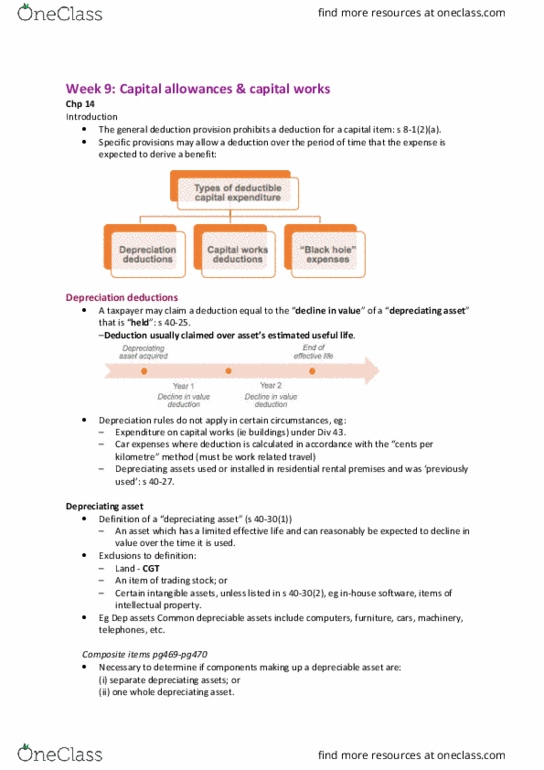

BTC3150 Lecture 6: Week 7

!

Week$7:$General$Deductions$

• The!main!provision!that!provides!taxpayers!a!deduction!for!an!expense!is!the!general!

deduction!provision:!

$$$$$$$$$$$$$$$Deductions$=$General$Deductions$(s8-1)$+$Specific$Deductions$(s8-5)$

• Section!8-1!has!the!potential!to!apply!to!any!taxpayer.!

• A!loss!or!outgoing!(ie!an!expense)!may:!

– Be!deductible!under!s!8-1!and!a!specific!provision.!In!these!cases,!use!the!“most!

appropriate”!provision:!s!8-10.!

– Not!qualify!for!a!deduction!under!a!specific!provision.!!In!these!cases,!consider!

deductibility!under!s!8-1.!

!

General!Deduction!rule:!

i.Positive$Limbs!(pass!1/2)!

ii.$Negative$limbs!(if!knocked!out!by!any-no!longer!deductable)!

!

1)Positive$limbs$

A!taxpayer!can!deduct!from!his!or!her!assessable!income!a!loss$or$outgoing!to!the!extent!that!it!is!(s!

8-1(1)):!

a)$Incurred$in$gaining$or$producing$assessable$income;$or$

b)$Necessarily$incurred$in$carrying$on$a$business$for$the$purpose$of$gaining$or$producing$assessable$

income$

!

Loss$or$outgoing:$

o Section!8-1!applies!to!both!a!loss!and!outgoings:!

– Loss:!depletion!of!a!taxpayer’s!financial!position:!Charles$Moore$&$Co$(WA)$Pty$Ltd$v$FCT!

(1956)!–!robbed!on!the!way!to!the!coy’s!bank.!Money!is!deductible!as!the!money!would!

have!been!income!if!he!successfully!banked!it!in.!

– Outgoing:!eg,!an!expense.!

o Determining!whether!there!is!a!loss!or!outgoing!is!not!generally!an!issue!in!claiming!a!

deduction!under!s!8-1.!

!

Nexus$test$–$positive$limb$s8-1$

a)Incurred$in$gaining$or$producing$assessable$income;$

o Requires!nexus!between:!

! !

b)$Necessarily$incurred$in$carrying$on$a$business$for$the$purpose$of$gaining$or$producing$assessable$

income$

!!!!!! !

!

!

!

!

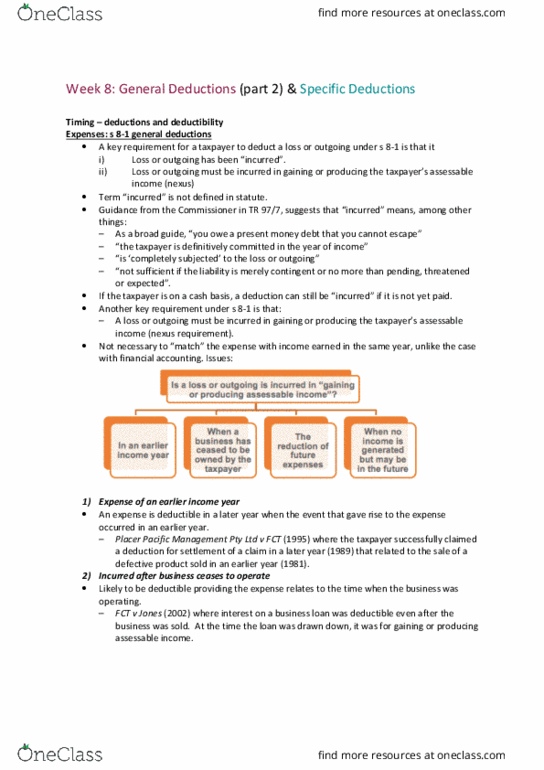

“Gaining$or$producing$assessable$income”!to!be!interpreted!as:!!

o “in$the$course$of!gaining!or!producing!assessable!income”:!Amalgamated!Zinc!(De!Bavay’s!

Ltd)!v!FCT!(1935).!

!!!!!!!!!!! !

Judicial$tests!

The!courts!have!adopted!a!number!of!approaches!to!determine!whether!a!loss!or!outgoing!is!

incurred!in!the!course!of!gaining!or!producing!assessable!income:!

a) Incidental$and$relevant$test!

!!!!!!!!!!!!!!!A!loss!or!outgoing!is!sufficiently!connected!to!the!production!of!assessable!income!where:!

Ø “the!expenditure!…!is!incidental!and!relevant!to!the!operations!or!activities!regularly!

carried!on!for!the!production!of!income”:!!

Ø W$Nevill$&$Co$Ltd$v$FCT$!(1937)-!compensation!made!to!fire!underperforming!

director=deducatable!beacause!after!firing!director,!coy!turned!around!and!generated!

income.!

b) Essential$character$test!

!!!!!!!!!!!!!!Courts!have!looked!at!the!“essential!character”!of!an!expense:!

Ø Home!to!work!travel!expenses:!essential!character!was!to!put!the!taxpayer!in!a!position!

to!gain!or!produce!assessable!income,!not!the!production!of!assessable!income!

CL:!Lunney$v$FCT;$Hayley$v$FCT!(1958).!

Ø No!deductible!if!choose!to!stay!far!away!from!work!

c) Occasion$of$the$expenditure$test!

Courts!have!considered!whether!the!occasion!of!the!expenditure!arises!out!of!income-

producing!activities:!!

Ø FCT$v$Payne!(2001)!and!FCT$v$Day!(2008)!–!deductible!for!legal!expenses.!Defending!Day!

for!misconduct!at!work-protecting!Day’s!name.!Lose!job/income.(protection!of!

job/income=!deductible)!

Ø Requires!an!assessment!as!to!what!is!productive!of!the!taxpayer’s!assessable!income.!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

$Nexus$sufficiently$direct$or$too$remote?$

• If!the!nexus!between!the!expense!and!the!production!of!assessable!income!is!too!remote,!it!

is!not!deductible!

• Eg!Go!overseas!to!find!inspiration!for!work!but!looks!more!like!when!for!holiday-!nexus!too!

remote,hence!non-deductable!

• Some!cases!exist!where!it!is!questionable!as!to!whether!a!nexus!can!be!established,!for!

example:!

a) Expenses$involving$alleged$or$actual$wrongdoing$

$$$$$$$$$$$$$!!!!!Nexus!satisfied!for!expenses!arising!from!alleged!or!actual!wrongdoing!incurred!by:!

§ Employees!defending!improper!conduct!charges!which!are!“quasi-personal”:!FCT!v!

Day!(2008).!

§ Business!taxpayers!in!respect!of!defending!claims!(eg,!for!libel!actions)!arising!out!of!

the!ordinary!course!of!business:!!

CL:Herald$and$Weekly$Times$v$FCT!(1932)!–!wrong!news!about!someone-Herald!

legal!expenses!in!court!are!deductibleàrelated!to!work!

$CL:FCT$v$Snowden$v$Willson$Pty$Ltd$(1958)àdefend!reputation!to!generate!future!

income.!

§ Company!directors!incurring!costs!to!defend!criminal!charges:!Magna!Alloys!&!

Research!Pty!Ltd!v!FCT!(1980).!

§ Expenses!related!to!illegal!business:!FCT$v$La$Rosa$(2003)!

b) Expenses$to$reduce$future$expenses$

§ Nexus!established!between!an!expense!that!improves!the!taxpayer’s!business!

overall!and!reduces!future!expenses!

§ Termination!payment!to!end!a!contract!of!employment!for!poor!performing!staff:!

W!Nevill!and!Co!Ltd!v!FCT!(1937).!

c) Involuntary$losses$or$outgoings$

§ Nexus!established!between!an!involuntary!loss!where!it!arises!out!of!the!taxpayer’s!

income-producing!activities!

§ Day’s!earnings!stolen!while!on!way!to!the!bank:!Charles!Moore!&!Co!(WA)!Pty!Ltd!v!

FCT!(1956).!

$

$$$Sufficient$temporal$nexus$

• An!issue!as!to!whether!a!nexus!can!be!established!where!expenses!are!incurred:!

!

a)Expenses$related$to$the$production$of$assessable$income$in$future$years$

§ An!expense!incurred!to!gain!or!produce!assessable!income!in!the!future!may!satisfy!the!

nexus!requirement!

– Interest!associated!with!the!purchase!of!an!asset!which!was!expected!to!produce!

income!in!the!future!was!deductible:!!

Document Summary

Week 7: general deductions: the main provision that provides taxpayers a deduction for an expense is the general deduction provision: Deductions = general deductions (s8-1) + specific deductions (s8-5) Section 8-1 has the potential to apply to any taxpayer: a loss or outgoing (ie an expense) may: Be deductible under s 8-1 and a specific provision. In these cases, use the most appropriate provision: s 8-10. Not qualify for a deduction under a specific provision. In these cases, consider deductibility under s 8-1. General deduction rule: i. positive limbs (pass 1/2: negative limbs (if knocked out by any-no longer deductable) A taxpayer can deduct from his or her assessable income a loss or outgoing to the extent that it is (s. 8-1(1)): incurred in gaining or producing assessable income; or, necessarily incurred in carrying on a business for the purpose of gaining or producing assessable income. Loss or outgoing: section 8-1 applies to both a loss and outgoings: