ACC10007 Lecture Notes - Lecture 9: Cost Driver, Indirect Costs, Resource Consumption

Management Accounting - Costing

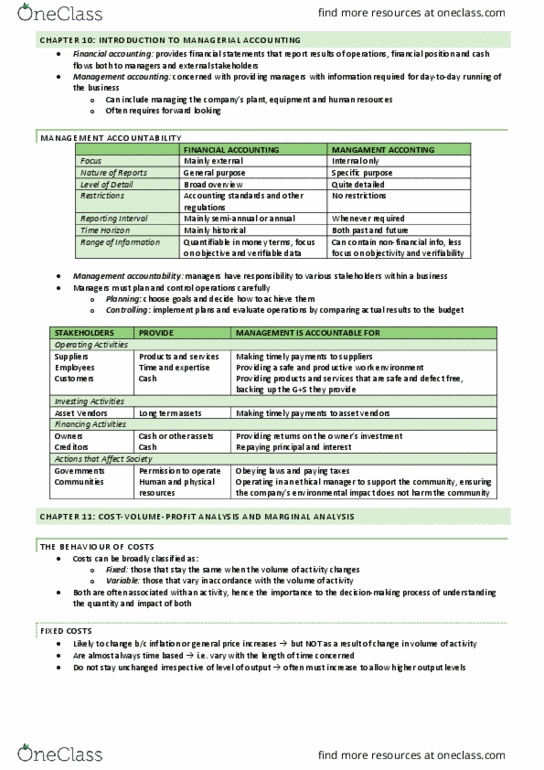

Financial Accounting

Management Accounting

Focus

Mainly external

Internal only

Nature of reports

General purpose

Specific purpose

Level of detail

Broad overview

Quite detailed

Restrictions

Accounting standards and other

regulations

No restrictions

Reporting interval

Mainly semi-annual or annual

Whenever required

Time horizon

Mainly historical

Both past and future

Range of information

Quantifiable in money terms;

focus on objective and

verifiable data

Can contain non-financial

information; less focus on

objectivity and verifiability

Use of cost information:

What is a cost?

An outlay or expenditure:

●Usually measured in monetary terms

●Made to achieve a particular objective

What is a cost object?

A cost object is basically anything for which a separate measurement of cost is required

Could include: products, services, customers, business units or geographical regions

Costs must be assigned to the specific cost object that caused the cost to be incurred.

Importance of costing:

●Allows costs to be managed.

●Leads to more informed decision making.

Use of cost information:

●The system used by entities to collect and report the cost of resources used by a particular cost objects is known as

the costing system.

●Costing systems track product costs for financial reporting purposes as well as all other costs incurred by the

business.

Costing is NOT just relevant for manufacturing:

While manufacturing has been the traditional industries using costing due to the need to cost inventories, costing is very

important in service settings.

Examples:

●Telecommunications: costs and profitability of mobile, fixed line, internet; different customer segments.

●Banking: costs of servicing customers through different channels; costs and profitability by product/ customer

type.

●Government: cost of providing services through different channels; impact of policy initiatives.

●Education: cost of delivery through online versus classroom based. Profitability of various courses.

Costs are NOT only relevant for Accountants:

Chief Executives:

●Where do we make our money and why?

●How can we improve profitability?

Marketing Managers:

●How should we price products?

●Which products/ services should we spend marketing effort and money on?

Operations Managers:

●What are our high cost processes and why?

●How can we reduce costs?

Why would be want to know the cost of a product?

●Value inventories on hand

●Determine cost of goods sold (cost of sales)

●Assist management of resources

●Assist pricing decisions

●Determine product line profitability

●Assist other decisions / planning - Should we drop a product line? Should we accept a special order?

The nature of Full Costing:

Full Costing is a method of determining the unit cost of output.

Full cost includes the total amount of resources, usually measured in monetary terms, sacrificed to achieve a particular

objective

●It considers both the direct and indirect costs of achieving that objective

A cost object can be any item for which management wants a separate measure of cost -- in a clothing factory, cost

objects could include: manufacturing cost of a pair of jeans, cost of running the maintenance department, total cost of

running the factory

Deriving Full Costs in a Single-product/Single-service Operation:

Assume a business has only one product line or service, and each unit is identical. Product cost per unit could be

calculated as

●The total cost of production (eg direct material, direct labour, factory rent, maintenance, electricity, depreciation

of equipment) divided by the number of units produced

This is used when the units of output are identical, or very similar, and may be referred to as process costing.

Single Product Operations example:

Just Beer is a craft beer manufacturer that makes one product, a pale ale. Last year it produced 60,000 bottles. The costs

incurred were as follows:

Labour $28,500

Materials 30,000

Other Expenses 6,900

Total $65,400

The full cost of producing one bottle of the pale ale is found by taking the total cost and dividing by the number of units

produced

$65,400 / 60,000 bottles = $1.09 per bottle

Issue with using only financial reporting inventory costs for decision making:

●Manufacturing can be a relatively small component of total costs.

●The company can be losing money when the costing system indicates that all products are profitable.

●Selling, delivery and service costs can differ substantially across products and customers.

Internal value chain:

It is important to understand all the costs of doing business, not just production costs.

The Internal Value Chain represents all the linked activities undertaken by an entity.

For a Manufacturer:

For a Service Provider:

Document Summary

Quantifiable in money terms; focus on objective and verifiable data. Can contain non-financial information; less focus on objectivity and verifiability. A cost object is basically anything for which a separate measurement of cost is required. Costs must be assigned to the specific cost object that caused the cost to be incurred. Could include: products, services, customers, business units or geographical regions. The system used by entities to collect and report the cost of resources used by a particular cost objects is known as. Costing systems track product costs for financial reporting purposes as well as all other costs incurred by the the costing system. business. While manufacturing has been the traditional industries using costing due to the need to cost inventories, costing is very important in service settings. Telecommunications: costs and profitability of mobile, fixed line, internet; different customer segments. Banking: costs of servicing customers through different channels; costs and profitability by product/ customer.