ACCT10001 Lecture Notes - Lecture 8: Income Statement, Cash Flow, Unintended Consequences

29 Aug 2018

School

Department

Course

Professor

Document Summary

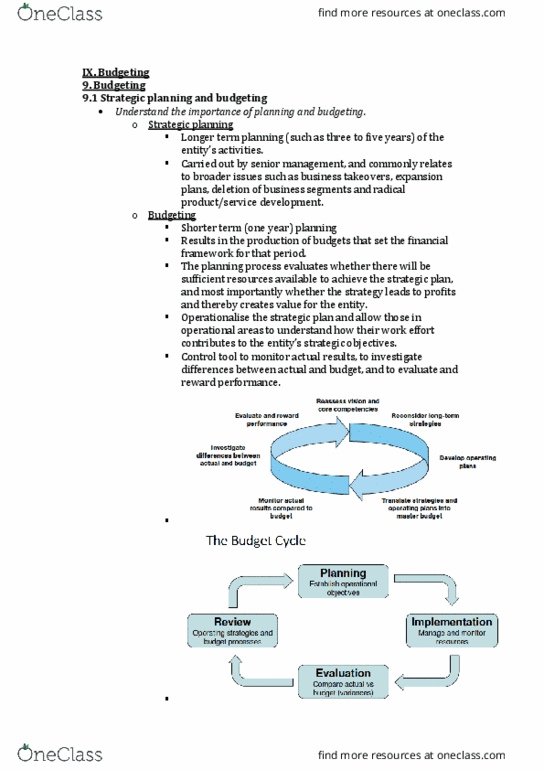

The budget cycle: planning, establish operational objectives, assess past performance and expected operating conditions, prepare budgets. If target is too difficult, no incentive to try. Intended selling price determined by: cost, desired profit margins, competition, pricing policy. The purchases budget: determines the volume of units required to the purchased to meet expected sales, determining the optimum inventory level is important due to the problems associated with too much or too little. Inventory at start + purchases cost of sales = inventory at the end: budgeted cost of sales + desired inventory inventory at start = required purchases. Individual budgets for each cost centre (sales & marketing, administration: all those expenses between gross profit and ebit, variable costs will be determined by budgeted sales volume, fixed costs will be based on known or estimated costs. Capital expenditure budget: planned expenditure relating to on-current assets (ppe) including major refurbishments and acquisitions linked to any expansion plans.