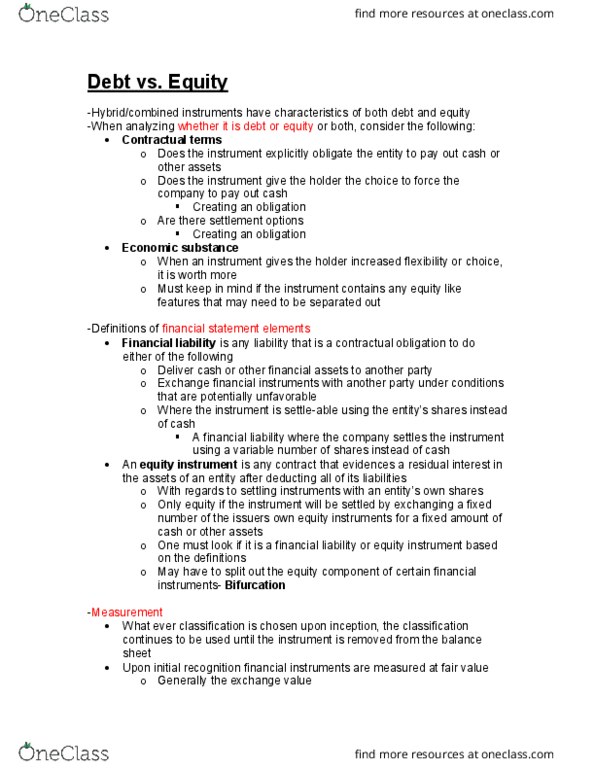

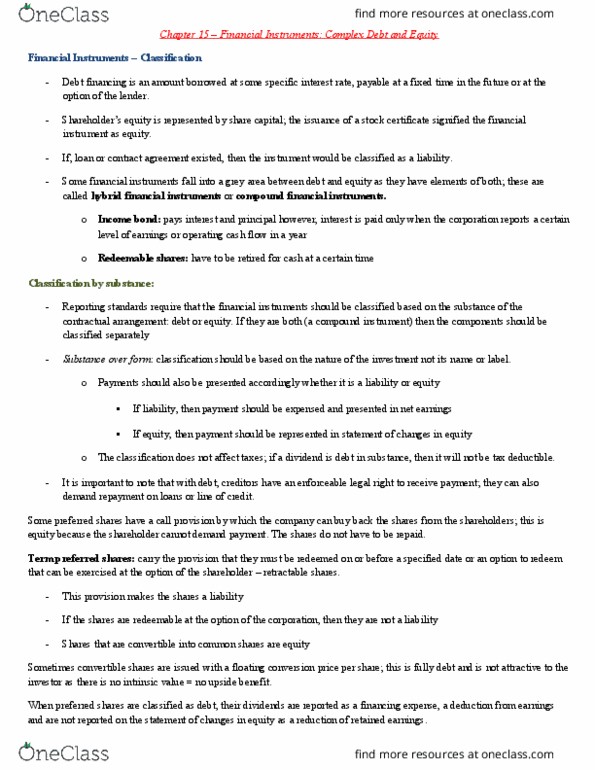

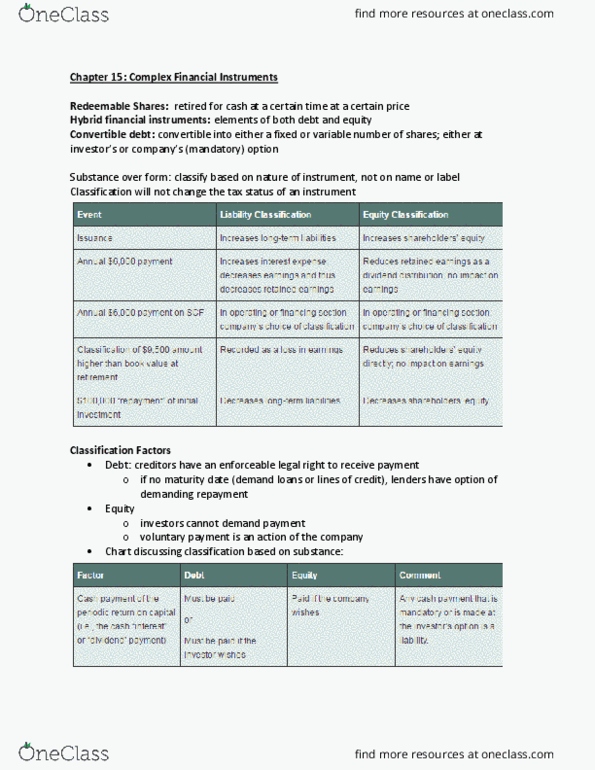

ACCT20002 Lecture Notes - Lecture 7: Effective Interest Rate, Credit Risk, Cash Flow

5 Jun 2018

School

Department

Course

Professor

INCLASS TUTORIAL QUESTIONS & SOLUTIONS: FINANCIAL INSTRUMENTS

Exercise 11.3

Distinguishing financial liabilities from equity instruments

Determine whether Satellite Ltd has a financial liability or equity instrument resulting

from the issue of securities in each situation below. Give reasons for your answer.

1. Satellite Ltd issues 100 000 $1 convertible notes. The notes pay interest at 7% p.a. The

market rate for similar debt without the conversion option is 9%. Each note is not

redeemable, but it converts at the option of the holder into however many shares that

will have a value of exactly $1.

2. Satellite Ltd issues 100 000 $1 redeemable convertible notes. The notes pay interest at

5% p.a. Each note converts at any time at the option of the holder into one ordinary

share. The notes are redeemable at the option of the issuer for cash after 5 years. If

after 5 years the notes have not been redeemed or converted, they cease to carry

interest. Market rates for similar notes without the conversion option are 7% p.a.

