BTC3150 Lecture Notes - Lecture 5: Liquigas, Glenboig, Embezzlement

!

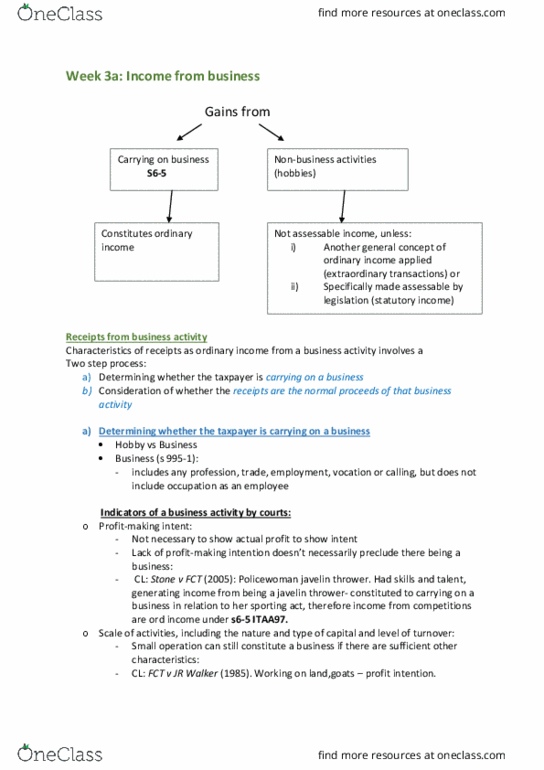

Week$4:$Extraordinary$&$Isolated$Transactions$&$Income$from$Property$

Extraordinary!and!isolated!transactions!

o A!receipt!from!the!normal!proceeds!of!a!business!constitutes!ordinary!income!(s!6-5).!

o Alternatively,!transactions!may!be!categorised!as:!

–Extraordinary+transactions:!where!the!receipt!arises!outside!the!normal!proceeds!of!the!

business.!

–Isolated+transactions:!where!the!receipt!is!one-off!in!nature!and!not!undertaken!by!an!

existing!business!operation.!

o While!extraordinary!and!isolated!transactions!may!appear!to!take!a!capital!characterisation,!

it!may!be!ordinary!income!if!it!falls!into!any!of!the!following!categories:!

i) Forms!a!business!itself!

ii) First!strand!of!FCT!v!Myer!Emporium!

iii) Second!strand!of!FCT!v!Myer!Emporium!

!

i)Forms+a+business+itself+

o Under!the!!"#$%&'($")!&**+'),-(.$/"0+)1)2"''$3)(1904)!principle,!a!gain!derived!from!an!

isolated!transaction!is!distinguished!between:!

a)A!mere$realisation!of!a!capital!good,!resulting!in!a!capital!gain:!Scottish+Australian+Mining+

Co+Ltd+v+FCT!and!

b)!A!gain$made$from$carrying$on$a$business,!resulting!in!ordinary!income!(s6-5)!

o Profit!from!an!isolated!(and!potentially!an!extraordinary)!transaction!that!has!exhibited!

34%%$/$+(0)$(.$/"0&'3)&%)")543$(+33!is!considered!&'.$("'-)$(/&6+)%'&6)543$(+33)"/0$1$0-:!7!8)1)

9:$0%&'.3);+"/:)<0-)=0.!(1982):!

Carrying!on!a!business!(ordinary!income)!

• FCT+v+Whitfords+Beach+Pty+Ltd+

(1982):!extensive!land!development!

amounting!to!a!land!development!

business.!

• Stevenson+v+FCT+(1991):$extensive!

land!development!"(.!sales!process!

undertaken!by!taxpayer.!

“Mere!realisation”!(capital!gain)!

• Statham+v+FCT+(1988):$existing!farm!

business!ceased!with!subsequent!

land!development!by!the!council!(not!

the!taxpayer).!Taxpayer!not!directly!

involved!in!sales!process.!

• Casimaty+v+FCT+(1997):)undertook!

minimum!land!development!required!

to!obtain!subdivision!approval.!

!

o Only!the!net!profit!is!assessable!as!ordinary!income!under!the!principle!in!7!8)1)9:$0%&'.3)

;+"/:)<0-)=0.)(1982).!

o Net!profit!=!Sales!proceeds!–!(Land!value!at!time!isolated!tras!commenced!+Development!

costs)!

!

!

!

!

!

!

!

!

!

!

!

!

!

ii)+First+strand+of+FCT+V+Myer+Emporium+

o Proceeds!from!an!extraordinary!or!isolated!transaction!will!be!ordinary!income!if!the!first!&'!

second!strand!of!Myer!applies.!

!

o An!extraordinary!or!isolated!transaction!will!satisfy!the!first!strand!of!Myer!when!the!

following!requirements!are!all!met:!

1. There!was!a!business!operation!or!commercial!transaction!

2. There!was!a!profit-making!intention!upon!entering!the!transaction!

3. The!profit!was!made!by!the!means!consistent!with!the!original!intention!

o Profit$resulted$from$“business$operation$or$commercial$transaction”!

If!resulting!from!an:!

