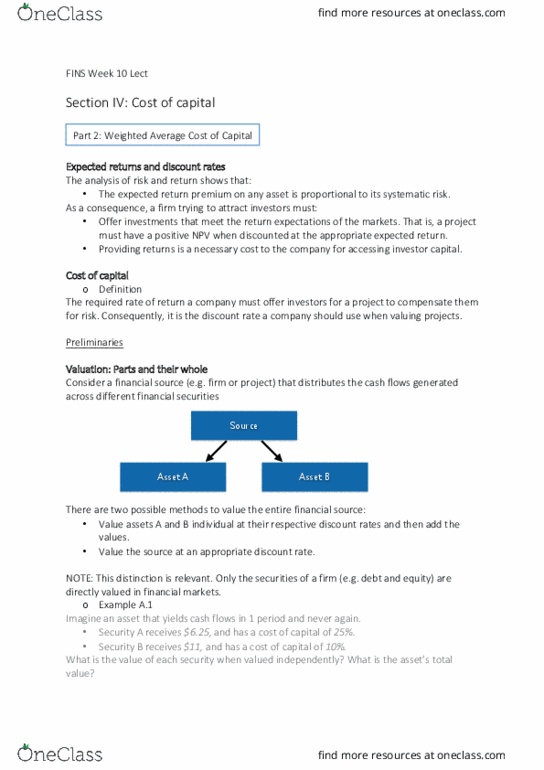

FINS1613 Lecture Notes - Lecture 7: Risk-Free Interest Rate, Risk Premium, Capital Asset Pricing Model

Chapter 13 – Cost of Capital

- Capital structure: relative proportions of debt, equity and other securities the firm

has outstanding

- Market value of E + MV(D) = MV(A) (means D/E is derived from underlying assets)

- Cost of capital: required rate of return a co must offer investors for a project to

compensate them for risk- discount rate used when valuing projects

- Weighted average cost of capital (WACC)

o Weighted ag of a pojet’s osts of apital fo eah seuit used i

financing- weights are fractional aouts of eah seuit’s total pojet

market value

o Expected return premium on any asset is proportional to its systematic risk

▪ Offer investments that meet return expectations of markets- +ve NPV

when discounted at expected return- return necessary cost to co for

investor capital

= Asset cost of capital

r(WACC) = r(E)*E% + r(P)*P% + r(D)*(1-Tc)*D%

- Project as a portfolio: return of a portfolio = weighted avg return of the securities

w/in

o Offer a return = to weighted avg of expected returns → based on market

values

- Firm w/out debt- unlevered vs. debt outstanding = levered (WACC for unlevered =

r(E)

o Values assets by discounting CF at WACC – NPV + total aket alue of fi’s

securities when applied to total firm CF

find more resources at oneclass.com

find more resources at oneclass.com

- Implicitly assumes relative aket alues of fi’s seuities do ot hage o/t

- CAPM limitations: used to find cost of capital for any asset/security- D/E

- Asset/security values must be current w reliable market values → debt

seuities/pef shaes do’t tade feuetl + listed P may be outdated- estimated

CAPM ß unreliable + ordinary shares generally valued using CAPM

- Cost of Debt: Debt paym tax deductible- fi do’t ea full ost of det → cost of

debt used in WACC reflect tax benefits of debt- YTM is expected return on debt

required by investors; r(D)= YTM, T(C)= firm tax rate

o Do’t use CPN ate histoial as det ost of apital- YTM of existing debt

- Unlevered: cost of capital for assets is same as r(E) for equity- FCF to equity holders =

FCF from assets

- Net debt= debt – cash and risk free securities (ie use market value of equity and net

det)

- Cost of Preference shares: Offer fixed dividend- reflect expected return demanded

by investor- constant growth dividend model

→ constant dividend growth model: r(P) = Div/P(0) + g

- Cost of Ordinary shares: Risk free rate (LT gov bonds), market risk premium

histoial ≈ 5.5-7%), appropriate ß reflect project systematic risk (industry avg)

- CAPM: obtain beta of equity or estimate

o Determine risk free rate (yield on treasury bonds)

o Estimate market risk premium (compare historical returns on market proxy

to historical risk free rate)

- Assuptios: average risk, costat D/E ratio (WACC does’t chage accordig to

leverage changes- assume maintain constant ratio), limited leverage effects (only

interest tax deduction- assue other fiacial stress factors are’t sigificat i level

of debt chosen) [also, issuance costs cash outflows

→

internal funds less costly than

external funding]

