FNCE10002 Lecture Notes - Lecture 5: Retained Earnings, Net Present Value, Weighted Arithmetic Mean

19 Jun 2018

School

Department

Course

Professor

Principles of Finance

Lecture 5: Capital Budgeting II

Issues in cash flow estimations

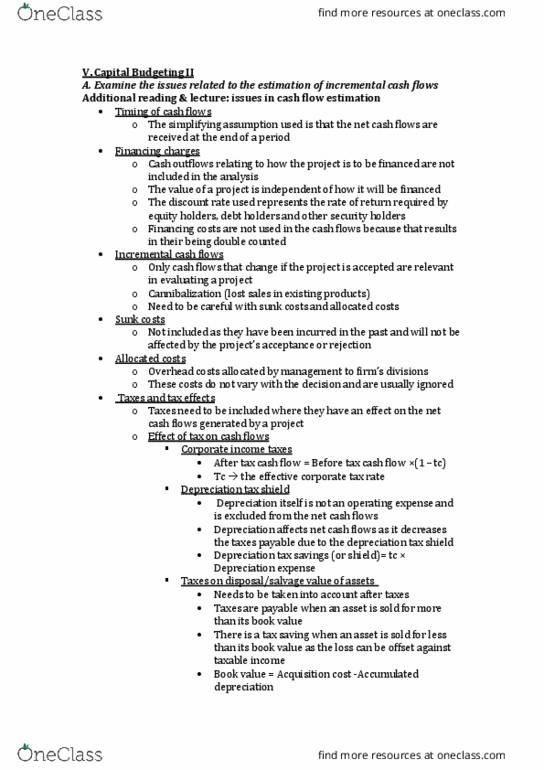

1. Timing of cash flows

The exact timing of project cash flows can affect the valuation of a project. The simplifying assumption that

we use is that the net cash flows are received at the end of a period.

2. Financing charges

Cash outflows that are relation to how a project is to be financed is not included in the analysis.

The valuation of the project is dependent on how it will be financed.

The discount rate used to represent the , and the rate of return required by debtholders and other security

holders.

Financing costs are not used in the cash flows because it results in their being double counted.

3. Incremental cash flows

Only cash flows that change if the project is accepted are relevant in evaluating a project

Cannibalization (lost sales in existing products)

Sunk costs

These costs are not included as they have been incurred in the past and will not be affected by the

project’s acceptance or rejection

Allocated costs

Overhead costs allocated by management to firm’s divisions

These costs do not vary with the decision and are usually ignored

Examples are administrative costs incurred by head office and allocated to divisions

4. Taxes and tax effects

Tax needs to be included where they influence the net cash generated by the project. Taxes have three

main effects on net cash flows

i. Corporate income tax

ii. Depreciation tax shield

iii. Taxes on disposal of assets

5. Corporate income tax

Corporate taxes should be included as a cash outflow.

6. Depreciation tax savings or depreciation tax shield

Depreciation itself is not an expense and is excluded form net cash flows. However, depreciation does

affect net cash flows because it reduces the taxes payable due to the depreciation tax shield.

7. Disposal or salvage value of assets

Disposal or salvage of assets needs to be considered after taxes.

i. Taxes are payable when the asset is disposed for more than its book value

ii. A tax saving occurs when an asset is sold for less than its book value as the cost can be offset

against taxable income.

find more resources at oneclass.com

find more resources at oneclass.com

Where R= revenue, OC = operating cost and D= depreciation …

The incremental net after tax cash flows are:

Separating the after-tax residual or salvage value we get

Inflation and Capital Budgeting

It is important to be consistent with the treatment of inflation. For nominal cash flows, use a nominal

discount rate. For real cash flows, use a real discount rate. The Fisher relationship gives:

The Weighted Average Cost of Capital

WACC () is the benchmark required rate of return used by a firm to evaluate its investment opportunities.

The discount rate used to evaluate projects of similar risk to the firm. It will consider how a firm finances its

investments (debt vs equity). The WACC depends on:

i. The market value of alternative sources of funds

ii. The market costs associated with the sources of these funds

iii. Qualitative factors (adjustments for inflation, taxes)

Estimating the WACC

Four main steps involved in estimating WACC:

1. Identify financing components

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Issues in cash flow estimations: timing of cash flows. The exact timing of project cash flows can affect the valuation of a project. The simplifying assumption that we use is that the net cash flows are received at the end of a period: financing charges. Cash outflows that are relation to how a project is to be financed is not included in the analysis. The valuation of the project is dependent on how it will be financed. The discount rate used to represent the , and the rate of return required by debtholders and other security holders. Financing costs are not used in the cash flows because it results in their being double counted. Only cash flows that change if the project is accepted are relevant in evaluating a project. These costs are not included as they have been incurred in the past and will not be affected by the project"s acceptance or rejection.