ACCT10003 Lecture Notes - Lecture 3: Accounts Receivable, Internal Control, Transaction Processing

19 Jun 2018

School

Department

Course

Professor

Accounting Processes and Analysis

LO#1: Describe the changing role of the accounting function in business and explain the factors behind

these changes

“Accounting is the process of identifying, measuring and communicating economic information about an

entity for decision making by a variety of users”

Process/system: Accounting involved consideration of how data is identified and collected to enable prep

or appropriate info.

Economic: focus on business events which have an economic effect on the business either directly or

indirectly

Measurement: evaluate how to best measure economic effect identified via the process/system. (quantify

other than dollars)

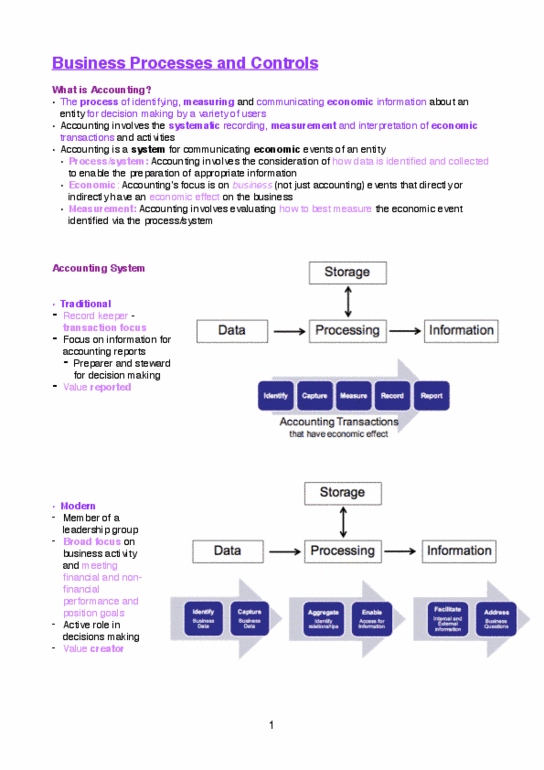

Traditionally:

- Record keeper- transaction focus

- Focus on information for accounting reports

- Preparer and steward for decision making (report to shareholders what’s happening)

- Value reporter

Modern:

- Member of leadership group and have an active role in decision making

- Broad focus on meeting financial and non-financial performance and position goals

There has been a movement from transactional activities to decision support/performance management

activities.

What is expected of the accounting function?

“CEOs and Boards are demanding more from Finance [Accounting]. It is no longer “good enough” to

excel at core Finance [Accounting] activities; Finance needs to advise on strategic and operational matters

as well. To help the business make better decisions faster, Finance [Accounting] must do both extremely

well.”

The accounting function is so far unable to meet these expectations. There is too much a great amount of

time spent on transaction processing as it is mostly manual work. Firms want a greater focus on analysis

and decision support.

LO#2: Describe, identify and explain the characteristics of accounting information

Qualitative characteristics of Financial Information identified in the conceptual framework. For financial

info to be useful it must be relevant and faithfully represents what it is reporting to represent. Usefulness

enhanced if it is comparable, verifiable, timely and understandable.

Relevant:

- Has to be capable- not actually make a difference.

- Have predictive or confirmatory value

- Materiality (how much of a difference in nature and/or amount)

Faithful representation:

- Complete- all information present

- Neutral- free from bias in selection and presentation- make decisions objectively (e.g. accounts

receivable- allowance for doubtful debt, measuring inventory- lower of cost and net realisable

value)

- Free from error- not necessarily accurate (auditors)

The CF also specifies “enhancing qualitative characteristics”:

find more resources at oneclass.com

find more resources at oneclass.com

- Comparability: enables comparisons between entities and for the same entity over a period of time

(e.g. figures from the previous year, use same accounting standards as other companies)

- Verifiability: potential for consensus among knowledgeable and independent observers (e.g. audit

report attached)

- Understandability: reasonable knowledge of business and economic activities to analyse and

interpret the information (note this does not exclude reporting on complex situations).

- Timliness: timely enough to be relevant information.

Information quality- underlying concept, quality information will lead to quality decisions and a higher

quality market. There is a demand for quality information, auditing and accounting systems which enable

the production of quality information.

CFO’s have importance in:

- Drive integration of info across enterprise

- Provide inputs to enterprise strategies

- Support/ manage/ mitigate enterprise risk

- Measure/ monitor business performance

- Driving enterprise cost reduction.

LO#3: Describe the role of the accountant in using, designing and evaluating accounting information

systems

Where does info come from?

Traditional accounting approach

Debit cash as bank goes up, credit inventory goes down.

Economic events > Date acquisition > Source “documents” Operational records: invoices, receipts etc. >

Journals: Chronological record of different types of activities (sales, purchases, cash receipts) > Posting to

ledgers ( record of activities organised by accounts) > reporting in Accounting reports (e.g. financial

statements) > users for interpretation and analysis > decisions and actions > economic events.

Modern accounting approach.

The Query Engine performs all “reporting”, classification and aggregation on the raw economic events data

(that addresses the ontological and measurement questions), providing any “view” of the data requested,

including journals, ledger or “source documents”.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Lo#1: describe the changing role of the accounting function in business and explain the factors behind these changes. Accounting is the process of identifying, measuring and communicating economic information about an entity for decision making by a variety of users . Process/system: accounting involved consideration of how data is identified and collected to enable prep or appropriate info. Economic: focus on business events which have an economic effect on the business either directly or indirectly. Measurement: evaluate how to best measure economic effect identified via the process/system. (quantify other than dollars) Preparer and steward for decision making (report to shareholders what"s happening) Member of leadership group and have an active role in decision making. Broad focus on meeting financial and non-financial performance and position goals. There has been a movement from transactional activities to decision support/performance management activities. Ceos and boards are demanding more from finance [accounting].