MAA261 Lecture Notes - Lecture 6: Efficient-Market Hypothesis, Book Value

Document Summary

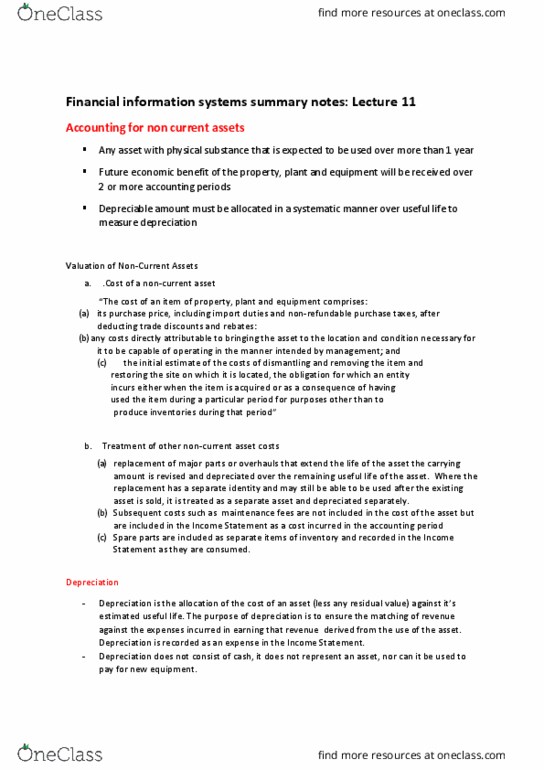

Week 6: accounting for property, plant and equipment. Explain the nature of property, plant and equipment. Compute the cost of property, plant and equipment. Cost = the amount of cash or the fair value of other consideration given to acquire an asset. Purchase price (including duties and non-refundable taxes, trade discounts etc. ) Estimate of required costs of dismantling, removing, restoring. Fair value = the price would be received in selling an asset in an efficient market. Other issues: cost recognised should only include reasonable and necessary expenditures, deferred payment may require recognition of interest component (present value calculation) Land and land improvements: borrowing costs, qualifying assets, equipment acquired for safety or environmental reasons. Apportion the cost of a lump sum payment for multiple asset acquisitions. Purchase of many assets at once: total cost apportioned over the identifiable assets, cost allocated on basis of fair value, each asset recorded at individual cost.