ECON1101 Lecture 9: ECON1101 Week 4 Lecture B

35 views2 pages

ECON1101 Week 4 Lecture B

● Read chapter 6

●

Market Demand

Market Supply

Linked to

Consumers

Firms

Who maximise

Utility

Profits

Constraints by

budget/income

Production function

Slope of curve due to

Decrease of marginal

benefit or marginal utility

Increase marginal cost

Gains from trade

Consumer surplus

Producer surplus

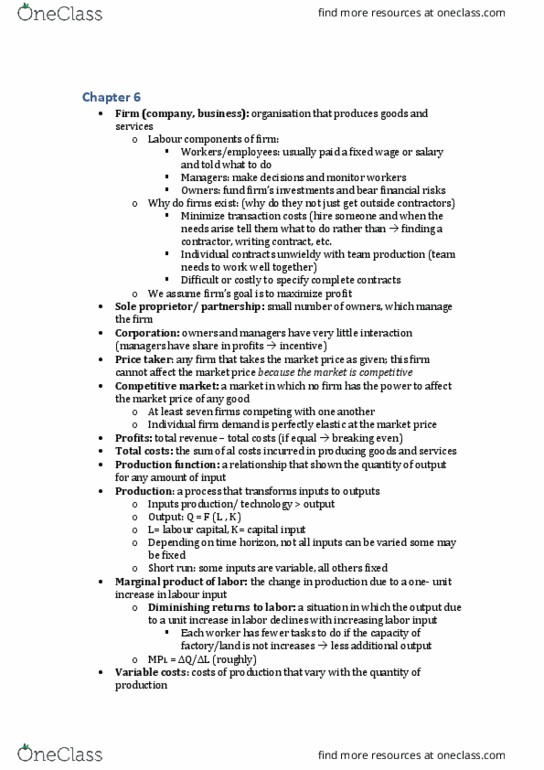

● Firm: an organisation that produced goods or services e.g. farms, bmw

● Labour components of firm:

○ Workers/employees: usually paid a fixed wage or salary and told what to

do

○ Managers: make decisions and monitor workers

○ Owners: Fund firm’s investments and bear financial risks uses financial

capital to purchase physical capital

● Why do firms exist?

○ To minimise transaction costs

○ Individual contracts unwieldy with team production

○ Difficult or costly to specify complete contracts

○ We assume firm’s goal is to maximise profit

● Competitive markets:

○ We’ll assume competitive markets:

■ No firm can influence market price firms are price-takers

■ Profit = revenue - cost

■ Revenue = price x quantity

● Production:

○ Production = a process that transforms inputs into outputs

○ Inputs = production/technology > outputs <- represent with a production

function

○ Output (Q = F(L.K) <- L = labour input K= capital input

○ Depending on tie horizon, not all inputs can be varied some may be fixed

find more resources at oneclass.com

find more resources at oneclass.com

Unlock document

This preview shows half of the first page of the document.

Unlock all 2 pages and 3 million more documents.

Already have an account? Log in

Document Summary

Firm: an organisation that produced goods or services e. g. farms, bmw. Workers/employees: usually paid a fixed wage or salary and told what to do. Owners: fund firm"s investments and bear financial risks uses financial capital to purchase physical capital. Difficult or costly to specify complete contracts. We assume firm"s goal is to maximise profit. No firm can influence market price firms are price-takers. Production = a process that transforms inputs into outputs. Inputs = production/technology > outputs rent = /day. L: labour - variable input -> wage rate = /hr. Marginal product of labour (mp): additional output from additional (or last) unit of labour.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers