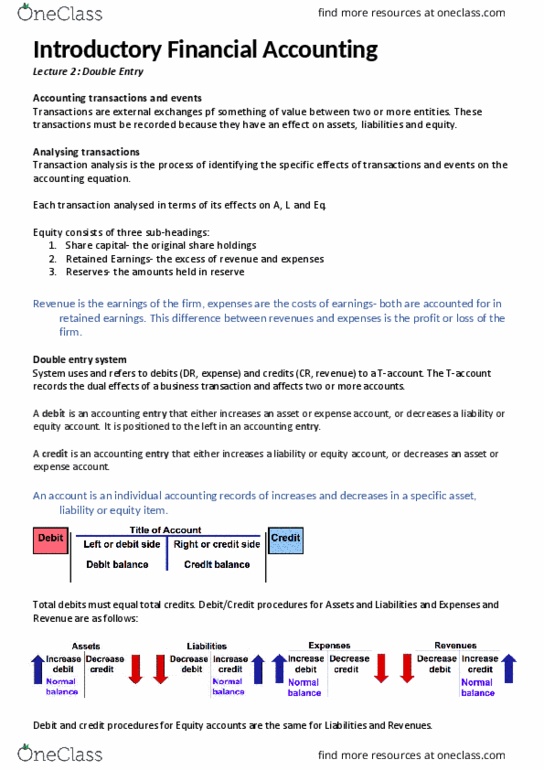

ACCT10002 Lecture Notes - Lecture 8: Private Placement, Write-Off, Cash Flow Statement

19 Jun 2018

School

Department

Course

Professor

Introductory Financial Accounting

Lecture 8: Equities, Dividends, Share Capital and Changes to Equity Accounts

Measurement Concepts for Shareholders Equity

Equity- the residual interest in the assets of the entity after deducting all its liabilities.

The Components of Shareholders Equity

Made of a number of different accounts which can comprise:

- Contributed Equity (paid up or share capital)

- Retained Earnings (current period profits + previous periods retained earnings – dividends

distributed as profits to shareholders)

- Reserves (e.g. revaluation surplus, general reserve)

The Corporate Form of Organisation

Characteristics of a corporation:

- Separate legal existence

- Limited liability of shareholders

- Transferable ownership rights

- Continuous life

- Ability to acquire capital

- Elected board of directors

- Subject to government regulations

Forming a company:

- A company is formed by registration and bound by the Corporations Act

- Each company is allocated an ABN and an ACN

- A company may adopt a constitution — set of rules governing internal management

- If no specific constitution is adopted, a company is automatically subject to the replaceable

rules of the Corporations Act

Shareholder Rights

A company is owned by its shareholders, who want both dividends and capital gain in share price. These

shareholders hold either ordinary, preference or cumulative preference shares

Ordinary shares have 3 major ownership rights:

Right to vote

Right to share in company’s profit

Right to a residual claim if company is liquidated

Preference shares have priority over ordinary shares with respect to dividends and claims at liquidation

Share Issues

Company receives cash for shares. When issuing shares, a company will have to decide how many shares

will be issued and how they will be issued in regards to timing and at what price and payment plan.

Private placement involves issue of shares to certain private investors by invitation – eg. via a broker, a

fund manager, or superannuation fund

Public issue requires a prospectus inviting public application for shares

The prospectus:

Reports on the company’s financial position, performance and plans

Contains reports from independent parties

Factors influencing the issue price of new shares include:

The company’s anticipated profits

find more resources at oneclass.com

find more resources at oneclass.com

The company’s expected dividend rate per share

The company’s current financial position

The current state of the economy

The current state of the securities market

Undersubscription:

A share offer is undersubscribed when the total number of applications received is less than the number of

shares the business is issuing. In such instances all application money is refunded and the issue is

abandoned

Oversubscription:

A share offer is oversubscribed when the total number of applications received exceeds the number of

shares the business is issuing. There are two ways to account for an oversubscription:

1. Refund excess money – first in or ballot allocation.

2. Offset excess application money against future instalments – pro rata allocation.

Note: a company can only issue the number of shares nominated in its prospectus

Equity and Earnings

At the end of the reporting period, all revenue and expense accounts are closed off to the temporary

account – the Income Summary Account (or the Profit and Loss Account or P&L Account). At this point, the

Income Summary Account reflects the Before Tax Profit or Loss.

Adjustments considered so far:

- Receivables adjustments (doubtful debts)

- Inventory adjustments (write-down)

- PPE adjustments (write-off)

- Liability adjustments (provision)

Closing the Profit and Loss to Retained Earnings

The Income Summary Account (P&L) balance now reflects the after-tax profit (or loss) which is then closed

and the balance is transferred to the Retained Earnings Account (an Equity account). The Retained Earnings

Account is a permanent equity account in the Balance Sheet.

Companies close their revenues and expenses to the Income summary account

Then they close the final profit from the Income summary account to the Retained earnings account

The Company Income Statement

Accounting Standard AASB 101, Presentation of Financial Statements, specifies the information that must

be shown in the income statement. Variations in the format of the statement are allowed provided that it

presents fairly the financial performance of the business.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Lecture 8: equities, dividends, share capital and changes to equity accounts. Equity- the residual interest in the assets of the entity after deducting all its liabilities. Made of a number of different accounts which can comprise: Retained earnings (current period profits + previous periods retained earnings dividends distributed as profits to shareholders) A company is formed by registration and bound by the corporations act. Each company is allocated an abn and an acn. A company may adopt a constitution set of rules governing internal management. If no specific constitution is adopted, a company is automatically subject to the replaceable rules of the corporations act. A company is owned by its shareholders, who want both dividends and capital gain in share price. These shareholders hold either ordinary, preference or cumulative preference shares. Right to a residual claim if company is liquidated. Preference shares have priority over ordinary shares with respect to dividends and claims at liquidation.