WACC: determine incremental FCF of investment → WACC → compute value of investment

incl tax benefit of leverage, by discounting incremental FCF of investment using WACC

- Cost of apital fo pojet’s CF he a pojet’s isk diffes fo the fi’s oeall isk

find more resources at oneclass.com

find more resources at oneclass.com

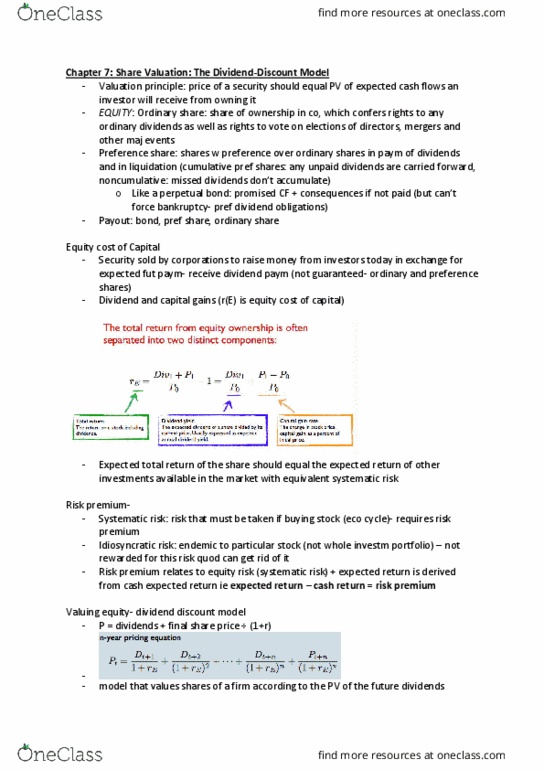

Estimating the cost of equity

CAPM

CDGM

Inputs

- Equity beta

- Risk free rate

- Market risk premium

- Current share price

- Expected dividend next year

- Future dividend growth rate

Assumptions

- Estimated beta is correct

- MRP is accurate

- CAPM is correct model

- Dividend estimate is correct

- Growth rate matches market expectations

- Future dividend growth is constant

Flotation costs

- Cost incurred by co when issuing securities- underwriting, legal, rego

o Incl costs at t=0 expense OR adjust r(E) to account for flotation costs

(assumes issuance costs are recurrent/ongoing expenses

Cost of Capital Part 3

- Tradeoffs between debt and equity

- Debt-to-value ratio (D/D+E)

- Raising capital: selling equity to private investors (control risk of administration +

equity rights)

o VC

o Institutional investors (target high risk)

o Corporate investors (strategic- related industries)

- IPO: provides a way for a successful young firm to raise additional capital

o Seed investors realise profits, firm sell shares extract cash, Board (decrease

share control)

▪ Pricing: generally underpriced (volatility) + generally underperform

the market 3-5years from IPO

▪ Cyclicality: business cycle (IPO vs other source of capital)

o Seasoned equity offering (SEO) occurs when a publicly traded firm sells

additional shares

- Raising debt:

o Private debt- fiaig ot pulil taded aoid ego osts, iestos a’t

really sell the debt e.g bank loans) vs. public debt (publicly traded)

o Debt securities- seniority (during administration), collateral

(secured/unsecured debt- backed by assets), covenants (restrictions on firm

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Capital structure: relative proportions of debt, equity and other securities the firm has outstanding. Market value of e + mv(d) = mv(a) (means d/e is derived from underlying assets) Cost of capital: required rate of return a co must offer investors for a project to compensate them for risk- discount rate used when valuing projects. = asset cost of capital r(wacc) = r(e)*e% + r(p)*p% + r(d)*(1-tc)*d% Project as a portfolio: return of a portfolio = weighted avg return of the securities w/in: offer a return = to weighted avg of expected returns based on market values. Firm w/out debt- unlevered vs. debt outstanding = levered (wacc for unlevered = r(e: values assets by discounting cf at wacc npv + total (cid:373)a(cid:396)ket (cid:448)alue of fi(cid:396)(cid:373)"s securities when applied to total firm cf. Implicitly assumes relative (cid:373)a(cid:396)ket (cid:448)alues of fi(cid:396)(cid:373)"s se(cid:272)u(cid:396)ities do (cid:374)ot (cid:272)ha(cid:374)ge o/t. Capm limitations: used to find cost of capital for any asset/security- d/e.