FINS1613 Lecture Notes - Lecture 3: Dividend Discount Model, Risk Premium, Preferred Stock

Chapter 7: Share Valuation: The Dividend-Discount Model

- Valuation principle: price of a security should equal PV of expected cash flows an

investor will receive from owning it

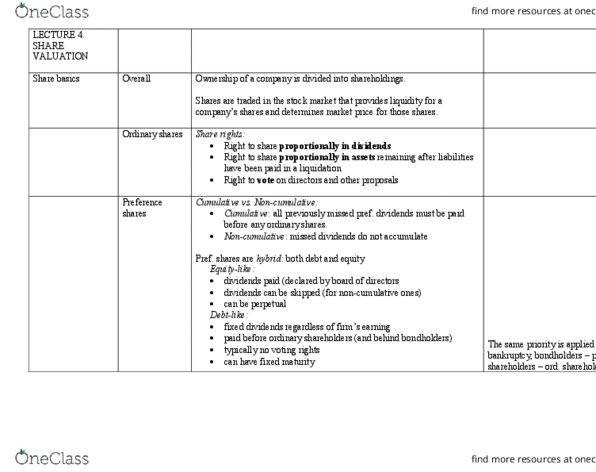

- EQUITY: Ordinary share: share of ownership in co, which confers rights to any

ordinary dividends as well as rights to vote on elections of directors, mergers and

other maj events

- Preference share: shares w preference over ordinary shares in paym of dividends

and in liquidation (cumulative pref shares: any unpaid dividends are carried forward,

ouulatie: issed diideds do’t auulate

o Like a pepetual od: poised CF + oseuees if ot paid ut a’t

force bankruptcy- pref dividend obligations)

- Payout: bond, pref share, ordinary share

Equity cost of Capital

- Security sold by corporations to raise money from investors today in exchange for

expected fut paym- receive dividend paym (not guaranteed- ordinary and preference

shares)

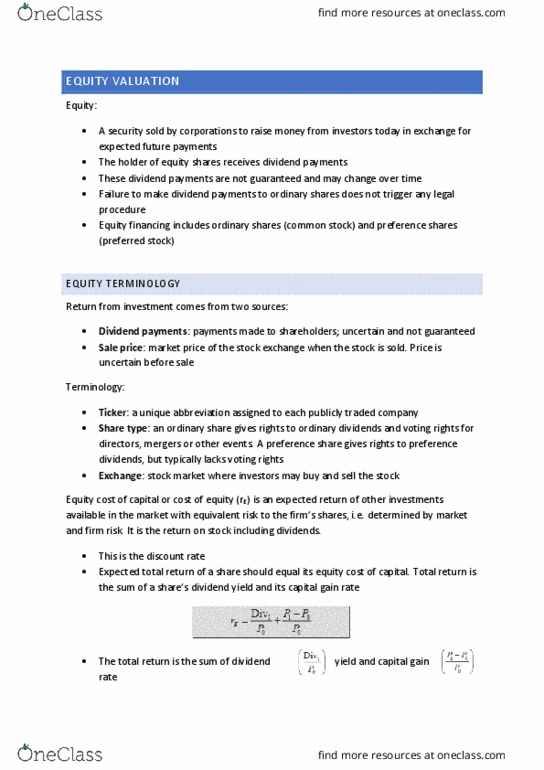

- Dividend and capital gains (r(E) is equity cost of capital)

- Expected total return of the share should equal the expected return of other

investments available in the market with equivalent systematic risk

Risk premium-

- Systematic risk: risk that must be taken if buying stock (eco cycle)- requires risk

premium

- Idiosyncratic risk: endemic to particular stock (not whole investm portfolio) – not

rewarded for this risk quod can get rid of it

- Risk premium relates to equity risk (systematic risk) + expected return is derived

from cash expected return ie expected return – cash return = risk premium

Valuing equity- dividend discount model

- P = dividends + final share price ÷ (1+r)

-

- model that values shares of a firm according to the PV of the future dividends

find more resources at oneclass.com

find more resources at oneclass.com

- price of a share = PV of all expected fut dividends it will pay

- Terminal price: final price of a stock used in dividend discount model

Constant Dividend Growth

- Valuing share by viewing its dividends as a constant growth perp: P(0) = Div(1)/ r(E) -

g

Dividends versus investment and growth

Div(t)= earnings(t)/shares outstanding(t) (EPS(t)) * dividend payout rate(t)

- Dividend payout rate- fraction of firm earnings that the firm pays out as dividends

each year

- To increase dividend if constant rate:

o increase earnings (net profit)

▪ change in earnings= new investm * return on new

▪ new investm= earnings*retention rate (fraction that retains for new

investm)

▪ earnings growth rate= change in earnings/earnings= retention*return

on new

▪ g= retention * return

o increase dividend payout rate

▪ ut the fi’s diided to iease iest ill eate alue ad aise

the share price only if new investm generate return > cost of capital

▪ dividend payout rate + retention rate = 1

o decrease # shares outstanding

- earnings per share (EPS) measures firm profitability- total earnings normalised by #

of shares outstanding

- return on new investm: measures ability of a firm to turn investm into earnings (ratio

of new earnings to new investm)

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Valuation principle: price of a security should equal pv of expected cash flows an investor will receive from owning it. Equity: ordinary share: share of ownership in co, which confers rights to any ordinary dividends as well as rights to vote on elections of directors, mergers and other maj events. Security sold by corporations to raise money from investors today in exchange for expected fut paym- receive dividend paym (not guaranteed- ordinary and preference shares) Dividend and capital gains (r(e) is equity cost of capital) Expected total return of the share should equal the expected return of other investments available in the market with equivalent systematic risk. Systematic risk: risk that must be taken if buying stock (eco cycle)- requires risk premium. Idiosyncratic risk: endemic to particular stock (not whole investm portfolio) not rewarded for this risk quod can get rid of it.