ACCT20001 Lecture Notes - Lecture 4: Indirect Costs, Cost Driver, Boeing

16 May 2018

School

Department

Course

Professor

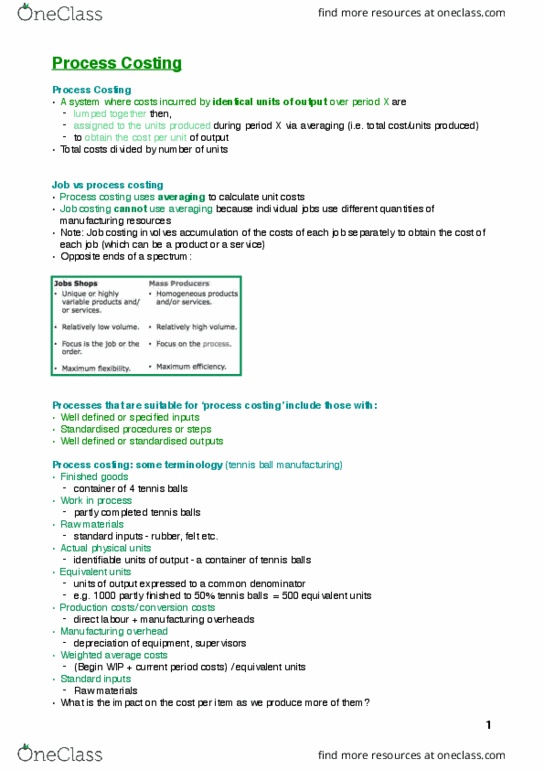

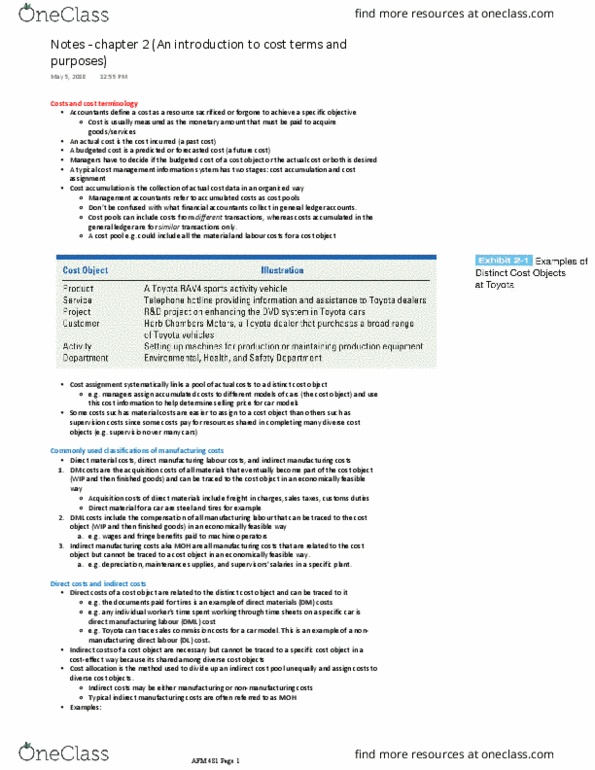

Cost assignment and Job Costing

Summary of Cost Classification

•Direct vs Indirect: depends on traceability of the cost object, which in turn depends on:

-Cost object selected

-Physical and Economic feasibility to trace

•Behaviour with regard to volume of output

-Variable vs fixed

•Inventoriable vs Non-Inventoriable (based on accounting standards)

-Merchandising: cost of purchase + freight in

-Manufacturing: cost of raw materials purchase + freight-in + cost of conversion

-Cost of conversions = direct labour + indirect manufacturing

Why we need to assign costs

Assigning costs to cost objects

1. Direct Costs

•Direct labour

-Traced to cost objects as it is incurred

-E.g. record how many actual hours did Worker A spend on the cost object and multiply by

actual hourly wage

•Direct materials

-Traced to cost objects as it is incurred

-e.g. record how much actual materials used for each cost object and multiply with actual

materials cost

2. Indirect Costs (overheads)

•Allocate to cost object using an allocation base (or cost driver)

•For manufactures, whether we allocate

-Manufacturing indirect costs; OR

-Manufacturing and non-manufacturing indirect costs (i.e. total value chain costs)

-Depends on the purpose of cost assignment (what do we want to know?)

•If for financial accounting (inventory valuation) purposes, then only manufacturing indirect

costs will be allocated

•But what if we want to know about the ‘full-cost’ of a job or some other cost object?

1

Cost Drivers

•A cost driver provides a measure of activity that explains the cost objects use of the

indirect cost

-Usually the allocation base

-Cost pool —> allocate to cost object

•Criteria used to select appropriate cost drivers include:

-cause and effect

-benefits received

-fairness or equity

-ability to bear

-behavioural factors

•Using an incorrect cost driver may mean:

-the cost assigned may result in over-costing or under-costing the cost object

-the influence on managerial behaviour - incorrect decision-making

•Cost drivers can be classified as:

•volume drivers - use a measure of output to assign indirect costs

-e.g. labour hours, units of output

•activity drivers

Determining the allocation rate

Steps in the allocation process:

1. Develop the cost allocation formula

•Identify indirect costs to be allocated

•Select appropriate cost driver

2. Calculate the indirect cost rate

•Divide indirect costs by total cost driver usage

3. Allocate cost to the cost object

•Calculated by multiplying indirect cost rate by cost object’s use of cost driver

•To start the allocation process, entity must decide on number of indirect cost pools

•A cost pool is a group of similar individual costs on a departmental or some other basis

-An allocation formula is developed for each cost pool

-An indirect cost rate is used to assign the cost to the cost object

•Determination of an actual indirect cost rate is not possible until the end of the period

-To avoid delay and so monthly fluctuations in cash flows, entity may use a predetermined

indirect cost rate based on budgeted costs

-This provides a benchmark against which to measure actual costs

•As the number of cost pools increases, the accuracy of cost information increases

A costing framework

•Simple costing system to determine full cost of a cost object:

2

Document Summary

Summary of cost classi cation: direct vs indirect: depends on traceability of the cost object, which in turn depends on: Physical and economic feasibility to trace: behaviour with regard to volume of output. Variable vs xed: inventoriable vs non-inventoriable (based on accounting standards) Merchandising: cost of purchase + freight in. Manufacturing: cost of raw materials purchase + freight-in + cost of conversion. Cost of conversions = direct labour + indirect manufacturing. Assigning costs to cost objects: direct costs, direct labour. E. g. record how many actual hours did worker a spend on the cost object and multiply by actual hourly wage: direct materials. Traced to cost objects as it is incurred. E. g. record how much actual materials used for each cost object and multiply with actual materials cost. Indirect costs (overheads: allocate to cost object using an allocation base (or cost driver, for manufactures, whether we allocate. Manufacturing and non-manufacturing indirect costs (i. e. total value chain costs)