ACCT20001 Lecture Notes - Lecture 6: Cost Accounting, Fidelity Investments, Resource Consumption

16 May 2018

School

Department

Course

Professor

Activity-based costing (ABC)

Over/under costing

•Product-cost cross-subsidisation means that at least one miscosted product is resulting in the

miscosting of other products in the organisation

•A classic example arises when a cost is uniformly spread across multiple users without

recognition of their difference resource demands

-E.g. Each person at a restaurant orders separately and some order expensively and some

order less. At the end, the bill is split - expensive person under-paid and cheaper person over-

paid

•Need to better reflect the resources consumed for pricing, profits and allocation of resources

•Poorly defined costing may inhibit sound decision making

•Improvement:

-Identify more direct costs

-Use more indirect cost pools

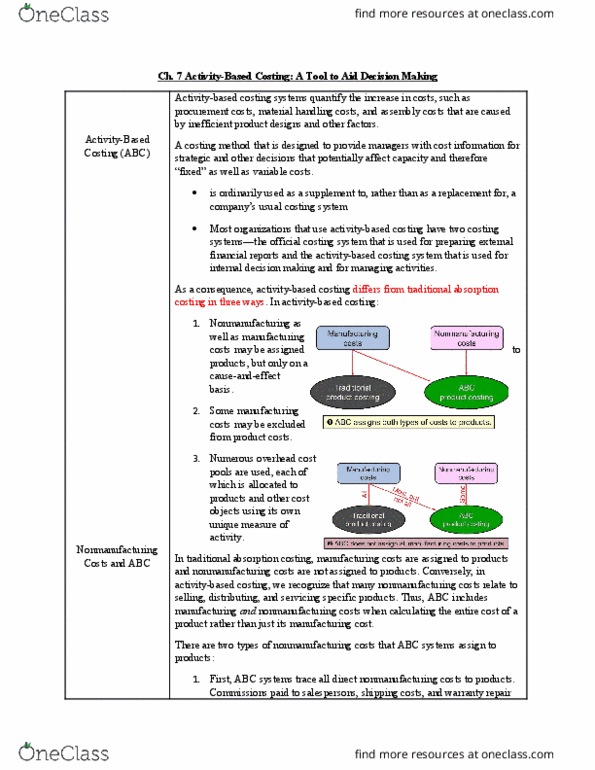

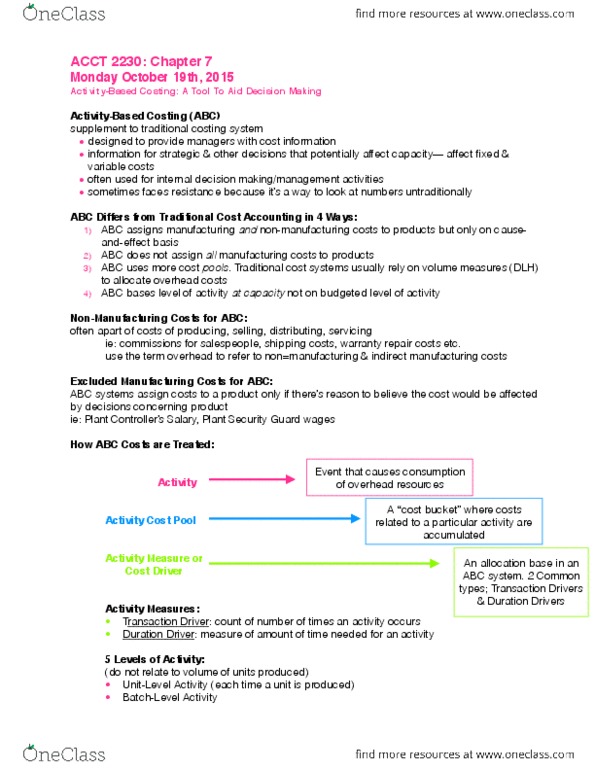

Activity-based costing systems

•An activity is a type of task or function performed in an organisation

•Seeks to identify more costs as direct

•Views costs through an activity lens

•Uses more cost pools than traditional systems for indirect costs

•Assigns overhead costs to specific activities performed in a manufacturing or service delivery

process

•Costs of various activities become the building blocks used to compile total costs for products or

other cost objects

Activity-based costing (ABC) and conventional costing

•Cost accounting systems have adapted over time to suit changes in:

-Operational environments

-Technology

-Cost structures

-Management reporting requirements

-Organisational structure, particularly those focusing on the value chain

•Some have argued that this adaptation has historically, been slow.

1

Conventional cost accounting systems

•Inappropriate pooling of indirect costs and poor choices for cost drivers can lead to the incorrect

costs of products or services

-Possible with any allocation system

•However, it is more likely to produce distorted cost data with the use of:

-Few direct costs categories

-Limited number of cost pools

-Cost driver and allocation bases centred around volume particularly in more complex

operating environments

-E.g. multiple products/services, frequent production in small lot sizes, complex customer

demands/environments

Activity-based costing systems

•Multiple cost pools used to reflect various activities performed

•ABC focuses on fundamental characteristic driving cost pool identification and cost pool selection

•Two steps:

1. Cost of overhead resources assigned to activity cost pools

2. Activity costs allocated to individual products or services

•More activity based cost pools and allocation bases

ABC Costing Framework

2

The cost hierarchy

•Not all costs vary with volume

Example:

•Facility-sustaining: Manufacturing facility $1.5m

•Product-sustaining: Product development cost $1.25m

•Batch-level: Product set up $750,000

•Unit-level: Materials handling $850,000, Production-line labour costs $2.5m, Power $500,000

•Cost driver/allocation base for each of these is different

Applying ABC Model

1. Identify the relevant cost object

2. Identify activities

3. Assign cost to activity-based cost pools

4. For each ABC cost pool, choose a cost driver/allocation basis

5. For each ABC cost pool, calculate a cost driver/allocation rate

6. For each ABC cost pool, allocate activity costs to the cost object

•An allocation basis and cost driver not always the same thing. !

However, often the allocation base will reflect the cost driver.

3