22107 Lecture Notes - Lecture 5: Barcode, Inventory Turnover, Liquid Oxygen

Lecture 7 - 3rd May 2018

Inventory

LO1 Inventory (lifeblood of any retailer)

→ Inventory is a tangible resource that is held for resale in the normal course of operations. The

phrase "intended for resale" differentiates inventory from other assets.

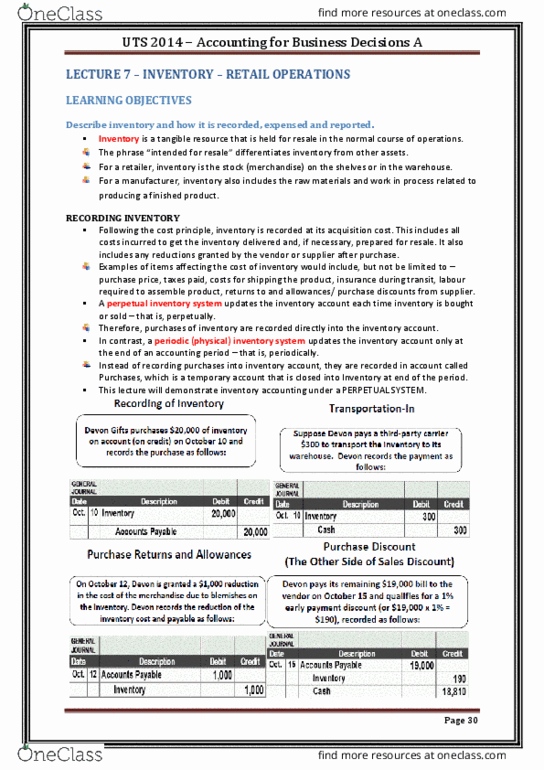

→ Following the cost principle, inventory is recorded at its acquisition cost. This includes all costs

incurred to get the inventory delivered or prepared for resale.

Examples of costs included in inventory:

• Purchase price

• Any taxes or duties paid

• Costs for shipping the product

• Insurance during transit

• Labour required to assemble the product

• Returns and allowances from the vendor

• Purchase discounts from the vendor (seller)

Types of Inventory Systems

• Both the recording of inventory purchases and the recording of cost of goods sold depends on a

company's inventory system. Under a perpetual system, cost of goods sold is updated each time

inventory is sold – perpetually.

• Under a periodic system, cost of goods sold is calculated and recorded only at the end of the

period – periodically. The periodic method is shown in the chapter appendix (LO8)

Reporting inventory and Cost of Goods Sold

• Inventory is expected to be sold within a year and is reported on the statement of financial

position (balance sheet) as a current asset.

• As its usually large, COGS is reported as a separate line on the statement of comprehensive

income (income statement/profit and loss statement)

LO2 Inventory Costing

To determine the cost of inventory sold, companies can use one of the following inventory costing

methods:

→ Specific identification

→ First in, First out (FIFO)

→ Last in, First out (LIFO)

→ Moving average

(need to make an assumption)

Calculating Moving (weighted) average:

LO3 Understand the income and tax effects of inventory cost flow

assumptions

Accountants can legally produce different profit figure. Inventory flow assumptions are one way in

which different expenses can be calculated (in AUS, we don’t use LIFO)

Comparing Inventory Costing Methods

→ Specific identification is not possible if one item cannot be distinguished from another (e.g. all

have same bar code). Then we need to make an inventory flow ASSUMPTION such as: