BSB110 Lecture Notes - Lecture 2: Current Liability, Accounts Payable, Comprehensive Income

Accounting – Regulation, Conceptual Framework, Accounting Equation, Financial Statements

Accounting

- The process of identifying, measuring, recording, and communicating economic

transactions/events of a business operation

- Transactions – economic activities relevant to a particular business e.g. sale of an item,

purchase from a supplier

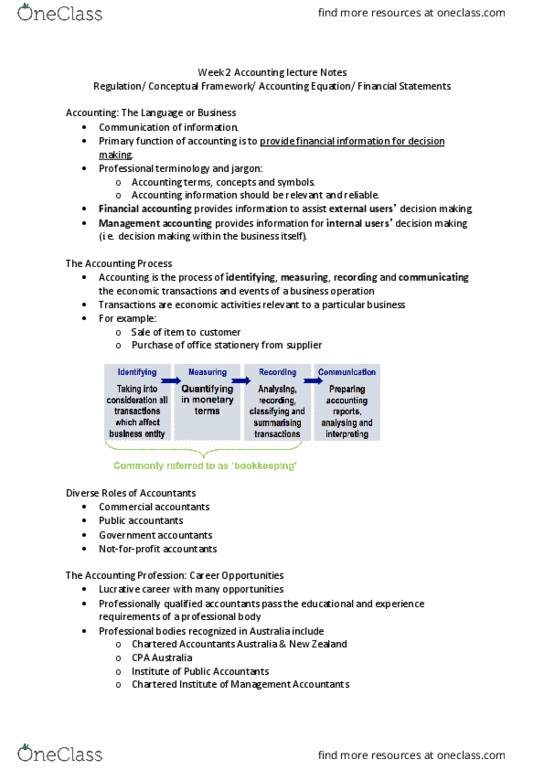

- Accounting process

oIdentifying – Measuring – Recording – Communication

oFirst three are also known as ‘bookkeeping’

oIdentifying – taking into consideration all transactions which affect business entity

oMeasuring – Quantifying in monetary terms

oRecording – analyzing, recording, classifying and summarizing transactions

oCommunication – preparing accounting reports, analyzing, and interpreting

- Roles

oCommercial accountants

oPublic accountants

oGovernment accountants

oNot-for-profit accountants

Business Organisations

- Sole Proprietorship (sole trader)

oOwned by one person e.g. restaurant, dentist, panel beaters

- Partnership

oOwned by more than one individual e.g. accountants, solicitors, doctors

- Company (Public and Private)

oOrganised as a separate legal entity and owned by shareholders e.g. BHP, CSR,

Westpac, RM Williams

oLimited liability

- Trust

oA relationship/association between 2 or more parties whereby one party holds

property in trust for the other (corporate trust is popular among small businesses)

- Co-operative

oMember-owned, controlled and used

oConsist of 5 or more people e.g. Australian Forest Growers, Ballina Fishermen’s Co-

operative Ltd.

- Not-for-Profit

oAssociations

Formed by small, non-profit, community-based groups

oGovernment (Public Sector)

Organisations owned by the government (federal, state, or local)

Conceptual Framework

- Consists of a set of concepts to be followed

- Four sections

oObjective of general purpose financial reports

Provide financial information about the reporting entity to resource

providers

Emphasises that primary users are existing and potential shareholders,

lenders, and other creditors

Provide information about financial position, financial performance and cash

flows to assist users to evaluate and predict:

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Accounting regulation, conceptual framework, accounting equation, financial statements. The process of identifying, measuring, recording, and communicating economic transactions/events of a business operation. Transactions economic activities relevant to a particular business e. g. sale of an item, purchase from a supplier. Roles: commercial accountants, public accountants, government accountants, not-for-profit accountants. Sole proprietorship (sole trader: owned by one person e. g. restaurant, dentist, panel beaters. Partnership: owned by more than one individual e. g. accountants, solicitors, doctors. Company (public and private: organised as a separate legal entity and owned by shareholders e. g. bhp, csr, Trust: a relationship/association between 2 or more parties whereby one party holds property in trust for the other (corporate trust is popular among small businesses) Co-operative: member-owned, controlled and used, consist of 5 or more people e. g. australian forest growers, ballina fishermen"s co- operative ltd. Formed by small, non-profit, community-based groups: government (public sector) Organisations owned by the government (federal, state, or local)