22107 Lecture Notes - Lecture 9: Total Absorption Costing, Fixed Cost, Variable Cost

UTS 2014 – Accounting for Business Decisions A

Page 50

Evaluate the impact of product costs and period costs on a company’s income statement

and balance sheet.

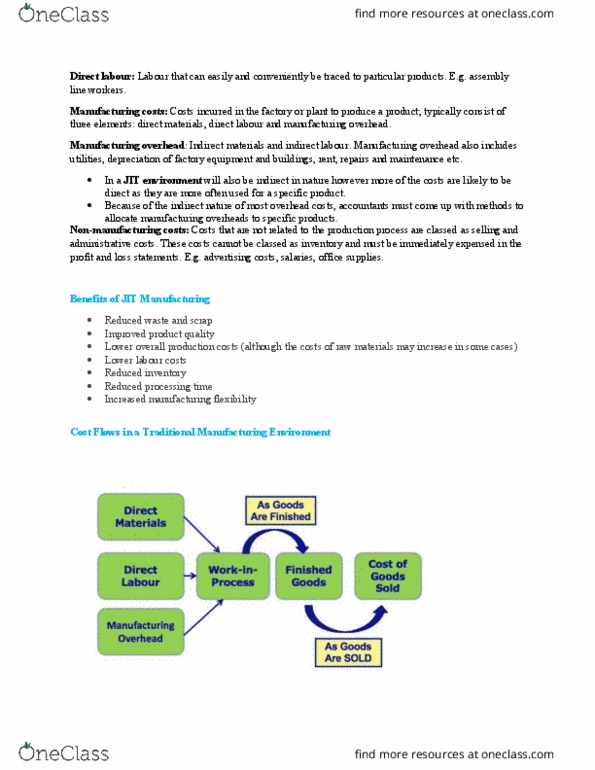

As mentioned before, manufacturing costs attach to products during manufacturing process.

Until the sale of the product, the costs of manufacturing are included in one of three

inventory accounts – raw materials, work in process and finished goods.

These inventory accounts appear on the BALANCE SHEET.

Only when product is sold are manufacturing costs expensed as COGS on income statement.

On the other hand, non-manufacturing costs are expensed immediately on the income

statement in the period in which they are incurred.

LECTURE 9 – COST VOLUME PROFIT ANALYSIS

LEARNING OBJECTIVES – COST BEHAVIOUR

Cost behaviour - how costs react to changes in production volume or other levels of activity.

Describe the nature and behaviour of fixed and variable costs.

Fixed costs are the costs that remain the same in total when production volume increases or

decreases but vary per unit.

- Fixed costs remain the same irrespective of production volume (or the level of activity).

UTS 2014 – Accounting for Business Decisions A

Page 51

- Consequently, fixed cost per unit always decreases when production volume increases.

- EXAMPLES – Facility-level costs such as rent, depreciation of a factory building, the salary of

a plant manager, insurance and property taxes are likely to be fixed costs.

Variable costs are the costs that stay the same per unit but change in total as production

volume increases or decreases.

- Variable costs vary in direct proportion to changes in production volume/level of activity.

- As a result, they are constant when expressed as per unit amounts.

- As production increases, variable costs increase in direct proportion to change in volume; as

production decreases, variable costs decrease in direct proportion to the change in volume.

- Examples include direct material, direct labour (if paid per unit of output) and other unit-

level costs, such as factory supplies, energy costs to run factory machinery and so on.

FIXED COSTS versus VARIABLE COSTS:

The relevant range is the normal range of production that can be expected for a particular

product and company.

Step costs refer to the costs that vary with activity in steps and may look like and be treated

as either variable or fixed costs; step costs are technically not fixed costs but may be treated

as such if they remain constant within a relevant range of production.

Mixed costs are the costs that include both a fixed and a variable component – making it

difficult to predict how the cost changes as production changes (unless the cost is first

separated into its fixed and variable components).

E.g. railway’s internet service has fixed costs of $50/month + variable costs of $3/HR of use.

Identify the difference between variable costing and absorption costing.

Absorption costing is a method of costing in which product costs include direct materials,

direct labour, and fixed and variable overhead – required for external financial statements

and for income tax reporting.

Variable costing is a method of costing in which product costs include direct materials,

direct labour and variable overhead; fixed overhead is treated as a period cost – consistent

with a focus on cost behaviour.

UTS 2014 – Accounting for Business Decisions A

Page 52

Key difference between absorption and variable costing is the treatment of fixed overhead.

o Under absorption costing, fixed overhead is treated as a product cost – added to the cost of

the product and expensed only when the product is sold. Under variable costing, fixed

overhead is treated as a period cost and is expense when incurred.

o The impact of this difference on reported income becomes evident when a company’s

production and sales are different (i.e. no. of units produced is greater/less than units sold).

Because absorption costing treats fixed overhead as a product cost, if units of production

remain unsold at year-end, fixed overhead remains attached to those units and is included

on the balance sheet as an asset as part of the cost of inventory.

Using variable costing, all fixed overhead is expensed each period, regardless of the level of

production or sales. Consequently, when production is greater than sales and inventories

increase, absorption costing will result in higher net income than variable costing.

LEARNING OBJECTIVES – COST-VOLUME-PROFIT-ANALYSIS

Cost-volume-profit (CVP) analysis is a tool that focuses on the relationship between a

company’s profits and (1) the selling prices of products of services, (2) the volume of

products or services sold, (3) the per unit variable costs, (4) the total fixed costs and (5) the

mix of products or services produced.

The assumptions of CVP analysis are:

- Expenses can be classified as either variable or fixed.

- CVP relationships are linear over a wide range of production and sales.

- Selling price, unit variable cost and total fixed costs will not vary within the relevant range.

- Volume is the only cost driver.

- The relevant range of volume is specified.

- The sales mix used to calculate the weighted-average contribution margin is constant.

- The amount of inventory is constant – number of units produced = number of units sold.

Use the contribution margin in its various forms to determine the impact of changes in

sales on profit.

The three approaches to calculate break even…

Conventional income statement

Contribution margin income statement

Contribution margin ratio

Document Summary

Evaluate the impact of product costs and period costs on a company"s income statement and balance sheet. As mentioned before, manufacturing costs attach to products during manufacturing process. Until the sale of the product, the costs of manufacturing are included in one of three inventory accounts raw materials, work in process and finished goods. These inventory accounts appear on the balance sheet. Only when product is sold are manufacturing costs expensed as cogs on income statement. On the other hand, non-manufacturing costs are expensed immediately on the income statement in the period in which they are incurred. Cost behaviour - how costs react to changes in production volume or other levels of activity. Describe the nature and behaviour of fixed and variable costs. Fixed costs are the costs that remain the same in total when production volume increases or decreases but vary per unit. Fixed costs remain the same irrespective of production volume (or the level of activity).