ACCT1101 Lecture 1: ACCT1101 NOTES S1

ACCT1101

Page 1

FINANCIAL ACCOUNTING

Chapter 1: Decision making and the role of accounting

ACCOUNTING

Accounting: is a service activity, its function is to interpret and provide financial information to assist in

decision making (steps 2,3,4 in decision making process)

Accounting is used in business, government, charities, and not for profit organisations.

ACCOUNTING ENVIRONMENT

•accounting evolves as a society and business changes

•some changes include: rapid developments in information and communication technologies, increasing

demand for a range of information about organisational impact, development of international regulations

and standards

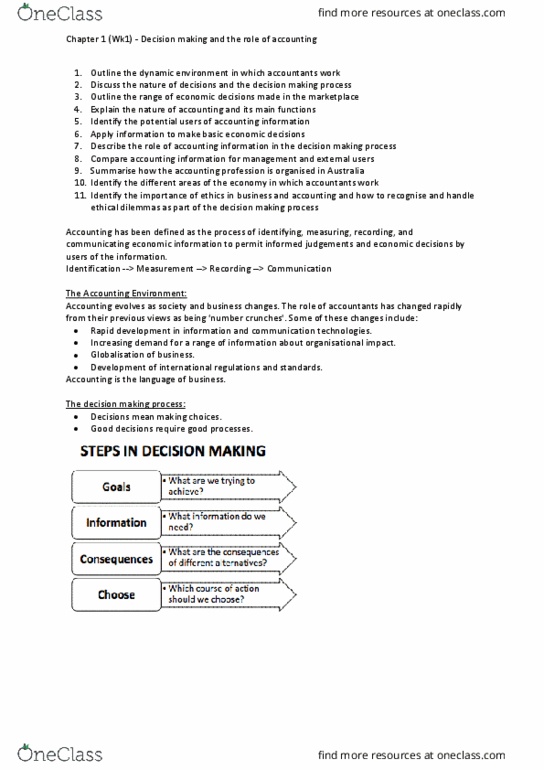

THE DECISION MAKING PROCESS

•decision making choices include: how we spend our time, how we spend our resources, competing

options available

•steps in decision making:

1. goals

2. Information

3. Consequences

4. Choose

•Economic resources have a cost as they are scarce. We must consider personal taste, social factors,

environmental factors, religious and/or moral factors, government policy

ACCOUNTING DEFINED

Identification: transactions (internal and external)

Measurement: quantification in monetary terms ($)

Recording: classification, summarisation

Communication: accounting reports, analysis and interpretation

•the uses of accounting information is external and internal users

FINANCIAL ACCOUNTING

•External focus

•reports information (performance and position)

•financing and investing

•legal compliance

•highly regulated

TYPES OF ACCOUNTING

PUBLIC ACCOUNTING: Accountants who offer their

services to the public for free

•can vary in size depending on international

organisations

•have four main areas in which they specialise:

auditing and assurance services, taxation services,

advisory services, insolvency and administration

ETHICS IN ACCOUNTING

Ethics in business: important in all business transactions

Ethics and professional accounting:

ACCT1101

Page 2

Ethics in practice: identify the ethical issue, analyse key issues and stakeholders, assess consequences,

select appropriate course of action.

Chapter 2: Financial Statements for Decision Making

TYPES OF BUSINESS ENTITIES

Single Proprietorship or sole trader

•owned by one person

•simple to set up

•common form of business structure

•seperate accounting entity, not seperate legal entity

Partnership:

•owned by two or more individuals (more capital and

resources)

•simple to set up

•seperate accounting entity not seperate legal entity

•jointly and separately liable (legal)

•each partner pays tax seperate so that they can

receive seperate income from the company

Company or Corporate

•owned by shareholders

•seperate accounting entity

•seperate legal entity

•Private Company:

•Public Company:

Limited Liability

•protection for owners

Main differences between a sole trader, partnership and a company make a table and insert here

1. profit/ loss sharing

2. capital contributed at the start of the company/ formation

3. dissolution/winding up of the entity

4. Legal liability

5. Tax Liability

BASIC FINANCIAL STATEMENTS

•accounting is and information system designed to communicate financial information to interested users

for making economic decisions

•financial statements are the outcome of the accounting process,are a primary information source for

users, and are useful for many decisions

3 PRIMARY INFORMATION TYPES

•Financial performance: (income statement) the ability of the entity to utilise its assets effectively and

efficiently

•tells if management was able to affectively use resources to generate profits

•Financial position: (balance sheet)the financial resources controlled by the entity, financial structure and

the measure of liquidity and solvency

•tells what financial assets you own

•Cash Flow Statement:

BUSINESS ACTIVITIES

Cash Movements: the ability of the entity to generate cash flow in the there areas:

1. operating activities: the provision and payment for goods and services

2. Investing activities: the acquisition and disposal of long term assets

3. financing activities: The raising of funds for an entity to carry out its operating and investing activities

ACCT1101

Page 3

THE BALANCE SHEET

•reports financial position of an entity at a specific point in time

•shows assets, liabilities and equity of an entity

•represents the accounting equation —> Assets=Liabilities + Equity

The accounting formula rearranged:

Account Format: Assets= Liabilities + Equity Narrative Format: Assets - Liabilities = Equity

Assets: resources controlled by the entity as a result of past transactions or events from which future

economic benefits are expected to flow to the entity

Liabilities: present obligations of an entity arising from past transactions or events, the settlement which is

expected to result in an outflow of resources from the entity

Equity: the residual interest of the owner/s in the assets (less liabilities) of the equity

Assets - Liabilities = Net Assets

Net Assets = Equity

Sometimes called Capital or Accumulated Surplus/ Funds

THE INCOME STATEMENT

•reports financial performance over a specific period of the

•shows income and expenses (e.g. income>expenses=profit OR

income<expenses=loss)

•sometimes called profit or loss statement or Operating Statement

Income: increases in economic benefits in the form of inflows or

enhancements of assets or decreases of liabilities that results in

equity, other than those relating to equity participants

it is activity involved with other entities, not the owner contributing

capital ($)

-interest recieved, dividends, commission,

Expenses: decreases in economic benefits in the form of outflows or

incurrences of liabilities that rest;t in decreases in equity, other than

this relating to equity participants.

Drawings are not an expense!

-electricity, don't have to be paid in cash to

qualify as an expense

THE STATEMENT OF CHANGES IN EQUITY

The initial capital of $437 330 has the profit for

the first year added to it ($437 330+136 350).

this equals $573 680. The drawings must be

taken away ($573 680-87 000=$486 680). This

means that the profit for that year is $49 350.

Document Summary

Chapter 1: decision making and the role of accounting. Accounting: is a service activity, its function is to interpret and provide nancial information to assist in decision making (steps 2,3,4 in decision making process) Accounting is used in business, government, charities, and not for pro t organisations. Accounting environment: accounting evolves as a society and business changes, some changes include: rapid developments in information and communication technologies, increasing demand for a range of information about organisational impact, development of international regulations and standards options available. The decision making process: decision making choices include: how we spend our time, how we spend our resources, competing, steps in decision making, goals. 2: consequences, choose, economic resources have a cost as they are scarce. Information environmental factors, religious and/or moral factors, government policy. Communication: accounting reports, analysis and interpretation: the uses of accounting information is external and internal users.