BSB110 Lecture Notes - Lecture 8: Critical Thinking, Internal Control, Bank Reconciliation

Accounting – Cash

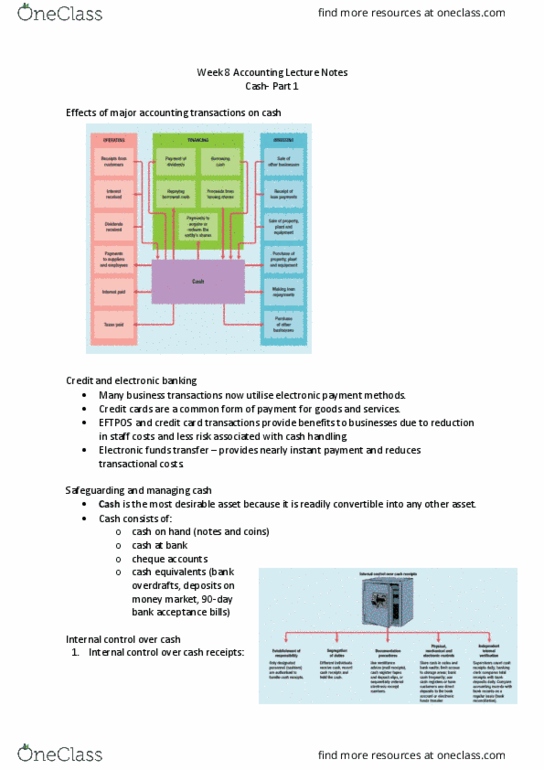

Safeguarding and Managing Cash

- Cash is the most desirable asset – readily convertible into any other asset

- Cash on hand

- Cash at bank

- Cheque accounts

- Cash equivalents (bank overdraft, deposits on money market)

Bank accounts to safeguard cash

- Minimises amount of cash kept on hand

- Provides a double record of all bank transactions

Bank reconciliation

- ‘bring to agreement’

- Things are recorded in business’s books and the bank’s records

- Reconciliation explains why they don’t agree (why there’s a difference)

- Most differences are due to timing differences

- Allows people to uncover errors, fraudulent activities etc.

- Mostly done one a month

- Internal control process – segregation of duties is essential (bank rec should be done by

someone who doesn’t have a recording responsibility)

- Reasons for differences

oDeposits in transit – some items have been recorded by the business but not by the

bank (e.g. depositing cash after the bank’s recording period for the day is over) – can

cause bank statement balance to be different from the business’s

oWriting cheques – on the day it is written, the business records it, but the bank

doesn’t record it until the cheque is presented

oBank charges – automatically deducted from the bank account, but not the

business’s records

- Items needed

oPrepared every month

oLook at what was outstanding the previous month

oCompare opening and closing balance

oLook at cash receipts, payments, and the bank statement

- Process

oCompare bank statement to previous month’s bank rec and current month’s CRJ and

CPJ

oIdentify unticked items on bank statement

oIdentify unticked items in CPJ and CRJ

oIdentify unticked items from opening/previous bank reconciliation

oTotal cash journals and post to the cash at bank account in ledger

oComplete bank rec

oIMPORTANT: Adjusted bank balance should equal cash at bank account balance

The Bank Statement

- From the bank’s perspective

- If balance is Cr – business is in Dr (is owed money)

- If balance is Dr – business is in Cr (owes money)

Managing and Monitoring Cash

- Principles

oIncrease speed of collection of receivables

Have as small a collection period as possible

Cannot be too small otherwise there is a risk of losing customers

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Cash is the most desirable asset readily convertible into any other asset. Cash equivalents (bank overdraft, deposits on money market) Minimises amount of cash kept on hand. Provides a double record of all bank transactions. Things are recorded in business"s books and the bank"s records. Reconciliation explains why they don"t agree (why there"s a difference) Most differences are due to timing differences. Allows people to uncover errors, fraudulent activities etc. Internal control process segregation of duties is essential (bank rec should be done by someone who doesn"t have a recording responsibility) Items needed: prepared every month, look at what was outstanding the previous month, compare opening and closing balance, look at cash receipts, payments, and the bank statement. Process: compare bank statement to previous month"s bank rec and current month"s crj and. If balance is cr business is in dr (is owed money) If balance is dr business is in cr (owes money) Principles: increase speed of collection of receivables.