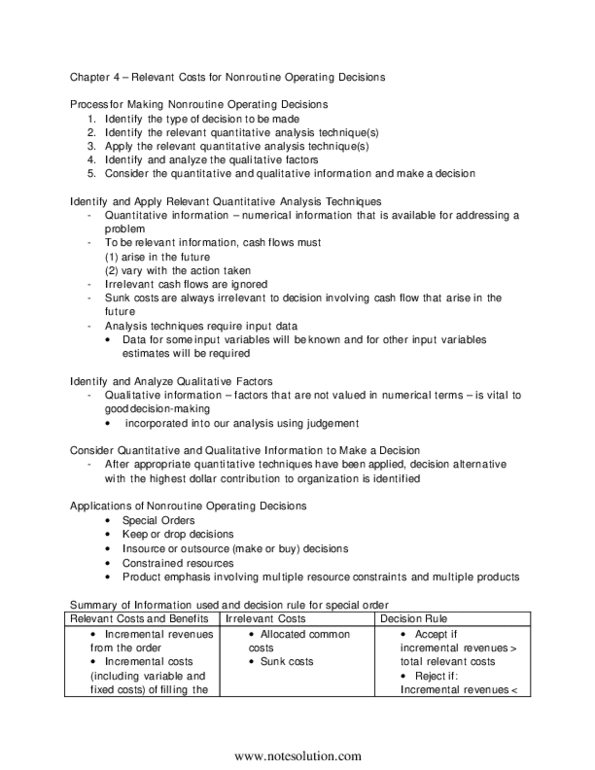

ACCY 307 Chapter Notes - Chapter 4: Insourcing, Decision Rule, Contribution Margin

74

views

4

pages

periwinklemoose863

9 Dec 2018

School

NIU

Department

Accountancy

Course

ACCY 307

Professor

Tamara Phelan

Like

For unlimited access to Textbook Notes, a

Class+

subscription is required.

Get access

Grade+

$40

USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30

USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers

Continue

Related Documents

ACC 410 Lecture : Textbook notes

olivelion816

ACC 410 Chapter 4: Chapter 4

olivelion816

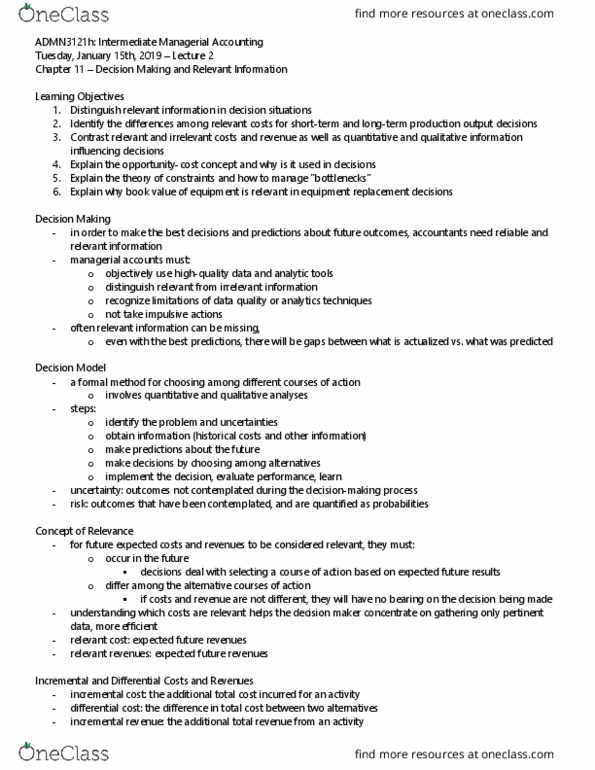

ADMN 3121H Lecture Notes - Lecture 2: Historical Cost, Opportunity Cost, Fixed Cost

blackpig635