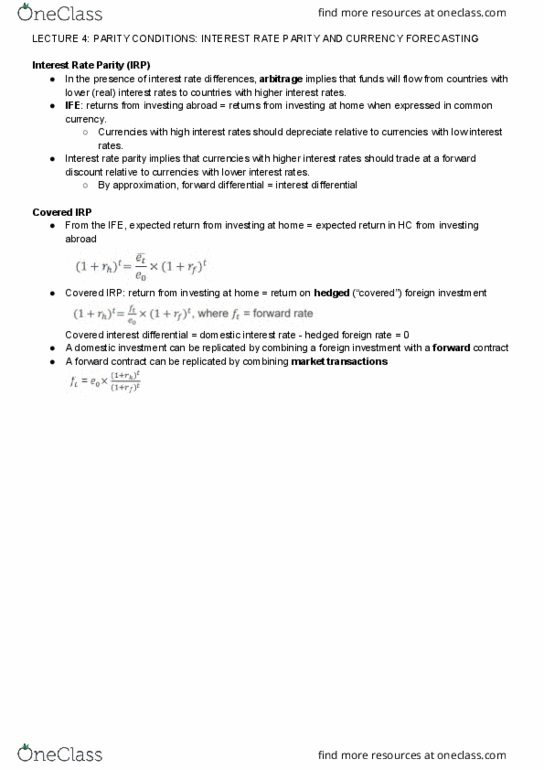

FINS3616 Lecture Notes - Lecture 4: Interest Rate Parity, Foreign Exchange Market, Arbitrage

3 – Interest Rate Parity

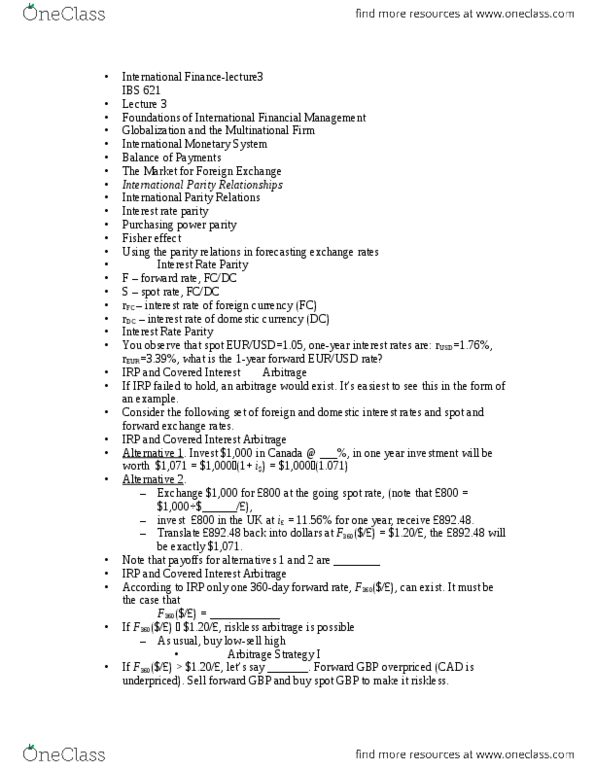

Two ways to buy a currency forward:

1. Enter into a forward contract

2. Borrow the domestic currency, buy foreign currency on spot market and invest for

term

Why should interest rate parity hold?

• If not, arbitrage possibilities would exist (barring any government controls)

• Forces relationship between forward/spot rates and the interest rate differential

between two countries

Deriving covered interest rate parity

• Expressing that when the forward rate is priced correctly, an investor is indifferent

between investing at home or abroad

• General expression for interest rate parity:

• Interest rate parity and forward premium discounts:

Forward premium if id > if

Forward discount if id < if

External currency market

• Bank market for deposits and loans that are denominated in foreign currencies (from

the perspective of the bank)

Market prospers because it is a way to get around reserve requirements, which

are generally lower in this market

• Interest rates lower due to avoided regulations and increased competition (i.e. supply

of said currency)

Annualised rate * (1/100) * (number of days/360) = de-annualised rate

• Influence over other markets

External currency market influences rates elsewhere

Loans to investors/corporations are based on these interbank markets

Most important is the LIBOR

Does covered interest rate parity hold?

• Prior to 2007, documented violations of interest rate parity were very rare

• Frequency, size and duration of apparent arbitrage opportunities do increase with

market volatility – especially around GFC

Why deviations from interest rate parity may seem to exist

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Two ways to buy a currency forward: enter into a forward contract, borrow the domestic currency, buy foreign currency on spot market and invest for term. Why should interest rate parity hold: forces relationship between forward/spot rates and the interest rate differential. If not, arbitrage possibilities would exist (barring any government controls) between two countries. Deriving covered interest rate parity: expressing that when the forward rate is priced correctly, an investor is indifferent between investing at home or abroad, general expression for interest rate parity: External currency market: bank market for deposits and loans that are denominated in foreign currencies (from the perspective of the bank) Market prospers because it is a way to get around reserve requirements, which are generally lower in this market. Interest rates lower due to avoided regulations and increased competition (i. e. supply of said currency) Annualised rate * (1/100) * (number of days/360) = de-annualised rate. Loans to investors/corporations are based on these interbank markets.