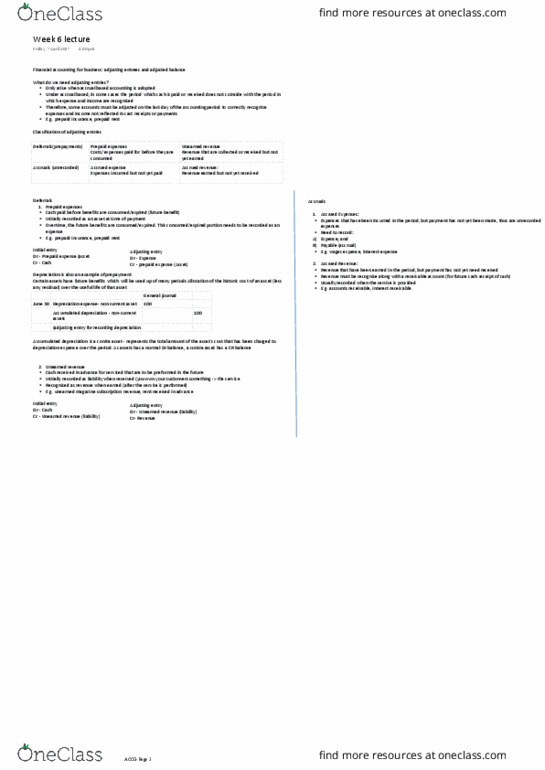

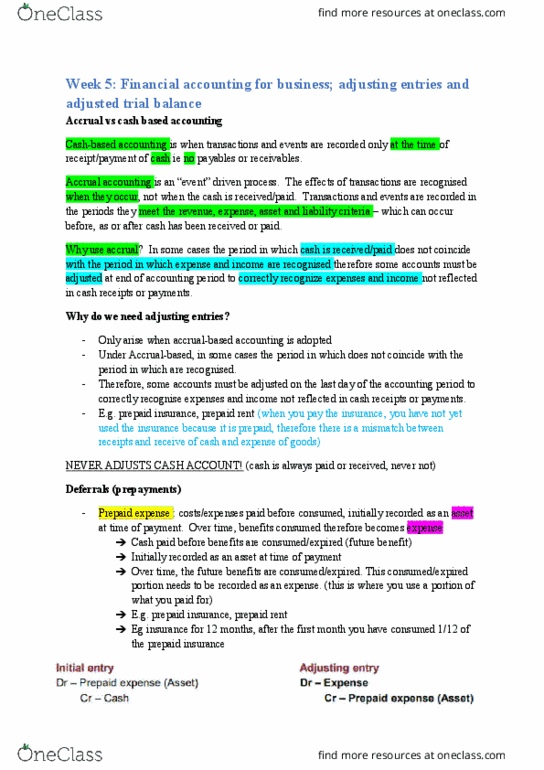

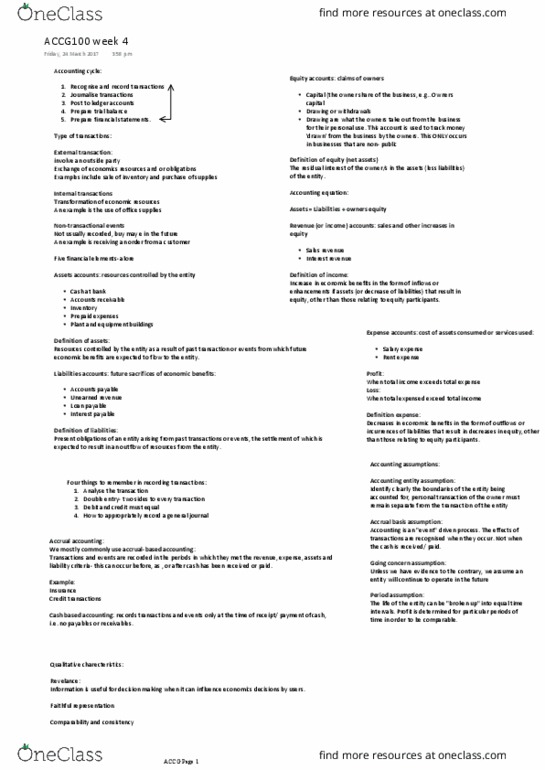

ACCG100 Lecture Notes - Lecture 6: Trial Balance, Retained Earnings, Capital Account

Document Summary

Get access

Related Documents

Related Questions

Chandler, Inc. is owned by Roscoe Chandler and providesappraisal services to individuals and companies wishing to purchaseand sell fine art. Chandler, Inc. began business on January 1,2016, and is just completing its first year of business. Roscoeasks for your help in completing the accounting cycle for thecompany by assisting with the closing process.

Before the closing entries are made, you begin with an adjustedtrial balance. The closing entries are essentially the link fromthe adjusted trial balance to the post-closing trial balance.

Chandler, Inc.

ADJUSTED TRIAL BALANCE

December 31, 2016

| ACCOUNTTITLE | DEBIT | CREDIT | |

|---|---|---|---|

1 | Cash | 76,000.00 | |

2 | Accounts Receivable | 29,000.00 | |

3 | Prepaid Insurance | 16,000.00 | |

4 | Equipment | 60,000.00 | |

5 | Accumulated Depreciation-Equipment | 40,000.00 | |

6 | Accounts Payable | 6,000.00 | |

7 | Salaries Payable | 8,000.00 | |

8 | Income Taxes Payable | 4,000.00 | |

9 | Common Stock | 2,000.00 | |

10 | Retained Earnings | 18,000.00 | |

11 | Dividends | 5,000.00 | |

12 | Income Summary | ||

13 | Fees Earned | 175,600.00 | |

14 | Rent Revenue | 92,000.00 | |

15 | Interest Revenue | 17,200.00 | |

16 | Salaries Expense | 71,000.00 | |

17 | Selling Expense | 25,600.00 | |

18 | Income Taxes Expense | 15,000.00 | |

19 | Depreciation Expense-Equipment | 47,200.00 | |

20 | Insurance Expense | 17,000.00 | |

21 | Miscellaneous Expense | 1,000.00 | |

22 | Totals | 362,800.00 | 362,800.00 |

The final step of the accounting cycle is the closing process.The main goal of this stage of the cycle is to ensure that thebalance of each temporary account is returned to zero and that netincome is transferred to the retained earnings account. The firststep in successfully undertaking the closing process is tounderstand the difference between a temporary account and apermanent account. Roscoe has some questions about the process.

Answer questions (1) - (3) below.

1. If a temporary account has an ending balance of $57,000, whatis its beginning balance for the following accounting period?

2. If a permanent account has an ending balance of $57,000, whatis its beginning balance for the following accounting period?

3. Roscoe will be preparing his yearly financial statementsafter completing Chandler, Inc.âs closing process, and is asomewhat confused about the characteristics of the accounts on hisChart of Accounts. He has started by creating the chart below, andasks for your help in completing it. For each account or type ofaccount listed, choose all descriptions that apply.

| Temporary Account | Permanent Account | Closed to Income SummaryAccount | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Yes | No | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Revenues | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Asset accounts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retained Earnings account | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Expenses | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Liability accounts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dividends account | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Roscoe has attempted to prepare the closing entries forChandler, Inc. on this panel. Heâs not sure if heâs entered thejournal entries correctly, and asks you to review them. You findthat two of the entries are correct, but two are incorrect. Determine which entries are incorrect, and enter all four of theclosing entries for Chandler, Inc. as of Dec. 31 on the Journalpanel. PAGE 25 JOURNAL

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||