ACCT10001 Lecture Notes - Lecture 5: Cookie Jar, Write-Off, Book Value

29 Aug 2018

School

Department

Course

Professor

Document Summary

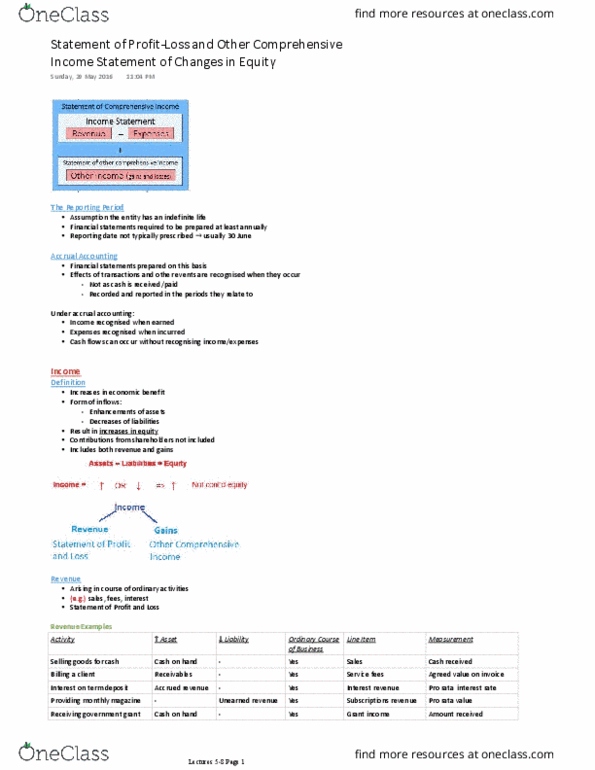

Income statement: a measure of performance combining two elements, the sources of revenue and other gains earned by the entity, the consumption of benefits (depletion of assets) and other losses incurred by the entity. Is it the increase in assets that triggered the income: or is it the increase in income that triggered the increase in asset, they occur simultaneously. Line item in the income statement disaggregated note disclosure: revenue recognition policies. Other revenue in the ordinary course of business: an entity rents out excess office space. Line item in the income statement: by nature: wages & salaries, depreciation, by function: selling, distribution, administrative, note disclosures, disaggregate information, recognition policies. Expenses relating to inventory: as sales occur, future benefit of inventory is consumed, as a service is provided, supplies of materials are consumed. If inventory if identified as missing, inventory is derecognised. Expenses relating to non-current assets: systematic allocation of cost over estimated useful life depreciation and amortisation, recognition.