ACCT10001 Lecture Notes - Lecture 6: Cash Flow Statement, Cash Flow, Accounts Payable

12 May 2018

School

Department

Course

Professor

Accounting Week 6

7.1 THE PURPOSE AND USEFULENESS OF A STATEMENT OF CASH FLOWS

Statement of cash flows: “tateet that epots o a etit’s ash iflos ad ash

outflows for a specified period

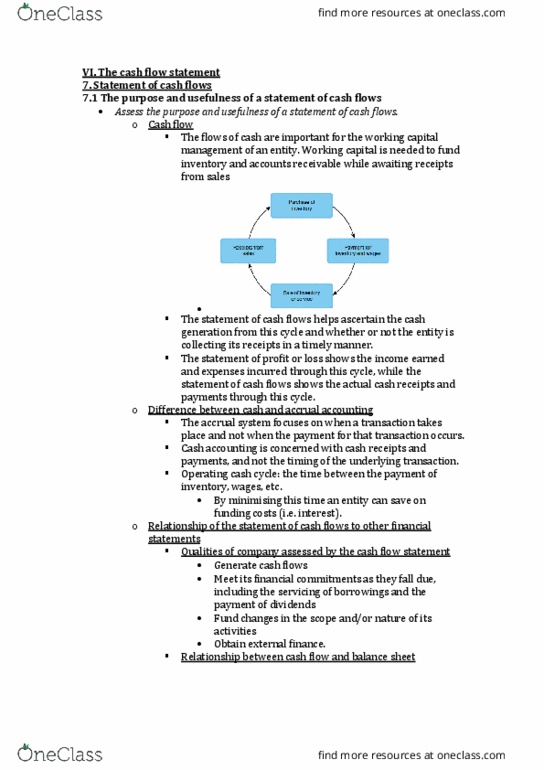

Working capital: Difference between current assets and current liabilities

• Needed to fund inventory and

accounts receivable while

awaiting receipts from sales

• Cash is very important through

cycle as there is normally an

outflow of funds for inventory

and wages prior to inflow from

sales

• CFS helps ascertain cash

generation from this cycle and

whether or not entity is

collecting receipts in timely

manner

Difference between cash and accrual accounting

• Accrual system focuses on when a transaction takes place and not when payment

occurs

• Cash flows is concerned with receipts and payments, not timing

• Timing between payment of inventory, wages, etc and collection of debts is called

the operating cash cycle

• By minimising this time an entity can save on funding costs (ie. interest)

• Positive operating cash cycle means firm collects funds prior to paying accounts

payable

• Entity needs enough cash to meet financial obligations in a timely manner but not

too much as there are costs of storing cash

find more resources at oneclass.com

find more resources at oneclass.com

Relationship of the Statement of Cash Flows to other Financial Statements

Financial Statements:

1. Profit and Loss Statement

2. Balance Sheet

3. Statement of changes in Equity

4. Cash Flow Statement

Cash flows: Cash movements resulting from transactions with parties external to the entity

Purpose of Cash flow Statement is to give additional info provided by other statements and

assist i assessig etit’s ailit to:

• Generate cash flows

• Meet financial commitments as they fall due, including servicing of borrowings and

payment of dividends

• Fund changes in scope and/or nature of activities

• Obtain external finance

Cash inflows: Cash movements into the entity resulting from transactions with an external

party

Cash outflows: Cash movements out of the entity resulting from transactions with an

external party

7.2 FORMAT OF THE STATEMENT OF CASH FLOWS

Cash: Cash and cash equivalents

Cash on hand: Notes and coins, and deposits at call with a financial institution

Cash equivalents: Highly liquid investments and short-term borrowings

Statement of cash flows reports cash on hand at start of reporting period, the cash inflows,

outflows and net cash flow for the reporting period, and the cash balance at the end of the

reporting period.

Classified into: Operating, Investing and Financing Activities

Operating Activities: Relate to the provision of goods and services and other activities that

are neither investing nor financing activities

Investing activities: Those activities that relate to the acquisition and/or disposal of non-

current assets (e.g. property, plant and equipment, and other productive assets and

investments) not falling within the definition of cash

Financing activities: Those activities that change the size and/or composition of the

financial structure of the entity (including equity), and borrowings not falling within the

definition of cash

find more resources at oneclass.com

find more resources at oneclass.com

Reconciliation of Cash from Operating Activities with Operating Profit

• Cash from operating activities can be compared to the P/L as the transactions

affecting the P/L statement reflect the cash flows relating to the operations of the

entity

• Not the same because P/L statement based on accrual accounting and CFS on cash

basis

• Comparing operating activities to profit/loss in P/L statement produces a

reconciliation between two figures showing differences in accrual and cash

transactions

• Reconciliation picks up changes in operating accounts between periods and help

users ascertain the changes in operating accounts brought about by the use of

accrual basis vs cash basis of accounting

• “oeties these aouts efeed to as okig apital

• Examining working capital accounts shows whether profit and flows of cash are

being utilised well in normal operations

Presentation of the Statement of Cash Flows

• net cash flows from operating activities

• net cash flows from investing activities

• net cash flows from financing activities

• total net cash flow (increase or decrease in cash held for the period)

• the beginning cash balance

• the ending cash balance

• comparative figures from the previous year

7.4 ANALYSING THE STATEMENT OF CASH FLOWS

Trend and Ratio Analysis

Trend analysis: Method of examining changes, movements and patterns in data over a

number of time periods

Ratio analysis: An examination of the relationship between two quantitative amounts with

the objective of expressing the relationship in ratio or percentage form

find more resources at oneclass.com

find more resources at oneclass.com