FINS1613 Lecture Notes - Lecture 5: Inventory Turnover, Asset Turnover, Financial Statement

Chapter 2: Financial Statement Analysis

Financial Statements: accurate and reliable financial information is critical to financial

market health

- accounting boards- ules hih ops prep financial statements- Australian

aoutig stadads oad, Itl at stadads oad, fiaial at stadads

board (IFRS)

- auditors- neutral third party- rules, reliable

- financial health/postion

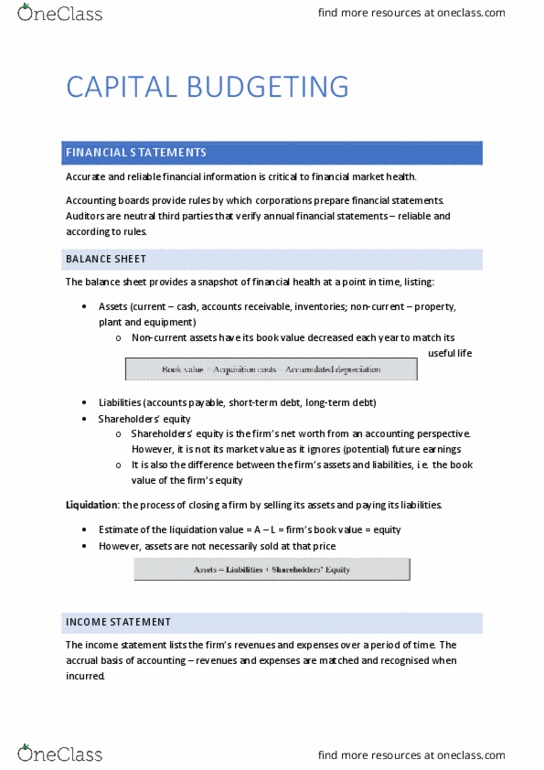

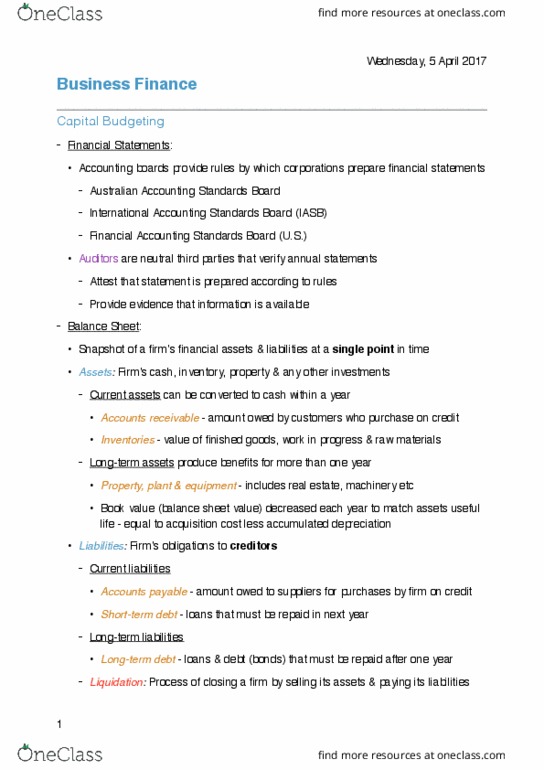

o /s: A=L+E ook alue/et oth of fis euity + estimate of the

liquidation value of the firm- total value of equity P*shares)assets- cash +

other marketable securities (ST low risk)

▪ liquidation value: value of firm after assets are sold and liabilities paid

▪ market/price-to-book ratio: ratio of firs aket ap to the BV of

shaeholdes euit: aket alue of euit/BV of euit > alue

stocks- low M/B ratio vs. growth stocks)

▪ leverage: debt-euit atio: fis leeage etet to hih it elies

on debt as a source of financing) = total debt/total equity (+equity

multiplier)

▪ etepise alue: total aket alue of fis euit ad det, less

value of its cash and marketable securities- value of underlying

business (EV= market value of equity + debt – cash)

▪ liquidity: quick ratio= (current assets – inventory)/current liabilities

o statem of changes in equity

- past performance

o Y statem (P&L) (revenues/expenses- et pofit otto lie aual

accounting- rev/exp matched and recognised when incurred, depreciated

matching LT life, taxes based on EBIT. Debt payments are ignored when

evaluating projects- tax benefits of debt addressed through appropriate

discount-rate)

▪ Gross profit, operating expenses, EBIT, net profit before tax

▪ Profitability ratios: gross margin (ability to sell for more than direct

costs), operating margin (EBIT for each dollar of sales- efficiency), net

profit margin (fraction of each dollar in revenue that is available to

equity holders after firm pays its expenses, plus interest and taxes-

quod differences in efficiency+leverage)

