MAA363 Lecture Notes - Lecture 7: Takeover, Natural Key, Financial Statement

Document Summary

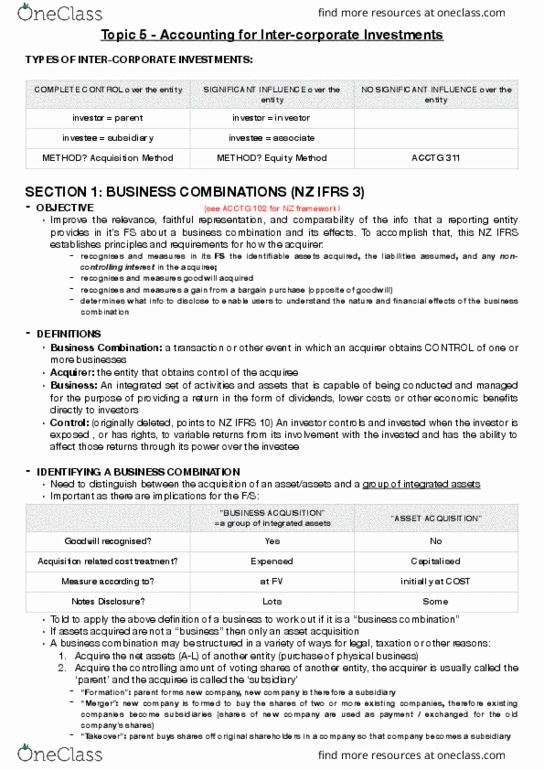

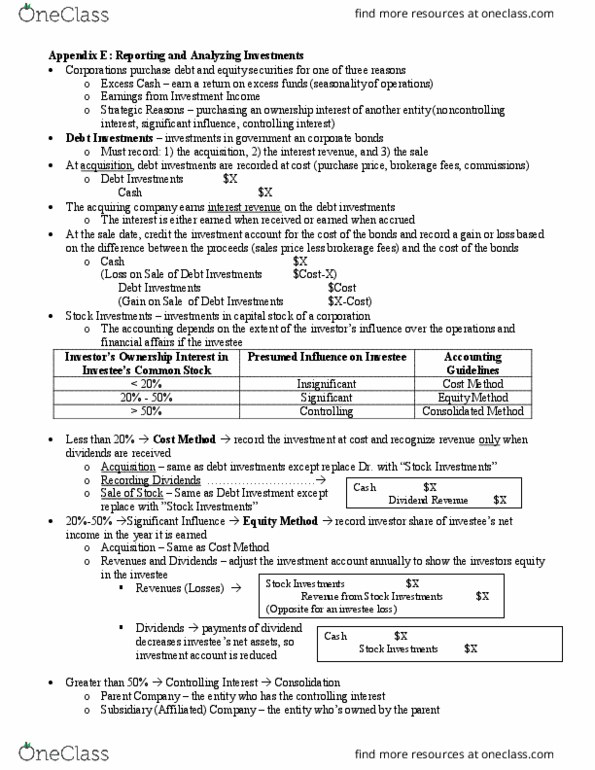

The accounting for investments in ordinary shares is based on the extent of the investors influence over both the operating and financial affairs of the issuing company/investee. E. g. a company that acquires 25% interest in another company in a hostile takeover may not have significant influence over the investee. The investment is recorded at cost, and income is recognised only when cash dividends are received. Costs include all expenditures necessary to acquire these investments e. g. brokerage fees/commissions. Pays per share for 1000 shares plus brokerage fees of . Business combinations: defined as a transaction of other event in which an acquirer obtains control of one or more businesses. Control enables the acquirer to determine the financial and operating policies of the entity and to obtain the benefits of that entity. The acquirer shall account for each business combination through the acquisition method. The acquire does not liquidate but continues its operations with no change in its assets or liabilities.