FIN111 Lecture Notes - Ordinary Income, Steady-State Economy, Cash Flow

• Future and present values of multiple cash flows

• Valuing level cash flows: annuities and perpetuities

• Comparing rates: the effect of compounding periods

• Loan amortisation (ordinary annuity)

1. Describe the four types of secondary markets

2. Features of ordinary and preference shares

3. Describe how the general dividend valuation model values a share

4. Discuss the assumptions that are necessary to make the general dividend valuation model easier

to use, and be able to use the model to calculate the value of a company's ordinary shares

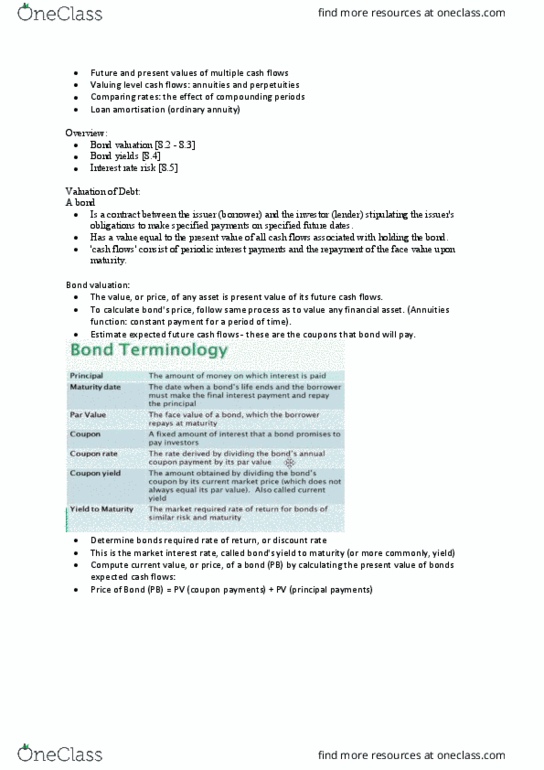

Only cover Parrino Pg. 302-320

Shares:

• Equity instrument giving the holder ownership rights in a firm.

• Shareholders have the right to vote for the managers of the firm and to receive profits the firm

makes.

• There is no guarantee that the shares will increase in value (capital gain) or that dividends will

be paid.

Two basic types of corporations:

• Privately held: typically small and owned by a few people who are closely involved in running

the business. Their shares are not traded publicly. E.g. proprietary limited (PtyLtd)

• Publicly held: firms listed/traded on a stock exchange. Typically owned by a large group of

people who employ management to run the business for them. E.g. limited (Ltd)

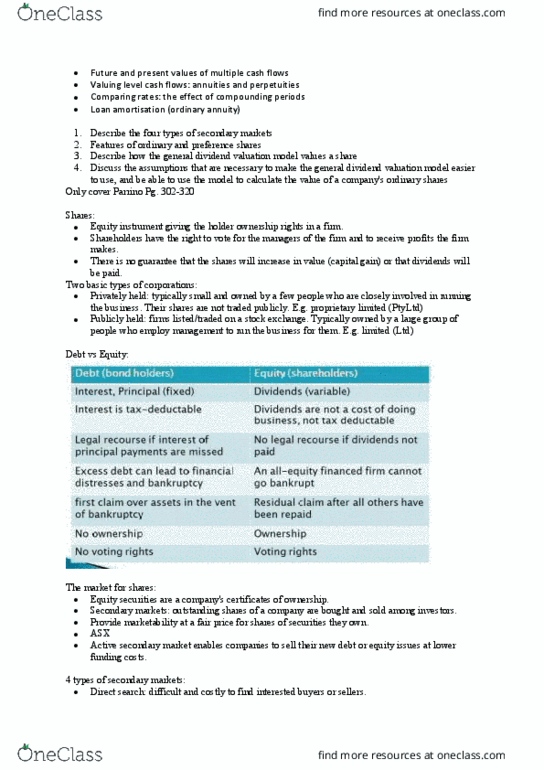

Debt vs Equity:

The market for shares:

• Equity securities are a company's certificates of ownership.

• Secondary markets: outstanding shares of a company are bought and sold among investors.

• Provide marketability at a fair price for shares of securities they own.

• ASX

• Active secondary market enables companies to sell their new debt or equity issues at lower

funding costs.

4 types of secondary markets:

• Direct search: difficult and costly to find interested buyers or sellers.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Future and present values of multiple cash flows: valuing level cash flows: annuities and perpetuities, comparing rates: the effect of compounding periods. Two basic types of corporations: privately held: typically small and owned by a few people who are closely involved in running the business. E. g. proprietary limited (ptyltd: publicly held: firms listed/traded on a stock exchange. Typically owned by a large group of people who employ management to run the business for them. Could be debt or equity however, legally, preference shares are equity: like dividends on ordinary shares, preference share dividends are taxable. D1 = next period dividend: the valuation model for constant growth share: The relationship between r and g: constant growth dividend model yields solutions that are invalid whenever dividend growth rate equals or exceeds discount rate. If g > r, the present value of the dividend gets bigger and bigger rather than smaller and smaller as it should.