3. Satellite Ltd issues redeemable preference shares. The shares carry a cumulative 6%

dividend. The shares are redeemable for cash if the company makes an accounting loss

in any year. Satellite Ltd is highly profitable and has a history of profits and paying

ordinary dividends at a yield of about 4% annually without fail for the past 25 years.

The market interest rate for long-term debt at the time the preference shares were

issued was 7% p.a.

(LO6)

Paragraph 16 of AASB 132:

When an issuer applies the definitions in paragraph 11 to determine whether a financial

instrument is an equity instrument rather than a financial liability, the instrument is an equity

instrument if, and only if, both conditions (a) and (b) below are met.

(a) The instrument includes no contractual obligation:

(i) to deliver cash or another financial asset to another entity or

(ii) to exchange financial assets or financial liabilities with another entity under

conditions that are potentially unfavorable to the issuer.

(b) If the instrument will or may be settled in the issuer’s own equity instruments, it is:

(i) a non-derivative that includes no contractual obligation for the issuer to

deliver a variable number of its own equity instruments or

(ii) a derivative that will be settled only by the issuer exchanging a fixed amount

of cash or another financial asset for a fixed number of its own equity

instruments.

SATELLITE LTD

1. 100 000, $1, 7% convertible notes – non-redeemable, convertible at the option of holder,

convertible into variable number of ordinary shares:

1.

Equity Instrument

Financial Liability

Contractual obligation to deliver variable

number of own equity instruments means

there is no equity risk. A financial

liability in full: refer para 16(b)

2. 100 000, $1, 5% convertible notes – redeemable for cash at the option of the issuer after 5

years, convertible at the option of the holder, convertible for a fixed number of ordinary shares,

interest ceases after 5 years if redemption or conversion not completed:

Equity component for the conversion

option as it relates to a fixed number of

own equity instruments: refer para 16(b).

The equity component is initially

measured as the difference between issue

proceeds and financial liability

component

Option to convert = $100 000 – $20 501

= $79 499

Contractual obligation for annual interest

only. The issuer does not have a

contractual obligation to repay principal

at redemption since redemption is at the

issuer’s option. Financial liability

component is initially measured as the

present value of the interest discounted at

equivalent rate of 7% p.a. for pure play

debt security.

PV = $5 000 x 4.1002 = $20 501

3. 6% preference shares – not redeemable as right to redeem is conditional. Cumulative

dividend distributions; the contractual obligation is limited to the dividends

Equity Instrument

Financial Liability

Classification as equity is appropriate

here; refer AASB 132/IAS 32, paragraph

AG26

The obligation is limited to the dividends.

The intention to make distributions of

dividends does not affect the

classification of the shares.

Exercise 11.7

Accounting for loan assets at amortised cost

Last Ltd is a manufacturing company that makes loans to other parties from time to time.

The loan assets are classified by Last Ltd as subsequently measured at amortised cost.

Last Ltd does not apply the simplified approach to impairment of loans receivable. In

accounting for impairment losses, Last Ltd classifies all loans as remaining at stage 1

from inception to maturity. On 1 July 2019, Last Ltd made the following loans:

A 3-year loan of $1 million to an employee, Mr Whale. The loan is interest free in

recognition of his loyalty to the company. Last Led estimates 12-months expected

credit loss as $30 000. The implicit interest rate is 10%.

Required

Prepare the entries of Last Ltd to account for the three loans from initial recognition on

1 July 2019 to derecognition on 30 June 2022, assuming loans are fully paid on maturity.

(LO14)

Loan to Mr Whale, $1m, 3 years, interest-free.

Initial measurement = fair value = $1 000 000/(1.10)^3 = $751 315

Paragraph B5.1.1 of AASB 9:

• The fair value of a financial instrument at initial recognition is normally the transaction

price (i.e. the fair value of the consideration given or received). However, if part of the

consideration given is for something other than the financial instrument, an entity shall

measure the fair value of the financial instrument. For example, the fair value of a long-

term loan or receivable that carries no interest can be measured as the present value of all

future cash receipts discounted using the prevailing market rate(s) of interest for a similar

instrument (similar as to currency, term, type of interest rate and other factors) with a

similar credit rating. Any additional amount lent is an expense or a reduction of income

unless it qualifies for recognition as some other type of asset.

In this case, the extra amount lent is to reward Mr Whale for his employee loyalty.

Consideration given for loan = $1 000 0000.

Fair value of loan receivable = $751 315.

Employee Expense = $248 685 .

Amortised Cost of Loan Receivable

Period

#

Opening

Balance

Interest

Rate

Interest

Income

Interest

Received

Amortis-

ation

Closing

Balance

Period

End

1

751 315

0.10

75 131

0

75 131

826 446

Jun-20

2

826 446

0.10

82 645

0

82 645

909 091

Jun-21

3

909 091

0.10

90 909

0

90 909

1 000 000

Jun-22

Document Summary

Determine whether satellite ltd has a financial liability or equity instrument resulting from the issue of securities in each situation below. Give reasons for your answer: satellite ltd issues 100 000 convertible notes. The market rate for similar debt without the conversion option is 9%. Each note is not redeemable, but it converts at the option of the holder into however many shares that will have a value of exactly : satellite ltd issues 100 000 redeemable convertible notes. Each note converts at any time at the option of the holder into one ordinary share. The notes are redeemable at the option of the issuer for cash after 5 years. If after 5 years the notes have not been redeemed or converted, they cease to carry interest. Market rates for similar notes without the conversion option are 7% p. a: satellite ltd issues redeemable preference shares.