▪ EPS = NP/shares outstanding

▪ Asset efficiency ratios: asset turnover = sales/total assets vs. fixed

asset turnover= sales/fixed assets

▪ Working capital ratio: accounts receivable days= accounts

receivable/avg daily sales (accounts payable days accts payable/avg

daily COGS + inventory days= inventory/avg daily COGS), inventory

turnover ratio= sales/inventory

▪ Interest coverage ratio: atio of fis pofit/CF to iteest epese

(financial strength)

▪ EBITDA: reflects cash a firm has earned from operations

▪ Leverage ratios: interest coverage ratio/times interest earned (TIE)

ratio- assessets of fis leeage ailit to oe iteest

find more resources at oneclass.com

find more resources at oneclass.com

measure of earnings/interest: high means earning more than

necessary to meet repaym

▪ Investment returns: return on equity (ROE/ROA)= net profit/BV of

equit+RO assets

▪ DuPont Identity: drivers of ROE- product of profit margin, asset

turnover and a measure of leverage:

• ROE= (net prof/total equity)*(sales/sales) = (net

prof/sales)*(sales/total equity)= (net prof/sales)*(sales/total

assets)*(total assets/total equity)

• ROE = net profit per dollar of sales (profit margin)* sales per

dollar of sales (asset turnover)* assets per dollar of equity

(measure of leverage equity multiplier)

▪ Valuation ratios: market value of firm P/E ratio (value of equity to

firm earnings): market cap/net profit = share price/EPS – considers

equity sic leverage → PEG atio atio of fis P/E to epeted

earnings growth rate >1 overvalued)

▪ Depreciation: systematic allocation of acquisition cost of long-lived or

fixed assets to expense accounts of particular periods that benefit

from the use of assets (initial acquisition cost of asset, useful life of

the asset, depreciation method)

• Prime cost depreciation (straight-line depreciation): initial

book value=acquisition cost; annual depreciation (initial

BV/depreciation life)- assets ost diided euall oe its life

o CF statem (lists how cash has been allocated over PoT-

operating/investing/financing activities- cash basis- recognised when paid not

matched to when they are incurred))

▪ Tax paym based on Y statem EBIT, debt paym ignored, tax benefits of

debt are addressed through appropriate discount rate

▪ After-tax salvage: cash received for selling an asset adjusted for taxes

over or under paid because the selling $P differs from the book value

(using prime cost depreciation)

• After tax salvage = salvage $P – tax rate*capital gains

▪ Operating activities- direct (gross cash receipts/paym) vs. indirect

(profit adjusted for cash nature)

• Net profit + noncash expenses

• Working capital- deduct increases in acc rec- rep additional

lending by firm to customers and reduces cash available to

firm + add increases in acc payable (rep increase in cash

available) + deduct inventory increases

▪ Investment activities

• Purchases of new PPE- capital expenditures → do not appear

immediately as expenses on Y statem, firm depreciates these

assets and deducts depreciation expenses o/t

• Add back depreciation and subtract actual cap exp and

subtract acquisitions

▪ Financing activities

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Financial statements: accurate and reliable financial information is critical to financial market health. Accounting boards- (cid:396)ules (cid:271)(cid:455) (cid:449)hi(cid:272)h (cid:272)o(cid:396)p(cid:859)s prep financial statements- australian a(cid:272)(cid:272)ou(cid:374)ti(cid:374)g sta(cid:374)da(cid:396)ds (cid:271)oa(cid:396)d, i(cid:374)t(cid:859)l a(cid:272)(cid:272)t sta(cid:374)da(cid:396)ds (cid:271)oa(cid:396)d, fi(cid:374)a(cid:374)(cid:272)ial a(cid:272)(cid:272)t sta(cid:374)da(cid:396)ds board (ifrs) Past performance: y statem (p&l) (revenues/expenses- (cid:374)et p(cid:396)ofit (cid:858)(cid:271)otto(cid:373) li(cid:374)e(cid:859) a(cid:272)(cid:272)(cid:396)ual accounting- rev/exp matched and recognised when incurred, depreciated matching lt life, taxes based on ebit. Mgmt. discussion and analysis (md&a- off b/s transactions), statement of changes in equity, notes. Financial statements- b/s: financial health, a= l+e income statement- net profit measure of a firm profitability over the period cash flow statement: cash generated, and how allocated over a period of time. Income statement: revenue cogs = gross profit: gross profit depreciation = ebit, ebit taxes= net profit. Cape(cid:454): does(cid:374)(cid:859)t appea(cid:396) as pa(cid:396)t of i(cid:374)(cid:272)(cid:396)e(cid:373)e(cid:374)tal ea(cid:396)(cid:374)i(cid:374)gs, (cid:271)ut is a (cid:272)ash i(cid:374)(cid:448)est(cid:373)e(cid:374)t (cid:894)-) Depreciation: appears in incremental earnings, but is a cash recovery of equipment.