–“Extraordinary!transaction”:!this!requirement!is!satisfied.!

–“Isolated!transaction”:!likely!to!be!satisfied!when!transaction!is!entrepreneurial!in!nature,!

rather!than!a!type!of!transaction!that!a!salary!earner!would!enter!into:!see!Ruling!TR!92/3.!

o Profit-making$intention$upon$entering$the$transaction!

o “Entering!the!transaction”:!in!relation!to!selling!assets,!“entering!the!transaction”!is!the!time!

of!asset!purchase.!

o Profit-making!intention!need!not!be!the!taxpayer’s!sole!or!dominant!intention:!7!8)1)!&&#$(>)

(1990).!

o Profit$made$by$means$consistent$with$original$intention!

o The!way!profit!is!eventually!made!must!be!consistent!with!the!original!profit-making!

intention.!

– Taxpayer!in!the!business!of!designing,!constructing!and!operating!shopping!centres!

undertaking!an!extraordinary!transaction:!9+30%$+#.)=0.)1)7!8)(1991):!

!

iii)Second+strand+of+FCT+v+Myer+Emporium+

o Proceeds!from!a!transaction!will!be!ordinary!income!if!the!taxpayer!sells!the!right!to!income!

from!an!asset,!without!selling!the!underlying!asset:!

–Sale!of!“right!to!interest”!(ie!income),!while!retaining!the!loan!principal!(ie!the!underlying!

asset):!?-+')@6*&'$46A!

–Sale!of!right!to!royalties,!while!retaining!underlying!property!(being!trademarks):!2+('-)

B&(+3)CDE=F)=0.)1)7!8)(1991).!

!

!

!

!

!

Statutory$provisions$

o Statutory!provisions!may!apply!to!a!receipt!arising!from!an!extraordinary!/!isolated!

transaction.!!

!!!!!!! !

o Common!statutory!provisions!that!apply!to!business!activities:!

a) Capital!gains!tax!

– Extraordinary!and!isolated!transactions!that!are!not!characterised!as!ordinary!income!in!

respect!of!a!post!19!September!1985!asset!will!often!be!subject!to!CGT.(See,!Chapter!11)!

b) Bounties!and!subsidies!

– Payments!from!the!government!to!assist!the!recipient!in!carrying!on!its!business!

constitute!statutory!income:!s!15-10.!

– Does!not!apply!to!gains!that!are!ordinary!income:!s!15-10(b).!

c) Profit-making!undertaking!or!plan:!s!15-15.!

>!Profits!from!a!profit-making!undertaking!or!plan!constitute!statutory!income!under!s!

15-15.!!Exclusions:!

–Gains!that!are!ordinary!income:!s!15-15(2)(a);!or!

–Gains!that!involve!assets!purchased!on!or!after!20!September!1985:!s!15-15(2)(b).!

•Potentially!limited!application!as!gains!would!often!be!assessed!as!ordinary!income!due!

to!7!8)1)9:$0%&'.3);+"/:)<0-)=0.A)

)

Income$from$property$

o ‘tree’!and!‘fruit’!analogy:!income!(being!the!fruit)!flows!from!capital!(being!the!tree).!

!

!

Main!areas!of!property!income!

1.Interest$

o Interest!is!the!return!that!flows!from!the!lending!of!money!and!is!the!compensation!for!the!

loss!of!use!of!that!money.!

–Capital!sum!lent!is!not!affected!by!the!payment!of!interest.!

–CL:!G$/:+3)1)9+306$(30+');"(H)=0.)(1947).!

o Constitutes!ordinary!income:!s!6-5.!

o I$3/&4(03)"(.)*'+6$463J =+(.+'3)6"-)$(/'+"3+)")30"(."'.)$(0+'+30)'"0+)"(.K&')&%%+')")#&"()

.$3/&4(0)&')*'+6$46)0&)"//&4(0)%&')'$3H)&%)(&(L'+*"-6+(0J)

=&"()I$3/&4(0J9:+'+)"6&4(0)*'&1$.+.)0&)0:+)5&''&M+')$3)#+33)0:"()0:+)#&"()"6&4(0)

=&"()*'+6$46J);&''&M+'):"3)0&)'+*"-)6&'+)0:"()0:+)"6&4(0)C&%)/"*$0"#F)".1"(/+.)5-)0:+)

#+(.+')

)

)

Document Summary

Week 4: extraordinary & isolated transactions & income from property. Extraordinary and isolated transactions: a receipt from the normal proceeds of a business constitutes ordinary income (s 6-5), alternatively, transactions may be categorised as: Extraordinary transactions: where the receipt arises outside the normal proceeds of the business. Taxpayer not directly involved in sales process: casimaty v fct (1997): undertook minimum land development required to obtain subdivision approval, only the net profit is assessable as ordinary income under the principle in fct v whitfords. Sale of right to interest (ie income), while retaining the loan principal (ie the underlying asset): myer emporium. Sale of right to royalties, while retaining underlying property (being trademarks): henry. Statutory provisions: statutory provisions may apply to a receipt arising from an extraordinary / isolated transaction, common statutory provisions that apply to business activities, capital gains tax.