ACCT1101 Lecture 1: ACCT1101 Practical Lecture Notes

Practical Lecture Notes

Practical Lecture Week 8:

-Cash management and control

-> bank reconciliations

-Statement of cash flows

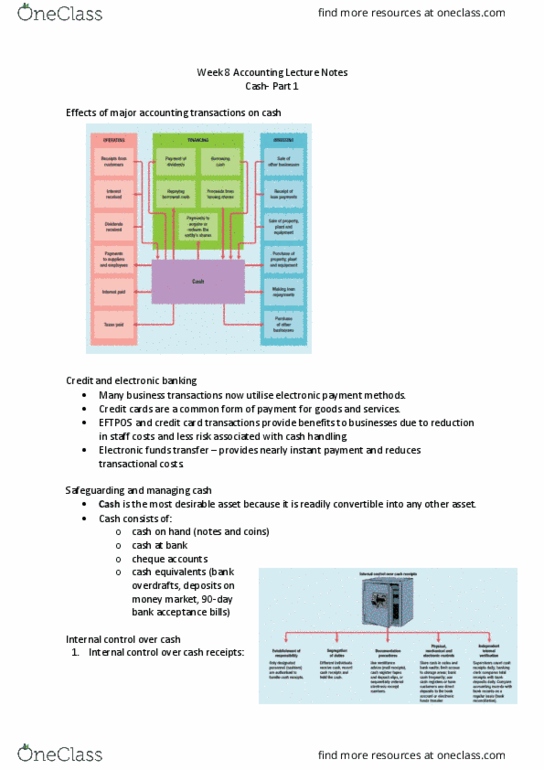

CASH MANAGEMENT AND CONTROL

•Cash: cash on hand and things which are readily convertible to cash

-incl. cheques, credit card duplicates, postal notes, EFT’s,etc

-not including accounts receivable, bills receivable

•Cant have restrictions, must be readily available

•Good control is essential

-essential control: deposits cash to bank each day and make all payments by authorised cheque or

by electronic fund transfer

•Remember: Bank statement is from Bank’s point of view - CR on bank statement means they hold your

money (liability to them) = DR (cash asset) in your records

BANK RECONCILIATION

•Reconciles cash at bank with the bank statement

•compare cash journals with bank statement to identify reconciling

items:

-not in bank statement yet

-unpresented cheques

-outstanding deposits

-items originating in bank statement

-interest and bank fees

-cheques dishonoured etc

-error by us or the bank

STATEMENT OF CASH FLOWS

•how much cash was generated and where did

it come from?

•how much cash was used and where did it go?

•how much cash does the entity have at the end

of the year?

•how much cash obtained to pay off non current

liabilities and acquire new non current assets

during the period?

•how were the cash proceeds from a new

issue of shares used?

•why has the cash position of the company

decreased when the company reported a

profit for the period?

•cash flow information enables users to

assess the liability of the entity to distribute

cash in the future:

-to meet financial commitments or

-perhaps to pay dividends

•Much of the information about cash is contained in the notes including:

•types of cash and cash equivalents

•types of non cash financing a

•the access to additional sources of cash

RECONCILIATION OF NET PROFIT TO OPERATING CASH FLOWS

•Net profit (from income statement)

•add back non cash expenses (e.g. depreciation)

•deduct increases in current assets (+ decreases)

•add increases in current liabilities (- decreases)

Practical Lecture Week 9:

Receivables

-bad debts

Inventories

-accounting for inventory costs when prices change

RECEIVABLES

•valuation is a key issue - how much will actually be received?

•allowance for doubtful debts is a contra account which reduces accounts receivable - its and estimate of

amounts not collectable

-percentage of net credit sales- what % of sales are not generally recovered? Not dependant on

what is already in allowance for doubt debts

-ageing- % collectable depending on days overdue. Calculate total amount for all receivables and

adjust allowance account balance. Don't include GST.

•To write off a particular account when bad, reduce A/R, GST Collections and Allowance for Doubtful

Debts (not bad debts exp)

INVENTORIES

Specific Identification

-particular inventory is identified and when sold its own cost is used to reduce inventory and record cost of

sales

FIFO

-cost of first inventory purchased is cost used when inventory sold

LIFO

-cost of last inventory purchased is cost used when inventory sold. **not allowed**

Average Cost

-take average of all purchases to record as cost of inventory sold and on hand

-Perpetual system = moving average

-Periodic system =weighted average

Problem 18.5

Exercise 12.4

E. The net credit sales method and the ageing of accounts receivable method both calculate a different

balance for the Allowance for Doubtful Debts. The net credit sales method calculates the adjusting entry for

Bad Debts Expense as a percentage of net credit sales. The calculation forms the basis of the adjusting

entry. The ageing of an accounts receivable calculates a required ending balance for the Allowance for

Doubtful Debts. The adjusting entry for Bad Debts Expense is calculated by taking into account any

opening balance in the allowance account to achieve the desired ending balance. Since the two methods

involve calculations based on different amounts the resulting balances on Allowance for Doubtful Debts

accounts will be different, and hence the net accounts receivable disclosed in the balance sheet will also be

different.