ACCT20002 Lecture Notes - Lecture 8: Deferred Tax, Corporate Tax, Book Value

7 Sep 2018

School

Department

Course

Professor

Document Summary

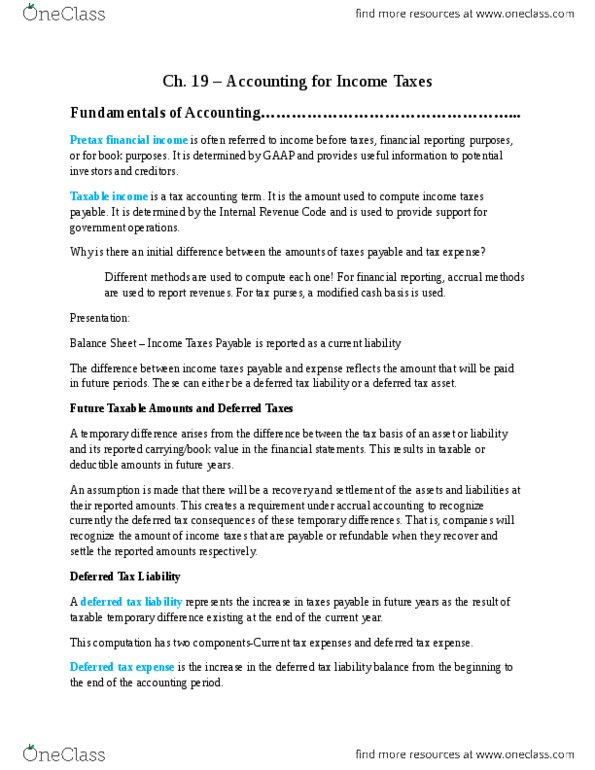

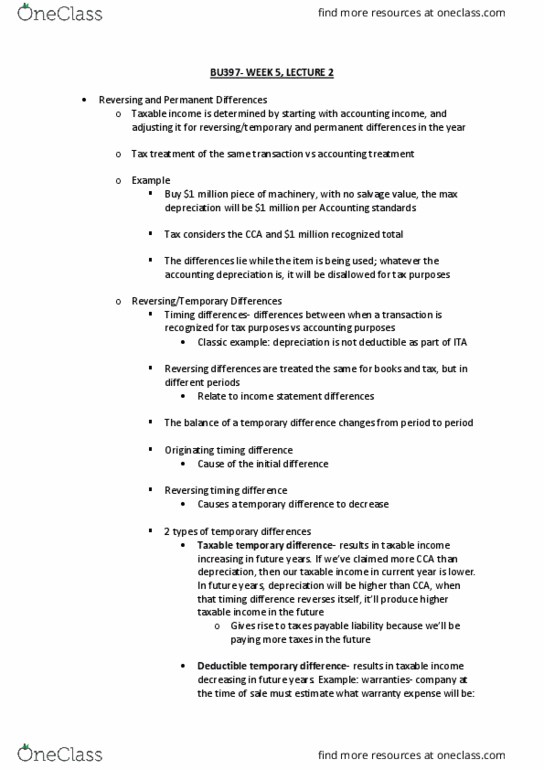

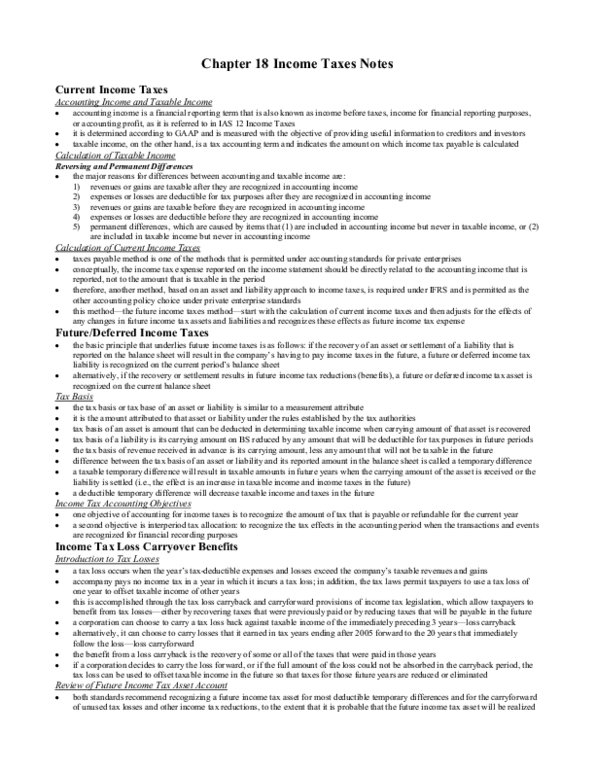

Tax payable approach - no longer used: calculate tax liability via: Taxable income x corporate tax rate (currently 30%: adjusting journal entry to raise expense and liability: Cr income tax payable (l: so, a company with taxable income of m would make the above adjusting entry of k. Ignores the di erences between accounting pro t and taxable pro t. Tax-e ect accounting - new approach: the method prescribed by aasb 112, methodology: Account for di erences via the balance sheet: also known as the balance sheet approach, para 5 makes the following distinction: Accounting pro t is pro t or loss for a period before deducting tax expense. Taxable pro t (tax loss) is the pro t (loss) for a period, determined in accordance with the rules established by the taxation authorities, upon which income taxes are payable (recoverable: requires the preparation of 2 worksheets: Current tax worksheet - to calculate the current tax payable.