ACCT10003 Lecture Notes - Lecture 7: Remittance

19 Jun 2018

School

Department

Course

Professor

Accounting Processes and Analysis

Lecture 7- Conversion Business Process & Payroll Process

Conversion Process

From the business perspective, it includes:

- Manufacturing process – ongoing and special order

- Purchase of raw materials for production

- Organisation and usage of inventory in process

- Finished goods timing and availability

- Allocation resources and therefore costs (‘purchase of resources’ from the organisation)

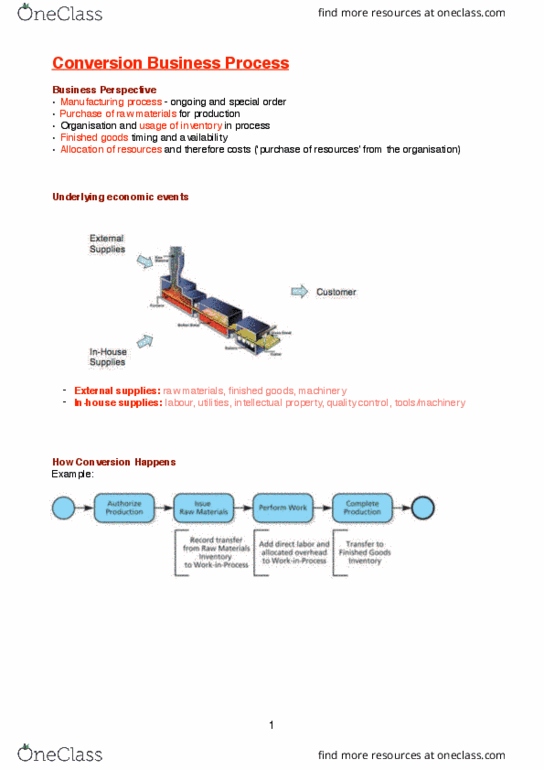

Underlying economic events:

External supplies: Raw materials, finished goods, machinery

In-house supplies: Labour, Utilities, Intellectual Property, Quality Control, Tools / Machinery

Accounting effect:

How Conversion Happens

Modelling a Conversion Process

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Lecture 7- conversion business process & payroll process. Manufacturing process ongoing and special order. Organisation and usage of inventory in process. Allocation resources and therefore costs ( purchase of resources" from the organisation) In-house supplies: labour, utilities, intellectual property, quality control, tools / machinery. Partner with proper authority authorizes production to ensure finished goods are available to meet expected demand. Issues from raw material according to bill of material recorded accurately. Partner issuing material must not be same partner who authorized production. Partner recording issue of material cannot modify bill of material. System must provide authorization order number control, default values, and range and limit checks; must also create audit trail. System must only allow partner to enter the number of items issued based on bill of material, subject to range and limit checks on quantities; date defaults to current date. Inspection ensures that only products meeting quality standards are allowed. Finished product inventory must be updated promptly and accurately.