ACCT1501 Lecture Notes - Lecture 10: Income Statement, Balance Sheet, Accounts Receivable

18 May 2018

School

Department

Course

Professor

Saturday, 13 May 2017

Accounting & Financial Management 1A

Financial Statement Analysis

-Using financial statements to evaluate an entity’s financial performance & position

-Comparisons - previous years, competitors, other factors

-Used for creditors & shareholders (providers of capital), managers (performance

evaluation), regulators (compliance with standards), customers, suppliers

-‘Common size’ financial statements

•Balance sheet items as % of total assets

•Income statement items as % of sales revenue

•Removes effect of company size

-Ratio Analysis:

•Ratio - proportion of one account over another (relationship between selected data)

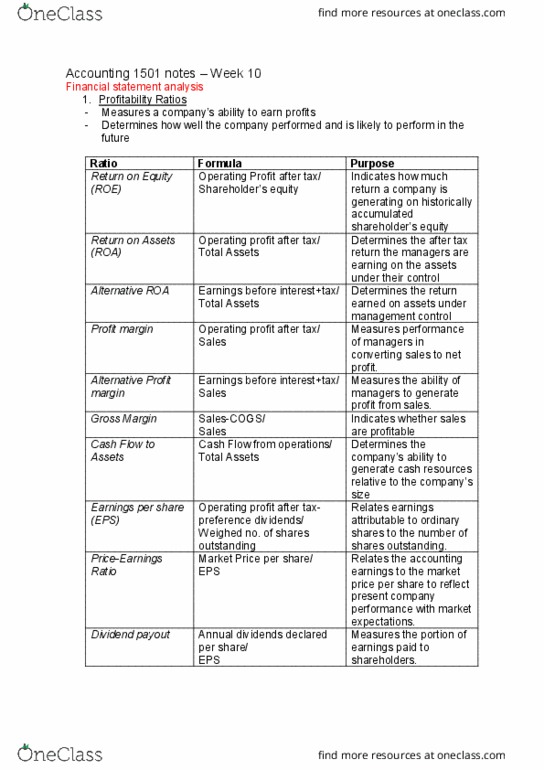

•Profitability Ratios: Company’s ability to earn profits

-Should exceed zero (a positive return)

-Higher ratios are more preferable

(i) Return on Assets (ROA)

•Ability to earn on company’s assets

•ROA = Operating Profit After Tax ÷ Total Assets

(ii) Return on Equity (ROE)

•Rate of return on amount of shareholders’ equity

•ROE = Operating Profit After Tax ÷ Shareholders’ Equity

(iii) Profit Margin (PM)

•Percentage of sales revenue that ends up as profit

•PM = Operating Profit After Tax ÷ Sales Revenue

•Gives some indication of pricing strategy or competition intensity in industry

•Gross Margin = Gross Profit (Sales revenue - COGS) ÷ Sales Revenue

-Further indication of company’s product pricing & product mix

!1

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Using nancial statements to evaluate an entity"s nancial performance & position. Comparisons - previous years, competitors, other factors. Used for creditors & shareholders (providers of capital), managers (performance evaluation), regulators (compliance with standards), customers, suppliers. Common size" nancial statements: balance sheet items as % of total assets, income statement items as % of sales revenue, removes effect of company size. Ratio analysis: ratio - proportion of one account over another (relationship between selected data, pro tability ratios: company"s ability to earn pro ts. Further indication of company"s product pricing & product mix. Measures pro tability in buying (or manufacturing) & selling goods before. Average number of days to collect accounts receivable: relationship between ratios: du pont system of ratio analysis. Roa = pro t margin x asset turnover. Roe = roa x leverage (total assets shareholders" equity: liquidity ratios: ability to pay its short term debts when due (i) current ratio, cr = current assets current liabilities.