Accounting ACCT 2610 Chapter Notes - Chapter 7: Perpetual Inventory, Finished Good, Current Asset

18 Oct 2016

School

Department

Course

Professor

Document Summary

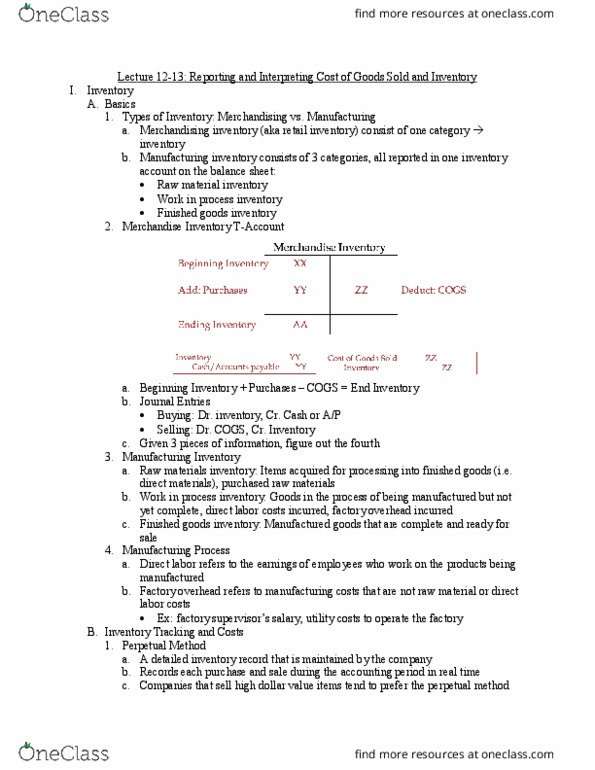

Chapter seven: reporting cost of goods sold and. Nature of inventory and cost of goods sold. Gross profit = net sales - cost of goods sold. The primary goals of inventory management are to have sufficient quantities of inventory available to service customers while minimizing the costs of carrying inventory. Inventory is tangible property held for sale in the normal course of business or used in producing goods or services for sale. Merchandisers (wholesale or retail businesses) hold the following: Merchandise inventory: includes goods held for resale in the ordinary course of business. Goods are usually acquired in a finished condition and are ready for sale without further processing. Raw materials inventory: includes items acquired for the purpose of processing into finished goods. Work in process inventory: includes goods in the process of being manufactured. Finished goods inventory: includes manufactured goods that are complete and ready for sale.