ACCY111 Lecture 4: Chapter 4 - Adjusting the accounts and preparing financial statements

Chapter 4 (Wk4) - Adjusting the accounts and preparing financial statements

1. Describe the difference between the cash basis and accrual basis of measuring profit.

2. Explain the accounting cycle and the need for end of accounting period adjusting entries.

3. Identify and prepare the different types of adjusting entries.

4. Prepare an adjusted trial balance and financial statements.

Measurement of profit:

Cash basis

• Income is recorded when cash is received.

• Expenses are recorded when cash is paid.

• This method does not recognise income when goods or services are performed on credit.

Accrual basis

• Income recognised when the anticipated inflow of economic benefit can be reliably measured.

• Expenses recognised when the consumption of benefits can be reliably measured.

Income- Accounting definition:

Increases in economic benefits during the period in the form of inflows or enhancements of assets

or decreases in liabilities. Result in increases in equity. Not contributions from the owners.

• Recognised at the fair value of assets received.

Expenses - Accounting definition:

Decreases in economic benefits during the period in the form of outflows or depletions of assets or

incurrences in liabilities. Result in decrease in equity. Not distributions to the owners.

• Recognised in the period in which the consumption of costs can be measured.

Temporary (nominal) accounts:

• Income statement accounts.

• Reduced to zero balance at the end of each accounting period. (process called closing the

accounts).

Permanent (real) accounts:

• Balance sheet accounts.

• Ending balances carried forward to next accounting period.

The accounting cycle - expansion to include adjusting entries

find more resources at oneclass.com

find more resources at oneclass.com

Chapter 4 (Wk4) - Adjusting the accounts and preparing financial statements

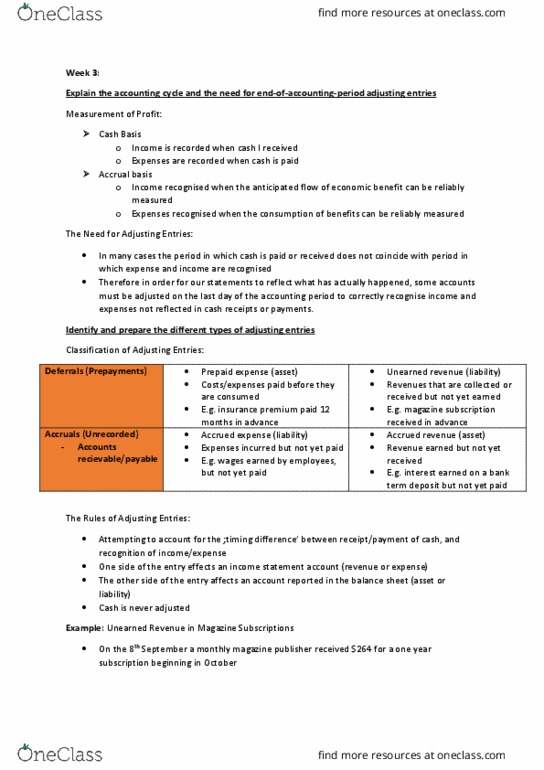

The need for adjusting entries:

• In many cases the period in which cash is paid or received does not coincide with period in

which expense and income are recognised.

• Therefore, in order for our statements to reflect what has happened, some accounts must be

adjusted on the last day of the accounting period to correctly recognise income and expenses

not reflected in cash receipts or payments.

Classification of adjusting entries:

• Adjusting entries: revenue

• Unearned revenue: revenues collected in advance, but not yet earned. E.g. magazine

subscription received in advanced.

• Accrued revenue: revenues earned, but not yet received in cash or entered. E.g. interest

earned on a bank term deposit but not paid.

• Adjusting entries: expenses

• Prepaid expenses: expenses paid for before they are consumed. E.g. insurance premium paid

12 months in advance.

• Accrued expenses: expenses incurred, but not yet paid for or entered. E.g. wages earned by

employees, but not yet paid.

• Deferrals (Pre-payments):

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Identify and prepare the different types of adjusting entries. Income is recorded when cash is received: expenses are recorded when cash is paid, this method does not recognise income when goods or services are performed on credit. Income recognised when the anticipated inflow of economic benefit can be reliably measured: expenses recognised when the consumption of benefits can be reliably measured. Increases in economic benefits during the period in the form of inflows or enhancements of assets or decreases in liabilities. Not contributions from the owners: recognised at the fair value of assets received. Decreases in economic benefits during the period in the form of outflows or depletions of assets or incurrences in liabilities. Not distributions to the owners: recognised in the period in which the consumption of costs can be measured. Income statement accounts: reduced to zero balance at the end of each accounting period. (process called closing the accounts).